Shares of Autoliv (ALV) fell in pre-market trading after the company lowered its FY24 guidance, leaving investors disappointed. The producer of airbags and seatbelts now expects its organic sales to grow by 2% year-over-year, compared to its previous estimate of 5% growth. Additionally, the company reduced its adjusted operating margin forecast to between 9.5% and 10% from the earlier estimate of 10.5%.

Claim 55% Off TipRanks

- Unlock hedge fund-level data and powerful investing tools for smarter, sharper decisions

- Discover top-performing stock ideas and upgrade to a portfolio of market leaders with Smart Investor Picks

Why Did ALV Lower FY24 Forecast?

ALV lowered its FY24 forecast due to an expected 3% decline in global light vehicle production (LVP) this year. This decline impacts Autoliv as it aims to have its products fitted in best-selling cars. However, the company’s management noted that they continue to anticipate a significant increase in profitability in the second half of the year, with margins expected to be around 11% to 12%, up from 8.0% in the first half.

ALV’s Q2 Results

The company reported Q2 adjusted earnings of $1.87 per share, a decline of 3% year-over-year. This fell short of analysts’ consensus estimate of $2.20 per share.

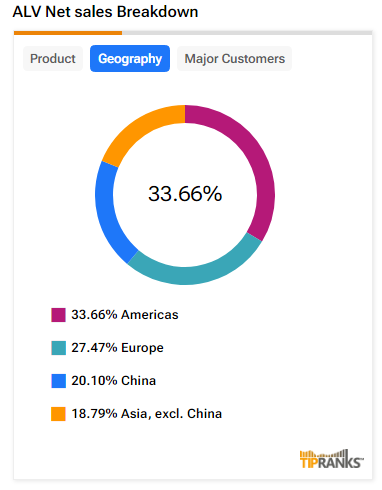

Sales declined by 1.1% year-over-year, with revenue hitting $2.6 billion, missing analysts’ expectations of $2.73 billion. The lower-than-expected sales were attributed to a decline in LVP with certain key customers and reduced sales in the Americas and China. The Americas account for more than 30% of ALV’s sales.

Is ALV a Good Stock to Buy?

Analysts remain cautiously optimistic about ALV stock, with a Moderate Buy consensus rating based on 10 Buys and six Holds. Over the past year, ALV has increased by more than 15%, and the average ALV price target of $133.21 implies an upside potential of 22.7% from current levels. These analyst ratings are likely to change following ALV’s Q2 results today.