Amazon (AMZN) shares turned lower during Thursday’s regular session, surrendering a nearly 3% after-hours gain despite reporting first-quarter results that topped Wall Street’s expectations. While overall revenue climbed 17% to $181.5 billion, the market’s initial excitement over cloud recovery is being met with caution regarding the massive capital required to fuel the AI industry.

Claim 55% Off TipRanks

- Unlock hedge fund-level data and powerful investing tools for smarter, sharper decisions

- Discover top-performing stock ideas and upgrade to a portfolio of market leaders with Smart Investor Picks

For context, Amazon posted earnings of $2.78 per share, much higher than the $1.63 analysts expected. The company’s bottom line was helped by a $16.8 billion gain from its investment in AI startup Anthropic. Despite spending heavily on new technology, Amazon managed to reach a record operating margin of 13.1%, showing it is finding ways to be more efficient.

What Stood Out This Quarter

The biggest driver behind the stock’s jump was Amazon Web Services (AWS). Cloud revenue grew 28% to $37.6 billion, marking its fastest growth in almost four years. CEO Andy Jassy said companies are moving beyond testing AI and are now launching large-scale projects on Amazon’s platform.

A key part of this rally is Amazon’s move into making its own AI chips, such as Graviton and Trainium. These custom chips have already reached a $20 billion annual revenue run rate. By developing its own chips, Amazon can offer more affordable cloud services to major clients like Meta Platforms (META) and Uber (UBER), reducing reliance on costly third-party suppliers and lowering expenses.

However, the company is spending a massive amount to stay ahead. Free cash flow dropped to $1.2 billion from $25.9 billion a year ago because Amazon spent nearly $60 billion this quarter on property and equipment, mostly for AI data centers.

What to Watch Next for AMZN Stock

Looking ahead, investors are watching how Amazon handles its $200 billion spending plan for 2026. The goal is to double data center capacity to meet rising AI demand. While the scale is large, the recent growth in AWS suggests these investments are already driving revenue.

Analysts are also tracking new partnerships, including OpenAI using Amazon’s infrastructure. The key question in the coming months is whether strong profits from AWS and advertising can keep covering these high AI costs without hurting cash flow.

Top Evercore Analyst Weighs In on Amazon Stock

Following Amazon’s Q1 2026 earnings report, Top Evercore analyst Mark Mahaney reiterated his Outperform rating and maintained his price target of $285. He said Amazon delivered a “clean beat” in Q1, with revenue and operating income both coming in well above expectations and at the high end of guidance. He highlighted strong AWS growth — its fastest in nearly four years — along with solid margins across retail and international segments.

While earnings included a boost from the Anthropic investment, core profitability still beat estimates. Looking ahead, Mahaney said Amazon’s Q2 guidance was strong and pointed to continued heavy spending on AI infrastructure, reinforcing its long-term growth plans.

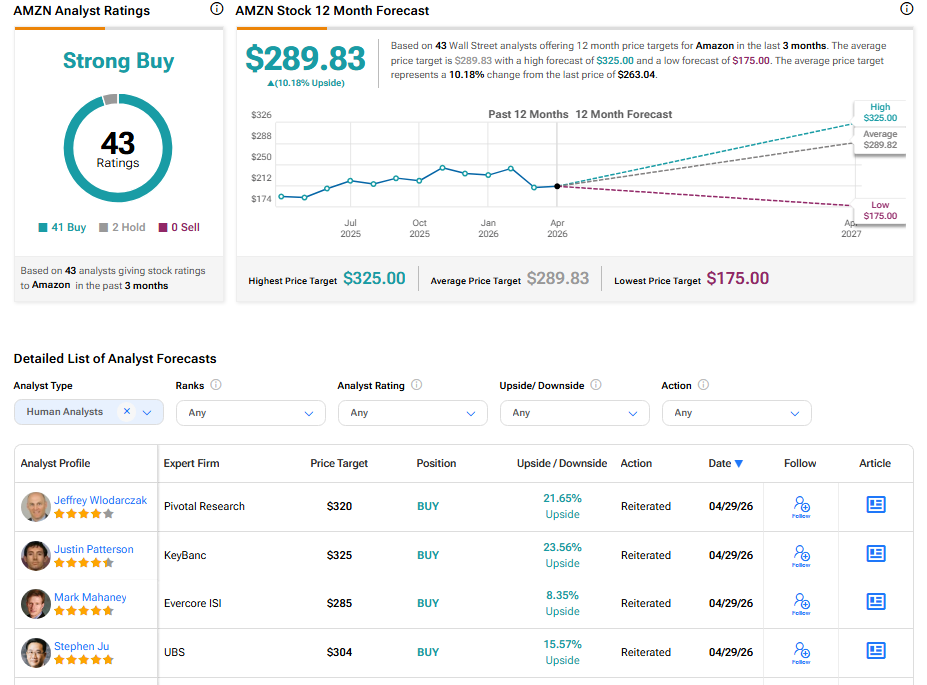

What Is the Price Target for AMZN Stock?

Currently, Wall Street has a Strong Buy consensus rating on Amazon stock based on 41 Buys and two Holds. The average AMZN stock price target of $289.83 indicates 10.18% upside potential. However, it’s worth noting that estimates will likely change following today’s earnings report.