Tech giant Alphabet (GOOGL) will announce its results for the first quarter of 2026 today, April 29, after the market closes. The stock has been on a tear, surging 118% over the past year and climbing 12% year-to-date, fueled by its booming cloud business, high demand for custom TPU chips, and major AI deals. While revenue is expected to grow nearly 19% to $106.9 billion, Wall street analysts expect a 6.4% dip in earnings per share to $2.63 as the company ramps up spending on AI data centers and infrastructure.

Claim 55% Off TipRanks

- Unlock hedge fund-level data and powerful investing tools for smarter, sharper decisions

- Discover top-performing stock ideas and upgrade to a portfolio of market leaders with Smart Investor Picks

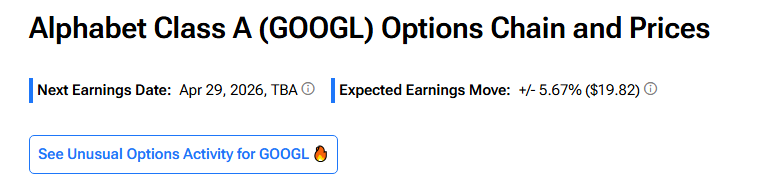

According to TipRanks’ Options Tool, option traders are expecting a 5.67% move in either direction in GOOGL stock in reaction to Q1 results. This implied move is higher than Alphabet stock’s average post-earnings move (in absolute terms) of 1.44% over the past four quarters.

Key Focus Areas for Investors

Investors are looking for proof that Alphabet’s massive AI investments are translating into real profits. Here is what to watch:

- Cloud & AI Momentum: Is Google Cloud growing faster as companies adopt new AI tools? Investors want to see if Gemini is driving new revenue.

- Ad Resilience: Are Search and YouTube holding strong against rising competition in the digital ad space?

- Spending vs. Returns: Shareholders will look for disciplined spending on data centers and updates on how much cash—via dividends and buybacks—will be returned to them.

Analysts’ Views on GOOGL Ahead of Q1 Results

Just yesterday, top Mark Shmulik of Bernstein reiterated an Outperform rating and a $900 price target on Alphabet. He expects solid 1Q performance, with Search and Cloud supported by AI-driven demand, while YouTube may be mixed but not a major drag. Shmulik said he does not expect changes to CapEx guidance this quarter and will look for more details on AI product progress and any OpEx savings.

His estimates point to Financial Services revenue of about $468 million, slightly below Street expectations, while EBITDA margins are seen near 30% versus company guidance of 29%. He also expects EPS of $0.12, broadly in line with consensus estimates.

Looking ahead, he still sees around 30% revenue growth as achievable but flagged risks from valuation, margin pressure, and rising competition, especially from OpenAI and Meta Platforms.

Is GOOGL Stock a Buy Right Now?

Heading into Q1 earnings, Wall Street has a Strong Buy consensus rating on Alphabet stock based on 26 Buys and five Holds. The average GOOGL stock price target of $387.68 indicates 12.57% upside potential from current levels.