Alphabet (GOOGL), the parent firm of Google, has been on a sharp run, and this week Alphabet even briefly passed Nvidia (NVDA) by market cap in after-hours trade. That marks a big shift for a firm that was once seen as at risk from the AI boom. However, there’s one glaring risk tied to Anthropic.

Claim 55% Off TipRanks

Forget margin or options. Here's how the pros trade NVDAThe new bull case is clear. Wall Street now sees Google as one of the few firms that can win in AI at more than one level. It has Gemini and DeepMind for AI models, Google Cloud for compute, TPUs for chips, and a huge reach through Search, YouTube, and Android. As Gene Munster of Deepwater Asset Management put it, “Google is one of the two best-positioned AI companies because they own most of the stack.”

That view got a boost after Alphabet’s latest results. JPMorgan Chase’s (JPM) five-star analyst Doug Anmuth called the stock its “top overall pick” in tech, while Mizuho’s top analyst Lloyd Walmsley raised its price target. A key reason was Google Cloud’s backlog, which nearly doubled to $462 billion. For stock bulls, that backlog points to strong future sales from AI demand.

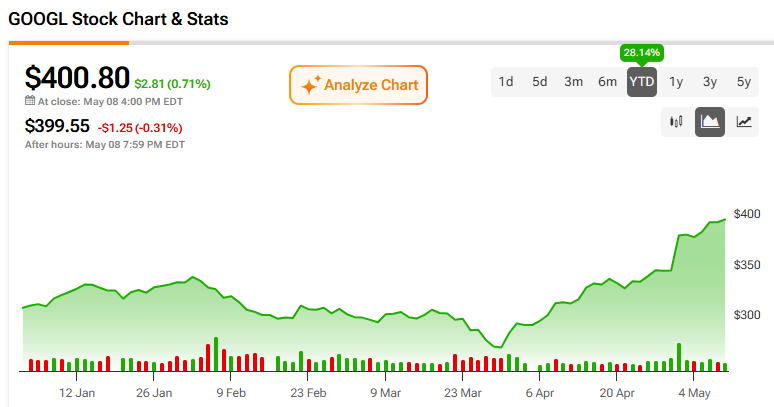

Meanwhile, GOOGLE shares rose slightly on Friday, closing at $400.80.

Anthropic Adds Upside, but Also Risk

However, there is one catch. A large part of that cloud story may be tied to Anthropic, the AI firm behind Claude. Reports say Anthropic agreed to spend $200 billion on Google Cloud over five years. If that sum is compared with Alphabet’s cloud backlog, it could make up more than 40% of future cloud sales under contract.

That is why some analysts are more cautious. D.A. Davidson four-star analyst Gil Luria said the setup looks like Oracle Corporation (ORCL), which saw its stock jump after a huge backlog gain, only for the market to later focus on how much of that demand came from OpenAI. “They did it the same way Oracle did,” Luria said, adding that Alphabet did not make clear how much of the backlog gain came from one deal with Anthropic.

In short, the worry is not that Anthropic is a weak client. The worry is that investors may be giving Alphabet credit for broad AI demand when a large share of the new backlog could depend on a single fast-growing, cash-burning AI firm.

Google’s AI Stack Still Looks Strong

Even so, Alphabet has a wider base than most AI plays. It can sell cloud tools, rent out compute, use its own chips, and add AI into products that billions of people already use. Its TPUs also give investors a way to bet on AI chips without buying Nvidia alone.

At the same time, Alphabet is spending a lot to keep up. The company is now set to invest heavily in AI data centers and compute. That may help it defend its lead, but it also raises the bar. Investors will want to see that this spend leads to real profit, not just a larger backlog.

For now, Alphabet has moved from AI laggard to AI leader in the eyes of Wall Street. But after a strong stock run, the key issue is changing. The question is no longer whether Google can compete in AI. The real question is how much of its AI growth is broad, lasting demand, and how much depends on Anthropic.

Is Google Stock a Buy, Sell, or Hold?

Turning to the Street, Alphabet boasts a Strong Buy consensus view. Of 32 ratings issued, 28 analysts rate it a Buy, while four analysts rate it a Hold. The average GOOGL stock price target is $428.09, implying a 6.81% upside from the current price.