Amazon (AMZN) stock is no longer the bargain it was in March, when shares briefly traded below $200 amid heightened concerns about the company’s aggressive spending on artificial intelligence (AI) infrastructure. Since then, the stock has rebounded sharply. However, I still see room for further upside, mainly because Amazon Web Services (AWS) continues to drive a disproportionate share of Amazon’s intrinsic value.

Meet Samuel – Your Personal Investing Prophet

200% short exposure to AMZN with AMZOIn my view, Amazon should not be valued as a single business. The company is better understood as a combination of two very different assets: a massive retail ecosystem and AWS, one of the highest-quality cloud infrastructure businesses in the world. That is why I believe a discounted cash flow (DCF) analysis can be particularly useful here. It helps estimate how much future free cash flow each part of the business can generate and what those cash flows are worth today.

For that reason, even though AMZN no longer screams “deep value,” I still view the stock as a Buy at current prices.

How Much Is Amazon’s Retail Ecosystem Worth?

Amazon divides its retail operations into two reporting segments: North America and International. Over the past 12 months, these two segments generated roughly $605 billion in combined revenue, accounting for approximately 81% of Amazon’s total sales. Specifically, North America alone represented about 72.2% of revenue from worldwide operations.

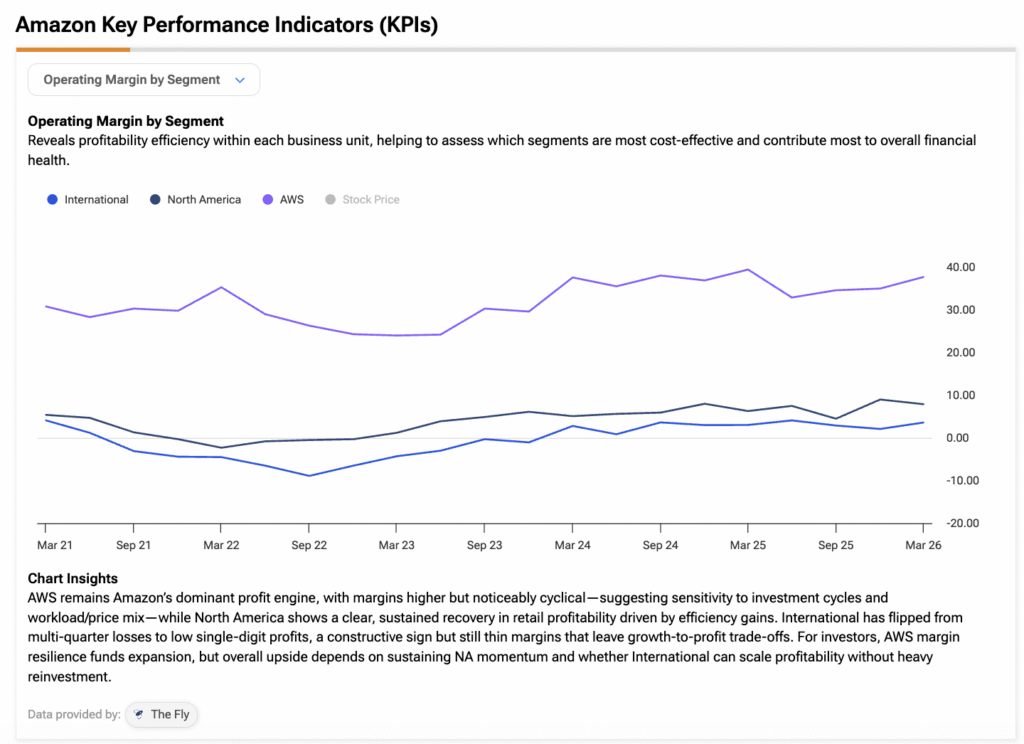

On a standalone basis, Amazon’s North America and International segments are lower-quality businesses than Amazon Web Services, not because they lack scale or profitability, but because they are more capital-intensive, more cyclical than cloud, and inherently less predictable. Still, these segments are far more resilient than traditional retail operations. They encompass Amazon’s entire retail ecosystem, including higher-margin businesses such as advertising, Prime subscriptions, marketplace fees, and fulfillment services.

With that in mind, I believe it is reasonable to assume that the North America segment can continue growing at 12% annually over the next five years, broadly in line with its growth over the past 12 months. At the same time, assuming 19% annual growth for the International segment also seems reasonable as a base case, reflecting its recent momentum before both businesses eventually normalize to a 2% long-term growth rate.

On profitability, I assume operating margins (EBIT) remain broadly stable at 7.3% for North America and 3.1% for International, despite having improved recently due to the increasing contribution from higher-margin businesses such as advertising. Conservatively assuming no changes in working capital and discounting future cash flows at an 8% rate, this framework implies a combined equity value of approximately $875 billion for Amazon’s retail business.

AWS Is Where the Real Value Sits

Even though AWS represents a much smaller share of revenue than North America and International combined, it is clearly a much higher-quality business. AWS is more profitable, more scalable, and generates far more predictable cash flows than the retail ecosystem.

With that in mind, my base case assumes AWS will continue to grow at roughly 20% annually over the next five years, in line with its FY2025 growth. On profitability, I assume AWS maintains its trailing operating margin of 35.2%, followed by 100 basis points of annual expansion through 2031 as scale continues to improve. After that, the business is assumed to normalize to a more sustainable long-term growth rate of 2%.

Using a lower discount rate of 7%, which I believe is justified by AWS’s higher margins and lower cash flow volatility, I arrive at a fair value of approximately $2.2 trillion for AWS. Adding Amazon’s retail business to that estimate results in a total equity value of roughly $3.08 trillion. Assuming the share count remains at 10.75 billion, this implies a price target of approximately $286 per share, representing potential upside of about 7% from current levels.

A Sanity Check on Amazon’s Valuation

Needless to say, the output of a discounted cash flow analysis ultimately depends on the assumptions behind it. Small changes in long-term growth rates can materially affect the outcome. For example, if AWS’s perpetual growth rate were increased to 3% instead of 2%, Amazon’s fair value would rise to roughly $3.5 trillion, or about $332 per share.

In any case, the more important point is that Amazon does not appear particularly expensive even under more conservative assumptions. Based on current consensus estimates calling for 20.3% earnings-per-share (EPS) growth this year, the stock trades at approximately 31x FY2026 earnings. However, this forward valuation is actually 38% below Amazon’s five-year average forward P/E of roughly 50x, indicating that the stock trades at a deep historical discount despite its recent rally.

At first glance, 31x earnings may still seem demanding. However, Wall Street expects EPS to increase from roughly $8.63 in 2026 to more than $18 by 2030. In other words, if those estimates prove reasonably accurate, Amazon’s earnings power could more than double over the next four years.

Is AMZN a Buy, Hold, or Sell, According to Wall Street Analysts?

Amazon is rated a Strong Buy by Wall Street analysts. Of the 46 analysts who have covered the stock over the past three months, 45 recommend Buy and only one rates the shares Hold. The average price target of $318.23 implies potential upside of 20.48% from current levels.

AWS Keeps the Bull Case Alive

Amazon is a Buy for me at current prices. Even when viewed through a discounted cash flow valuation using relatively conservative assumptions, I believe the stock still offers a margin of safety. The same conclusion holds when considering more traditional valuation metrics. That said, it is no longer as compelling as it was in March, when shares briefly traded below $200.

Perhaps more importantly, I believe the market is still underestimating how much of Amazon’s intrinsic value is tied to AWS. Meanwhile, the core retail ecosystem continues to improve in both profitability and overall business quality.