Alibaba’s (BABA) investment cycle is hiding its true earnings power. Sure enough, the latest quarter gave the market plenty of reasons to stay skeptical. Notably, margins are coming under pressure, and cash flow is moving sharply in what initially seems to be the wrong direction. Yet I don’t think these reasons tell the full story of this technology company that facilitates online shopping and business transactions.

Meet Samuel – Your Personal Investing Prophet

- Start a conversation with TipRanks’ trusted, data-backed investment intelligence

- Ask Samuel about stocks, your portfolio, or the market and get instant, personalized insights in seconds

Much of the weakness stems from a deliberate decision to spend heavily on cloud and artificial intelligence (AI). However, these investments should strengthen the business over the next several years. That is exactly why the stock still looks attractive to me despite the recent earnings disappointment. I remain bullish on Alibaba today.

The Heavy Cost of Staying In the Lead

There are a few reasons Alibaba has underperformed lately. For starters, in recent years, fund managers have treated Chinese tech as radioactive, fleeing toward the predictable growth of U.S. mega-caps. While American tech benefited from rampant AI enthusiasm, Alibaba navigated a tepid post-pandemic recovery in China, muted domestic demand, and relentless geopolitical friction. This has proven to be a relentless overhang that has created a permanent “avoid” mentality among institutional investors.

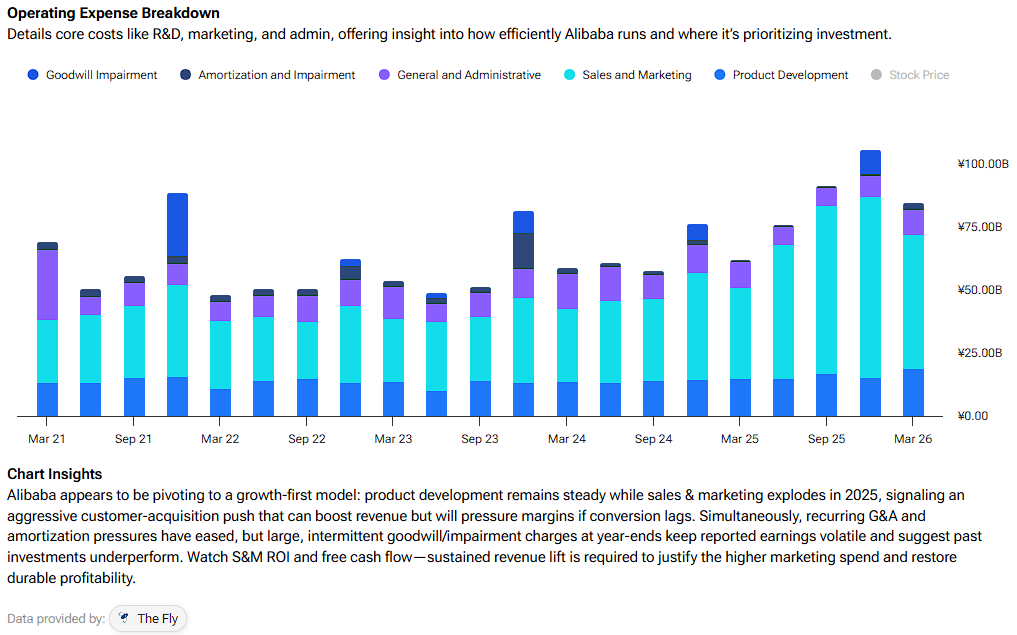

Last week’s Q4 fiscal 2026 results certainly didn’t do much to ease the market’s nerves. At first glance, the numbers looked horrific, adding to the already dampened sentiment. Adjusted net profit plunged by 99.7% year-over-year and obviously missed consensus expectations. Adjusted EBITDA also plunged 84% to $2.4 billion. In fact, the company even swung to a negative free cash flow position of $2.5 billion for the period.

