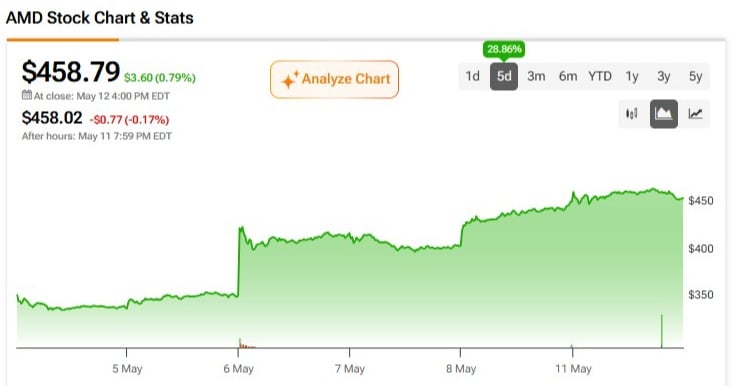

Advanced Micro Devices, Inc. (AMD) released its Q1 2026 results on May 5, and they comfortably beat revenue and earnings estimates for the quarter. The market has repriced the stock much higher since then. I can’t argue with the headline numbers, and it looks like the company’s artificial intelligence (AI) growth story is here to stay. However, I’m neutral on the stock because I believe AMD is increasingly running on a single engine, Data Center, while its valuation assumes the plane is airborne and flying.

Claim 55% Off TipRanks

Forget margin or options. Here's how the pros trade NVDAI think the real investment question lies in the gap between what the global semiconductor company delivers in aggregate and what the market is pricing in.

AMD’s Revenue Centers

AMD’s semiconductor business operates across these segments: Data Center, Client and Gaming, and Embedded, each serving different markets. The problem, in my opinion, is that revenue and growth contribution across those segments is increasingly uneven.

Let’s take the Data Center segment first. Revenue here comes from EPYC server central processing units (CPUs) and Instinct AI accelerators, competing directly with Intel (INTC) on the CPU side and Nvidia (NVDA) on the graphics processing unit (GPU) side. The company made a record $5.78 billion in Q1 2026, 57% higher than in the same period last year. That means the segment now accounts for around 56% of AMD’s total sales, which is a first.

Meanwhile, you can still point to some fantastic year-over-year growth in the other segments: Client and Gaming rose 23% to $3.6 billion, and Embedded grew 6% to $873 million. However, on a sequential basis, the company’s revenue is flat, primarily due to the seasonality of the other segments. If we take out the Data Center here, Q1 was effectively stagnant.

AMD’s Business Is Starting to Have a Small Concentration Problem

If we look a bit deeper, on the customer level, the concentration is obvious. First, AMD has expanded its Instinct GPU partnership with Meta (META) to deploy up to 6 gigawatts of Instinct GPUs across multiple product generations, including a custom accelerator based on the MI450 architecture.

I know it’s a big win that validates the company’s AI infrastructure push, but even more importantly, it gives AMD multi-year revenue visibility that most peers lack. On the other hand, we have a single hyperscaler commitment that is large enough to materially move the company’s top line, and that cuts both ways if AI capex budgets shift.

Additionally, we have word from management that AMD now expects the server CPU total addressable market (TAM) to surpass $120 billion by 2030. During the Q1 earnings call, company CEO Lisa Su sounded very confident that AMD will reach tens of billions in Data Center AI revenue next year, and I think those projections are credible, given how quickly they’ve managed to grow it over the last few quarters.

Again, though, said growth is almost entirely contingent on the AI infrastructure cycle sustaining itself, which is the same assumption holding up AMD’s valuation.

Margin Growth Is Encouraging

The margins are a big part of why the headline numbers look great. Non-GAAP gross margin came in at 55% for Q1, up 170 basis points year-over-year, with the Data Center segment operating income of $1.6 billion at a 28% segment margin, up from 25% a year ago.

Management also guided Q2 non-GAAP gross margin to be approximately 56%. Yes, the trajectory is positive, but it is important that we look at the main driver here: margins are expanding because Data Center, the highest-margin segment, is growing fastest. If that mix dynamic reverses, I’m almost positive that the margin expansion story goes with it, especially since sales in the Gaming segment will drop by about 20% in H2, and it wasn’t exactly a high-margin driver anyway.

Besides that, non-GAAP operating expenses of $3.1 billion grew 42% year-over-year, and management is guiding $3.3 billion for Q2 while they’re spending heavily to compete with Nvidia.

It’s Not Too Pricey, but I’d Hold Off on the Rally for Now

AMD currently trades at a trailing P/E of around 150x. In my view, that is a significant premium for a business whose growth is concentrated in a single segment. Meanwhile, there’s Nvidia, the clear AI GPU market leader with a superior software ecosystem, trading at roughly 26x forward earnings. Broadcom (AVGO) is compounding its AI revenue at a comparable rate through custom application-specific integrated circuit (ASIC) design while trading at approximately 84x.

I believe that AMD’s multiple implies expectations of either rapidly closing the competitive gap with Nvidia, beyond what historical trends suggest, or a sustained Data Center growth rate that would push the stock to its current price. The Q2 guide of $11.2 billion is well above the prior consensus of $10.5 billion, and yes, it supports the near-term re-rating case. However, I’m not sure it justifies a nearly 150x earnings multiple for a business that is sequentially flat ex-Data Center. That is a harder argument to make.

Is AMD a Buy, Sell, or Hold?

Turning to Wall Street, AMD has a Strong Buy consensus rating based on 27 Buys and eight Holds assigned in the last three months. At $442.94, the average AMD price target implies 3.46% downside from today’s price.

All things considered, I know that the long-term upside from AMD’s AI-centric data center sales is credible, but at today’s price, I’d recommend watching the stock for now.