Amazon’s (AMZN) Q1 answered the key questions around its heavy spending, showing that the company is building a long-term advantage rather than just burning cash. For the past year, investors have debated whether the global technology and retail platform was investing for the future or simply caught in an expensive artificial intelligence (AI) race. The Q1 report has helped settle that.

Claim 55% Off TipRanks

Forget margin or options. Here's how the pros trade AMZNAmazon Web Services (AWS) is accelerating, AI is generating explosive revenue, and retail continues to show the operating leverage that has long defined the business. Accordingly, I remain bullish on AMZN stock, even after it reached new all-time highs.

AWS Finally Gets the Last Word

What instantly grabbed my attention the moment I looked at Amazon’s Q1 report was not just revenue, although $181.5 billion, up 17% year-over-year, was hardly quiet. It was AWS growing 28% to $37.6 billion, its fastest growth rate in 15 quarters, on a business now running at roughly $150 billion annually. That is the sort of acceleration critics said was getting harder, not easier, as the base became enormous. Amazon just made the opposite case.

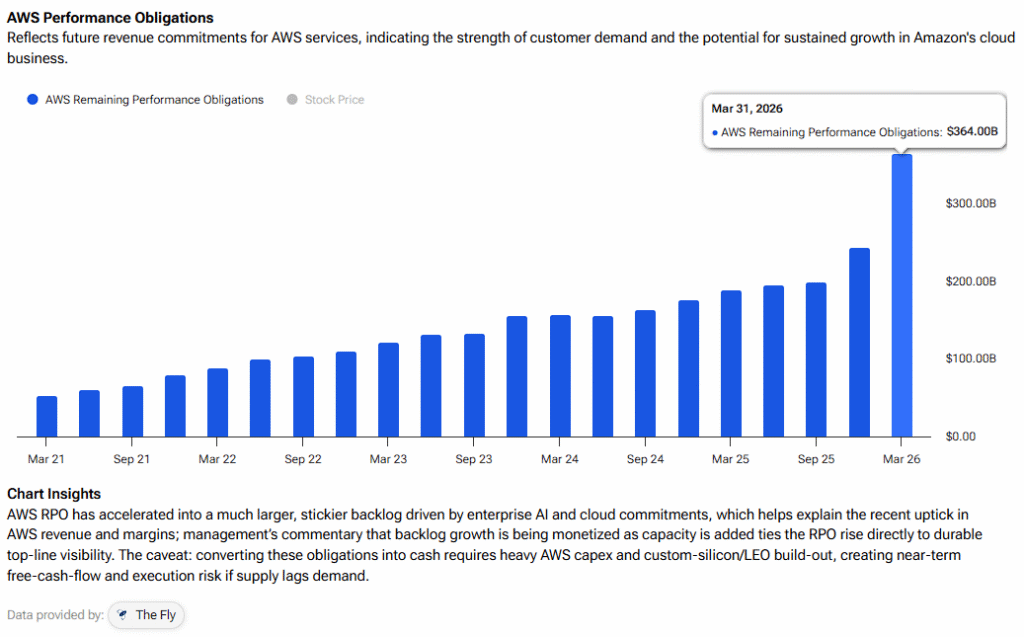

I believe this was key to Wall Street sentiment because investors had been watching for $43.2 billion in quarterly cash capital expenditures, mostly tied to AWS and generative AI. Such a large figure would likely have looked reckless if growth had slowed. However, it now looks different as the cloud engine is accelerating. Management argued that spend comes first and monetization follows. That is uncomfortable, but not unfamiliar for Amazon. AWS performance also surged to a staggering $364 billion, implying sustained momentum ahead.

Then came another surprise when Andy Jassy said AWS’s AI revenue run rate is already above $15 billion, only three years into this AI wave. He contrasted that with AWS’s early history, when the cloud business had a $58 million run rate three years after launch. The comparison is imperfect, of course, but the message is that there is already a large business growing on a large cloud platform, and the scale of all this in such a short period of time is mind-blowing.

AI Developments Drive Growth

Amazon’s AI opportunity is not limited to just selling standalone AI tools. Management said AI workloads often bring more traditional cloud spending with them, because customers need data, storage, compute, security, and inference close together. For example, Trainium, the company’s custom AI chip family, has become a key part of its pitch to large model builders.

Jassy said Amazon’s chips business is above a $20 billion annual revenue run rate and growing at triple-digit rates. Custom silicon could give Amazon better control over supply and better unit economics. It also keeps the company from being just another buyer stuck in the graphics processing unit (GPU) line.