Wall Street looked at these shrunken margins and panicked. Indeed, you can’t blame those who conclude that Alibaba’s core business model was in decline amid intense price wars. E-commerce margins across Taobao and Tmall were also severely squeezed as the company scrambled to defend its market share against aggressive, low-cost rivals. Operating costs ballooned across the board, and the headline loss of profitability made it easy for bears to argue that the stock remains dead money.

Buying the Future with Today’s Cash

However, if you look closely at where that cash actually went and assess what this means for Alibaba, the story can change entirely. Specifically, that terrifying drop in net profit wasn’t driven by an organic collapse in demand. Instead, it was the result of a deliberate, aggressive capital allocation strategy. Alibaba is killing short-term earnings to bankroll its long-term survival in the AI era. Management is essentially telling us that the cost of admission to the next tech cycle is punishingly high, and they are willing to pay it upfront.

We are already seeing the initial green shoots of this investment cycle. Take Alibaba’s Cloud Intelligence Group, for instance, which grew its revenue by 38% year-over-year, with external customer revenue up 40%. This acceleration was supercharged by triple-digit growth in sales of AI-related products, showing that corporate China is migrating its workloads to Alibaba’s infrastructure. CEO Eddie Wu noted that the return on investment for this tech spend over the next three to five years is crystal clear, and the traction behind their Qwen large language models confirms they are building a real competitive moat.

Yet this isn’t just a cloud story either. Alibaba’s domestic e-commerce arm is undergoing a pricey facelift. The company poured massive subsidies into its new “Taobao Instant Commerce” initiative to capture the fast-growing quick-commerce market. The results speak for themselves. Quick commerce revenues skyrocketed by 57% year-over-year. So while these delivery subsidies squeezed today’s profits, they are most certainly succeeding in stabilizing user engagement and driving transaction volume.

An Absurdly Cheap Valuation

I readily concede Alibaba deserves a permanent “China discount.” We have to be honest about that: anyone investing here without factoring in unpredictable regulatory shifts or geopolitical friction, such as U.S. export restrictions on AI semiconductors, is daydreaming. The structural risk of Chinese American Depositary Receipts (ADRs) naturally caps the earnings multiples Western institutions will pay. However, even after applying a harsh haircut for these ongoing political headaches, the current price looks completely disconnected from reality.

Note that Alibaba’s current earnings look artificially depressed by this huge investment cycle. Once these capital expenditures normalize and new initiatives scale, the underlying earnings power will eventually emerge. Wall Street consensus currently projects an expected earnings per share (EPS) of $6.80 for Fiscal year 2027 and $9.22 for Fiscal year 2028, on the conservative front.

These projections imply a forward P/E multiple of just 19.5x for Fiscal year 2027 and a remarkably low 14.4x for Fiscal year 2028. To put that in perspective, these forward multiples represent a staggering 30%–50% discount to Alibaba’s own 5-year historical average P/E of about 28x. Considering Alibaba is a tech behemoth controlling half of Chinese e-commerce and boasting world-class cloud infrastructure, I believe these multiples are absurd.

At its current price levels, BABA stock may not benefit from a modest multiple expansion and its underlying earnings growth. However, it still offers a decent margin of safety, as further multiple compression appears hard to justify, in my view.

Is BABA Stock a Buy, Sell, or Hold?

Despite its recent underperformance, Alibaba stock maintains a Strong Buy consensus rating on Wall Street, based on 16 Buy and one Hold ratings. Notably, no analyst rates the stock a Sell. Furthermore, BABA’s average price target of $189.89 implies about 40% upside over the next 12 months.

Final Thoughts

Alibaba is testing investors’ patience. It has been doing so for years. The market hates short-term margin contraction, and so it’s not surprising to see this trend sustained. However, true value investors may want to welcome the recent underperformance. Once capex moderates, Alibaba is likely to come out on the other side looking very cheap. At today’s price levels, the risk-reward ratio is heavily skewed in your favor.