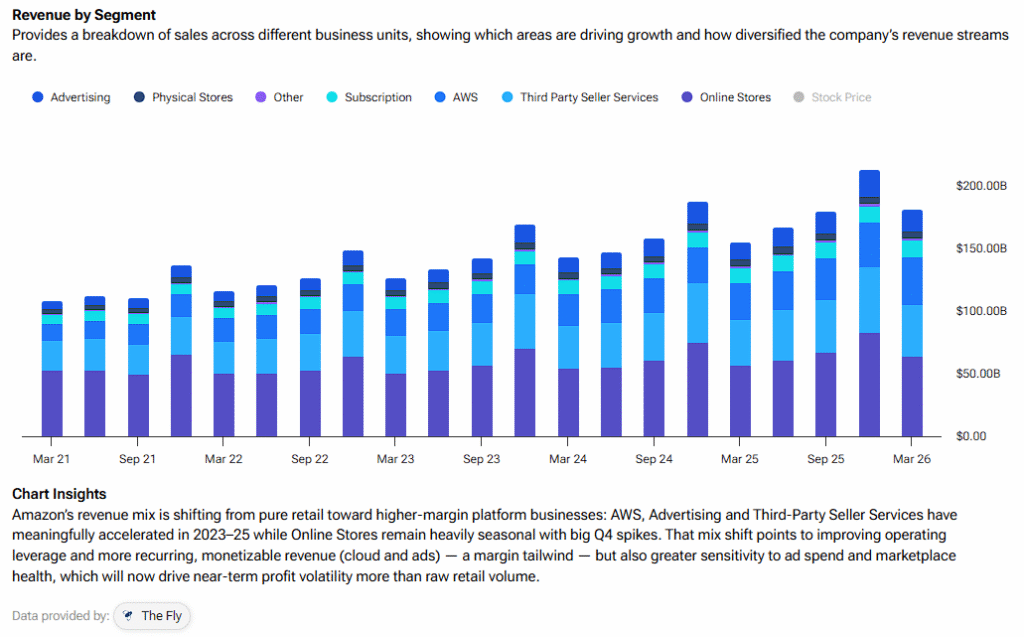

While all this is happening, retail is quietly widening the moat. North America sales rose 12% to $104.1 billion in Q1, while segment operating income reached $8.3 billion. Unit growth accelerated, too, and management said fulfillment expense grew more slowly than units. So we are looking at a classic Amazon case. Faster delivery, better inventory placement, more robotics, fewer wasted steps, all compound to better unit economics.

Advertising also performed well. Amazon’s ad revenue rose 24% to $17.2 billion, and management said the business has crossed $70 billion on a trailing 12-month basis. Remember that this is a very different profit pool from boxes and warehouses. Advertisers are paying to reach shoppers close to buying. Google (GOOGL) and Meta (META) have scale, but Amazon has purchase intent right at the checkout button.

The Breakout Still Has Room

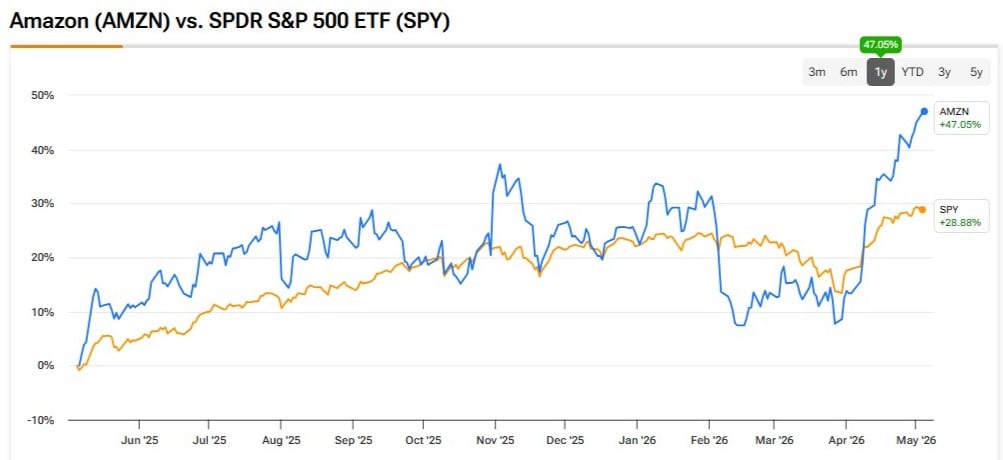

AMZN finally broke out to new highs, and the post-earnings momentum has held as the market reprices the business as an accelerating compounder again. Using this year’s consensus earnings per share (EPS) estimate of $8.55, we see the stock is trading at roughly 31x earnings.

The 31x multiple looks more than justified if EPS can grow at least in the mid- to high-teens over the medium term, in my view. It is a reasonable premium for a company with one of the strongest consumer moats in the world, including a cloud platform still compounding at scale, an emerging AI infrastructure franchise, and a flourishing ad business.

Honestly, the retail moat is just unmatched. Competitors can copy bits and pieces, but I don’t think anyone can copy the flywheel at this point. In the cloud, the competition is tougher, for sure, with Meta and Google fighting hard. Yet AWS growing 28% on a $150 billion run rate suggests Amazon is not being left behind. It is still winning enough to matter, and perhaps more than enough.

That is what I think the current valuation still does not fully account for. Don’t get me wrong, a retailer alone would not deserve this multiple. A cloud company alone might face too much AI-capex anxiety as well. However, Amazon is both. Plus, you have advertising, silicon, and logistics layered on top. When several engines accelerate together, the multiple can hold. In Amazon’s case, it may even expand.

Is AMZN a Buy, Sell, or Hold?

Despite the stock’s sustained post-earnings rally, Amazon still has a Strong Buy consensus rating on Wall Street, based on 45 Buy and two Hold ratings. Notably, no analyst rates the stock a Sell. Further, AMZN’s average price target of $315.09 implies nearly 16% upside potential over the next 12 months.

The Bottom Line

Amazon’s quarter did not remove every single risk out there. At the end of the day, capex is huge and free cash flow is compressed. Also, cloud competition remains intense. However, the company has earned the benefit of ambition. AWS is accelerating, AI is monetizing, retail is compounding, and the valuation remains fair. For AMZN, the bullish momentum looks sustainable.