Much of the discussion around AI has centered on its impact on the workplace and the digital economy. Questions surrounding jobs remain unresolved, while the so-called “SaaSpocalypse” has reflected the software sector’s struggle to adapt to rapidly changing dynamics. Yet, AI is not limited to the workplace. Like human intelligence itself, its influence is likely to extend across nearly every part of daily life.

Meet Samuel – Your Personal Investing Prophet

- Start a conversation with TipRanks’ trusted, data-backed investment intelligence

- Ask Samuel about stocks, your portfolio, or the market and get instant, personalized insights in seconds

In addition to freeing up consumer leisure time, AI – especially generative AI – promises to boost productivity and creativity for entertainment content providers. Higher productivity, lower costs, and consumers having more free time could prove transformative for the entertainment industry.

Morgan Stanley analyst Sean Diffley covers the media and entertainment sector, and he’s been watching the effects of AI as a leisure play.

“American leisure time has been remarkably stable for the last 20 years at ~4-5 hours/day (with TV accounting for about half of this ‘free time’). AI has the potential to add 30-60 minutes of incremental leisure time a day in the next 3-5 years and it is not crazy to imagine a world where we only have to work 3-4 days a week. Today, your full self-driving car can drive you to work while you check emails or watch NFLX, productivity tools make you more efficient at getting tasks done and one day robots may do your chores. With increasing free time, Entertainment could be the last thing standing when most daily tasks are automated,” Diffley opined.

The analyst goes on to extrapolate from that and picks out two entertainment stocks for investors to buy now, before a boom sets in. We’ve opened up the TipRanks database to find out what Wall Street thinks of these Morgan Stanley picks; here are the details, and Diffley’s comments on his picks.

Liberty Formula One (FWONK)

The first entertainment stock we’re looking at here, Liberty Formula One Group, is the motor racing arm of the larger Liberty Media Corporation. Liberty Media operates through two publicly traded subsidiaries, and Formula One occupies what is quietly described as ‘pinnacle of motorsports.’ Taken together, the motor racing arms that make up the Formula One Group are responsible for the FIA’s (the International Automobile Federation, whose sport division governs automobile racing) Formula One World Championship.

Formula One Group has two main assets. Formula 1 is one of the leading, and most exciting, motor sports in the world, and is currently in its 76th consecutive season of championship races. The company’s other leading asset is MotoGP, the world’s top motorcycle racing circuit. Together, these racing circuits feature 46 races, held around the world; Formula 1 races are scheduled in over 20 countries, MotoGP heats are held in 18 countries. We should note that Liberty Media acquired MotoGP just last year, adding the popular motorcycle racing name to its motorsport portfolio.

The company generates revenue through several streams, including race promotion fees, sponsorship and partnership agreements, media rights, hospitality packages, and freight and logistics services tied to race operations.

Shares of FWONK have fallen more than 10% this year as investors weigh the financial impact of the MotoGP acquisition and question whether the company can continue meeting earnings expectations following the deal. In addition, geopolitical tensions in the Middle East have added another layer of uncertainty after major races in Bahrain and Saudi Arabia were canceled.

The company is set to report first-quarter results on Thursday. Before that release, however, it is worth revisiting the company’s fourth-quarter performance to better understand its current positioning. In Q4 2025, Formula One Group reported revenue of $1.61 billion, marking growth of more than 37% year over year and topping expectations by roughly $58.7 million. The company ended the year with slightly more than $1 billion in cash and liquid assets, alongside total debt of $5.1 billion. Liberty Formula One Group is scheduled to report Q1 2026 results on May 7.

Morgan Stanley’s Diffley, in looking at Liberty Formula One, notes that the company currently presents investors with a sound entry point and solid prospects for growth.

“Liberty Formula One trades at a ~25% discount to the aggregate value of F1 teams despite significantly greater FCF generation and ownership of MotoGP. The sport has >800mn global fans and remains underpenetrated in the US (the most lucrative sports market) and Asia (the fastest growing). The cancellation of two Middle East races and concerns about margins post the latest Concorde agreement are reflected in the price, in our view. The race calendar resuming in Miami this weekend could re-ignite enthusiasm and drive further excitement around more opportunities with Apple, while the Liberty Investor Day around the LVGP in November could also serve as a catalyst later this year. While we are largely in-line with consensus for FY27 adj EBITDA at ~$1.4bn and FCF at ~$1.08bn, we believe numbers are de-risked and the multiple is too low,” Diffley opined.

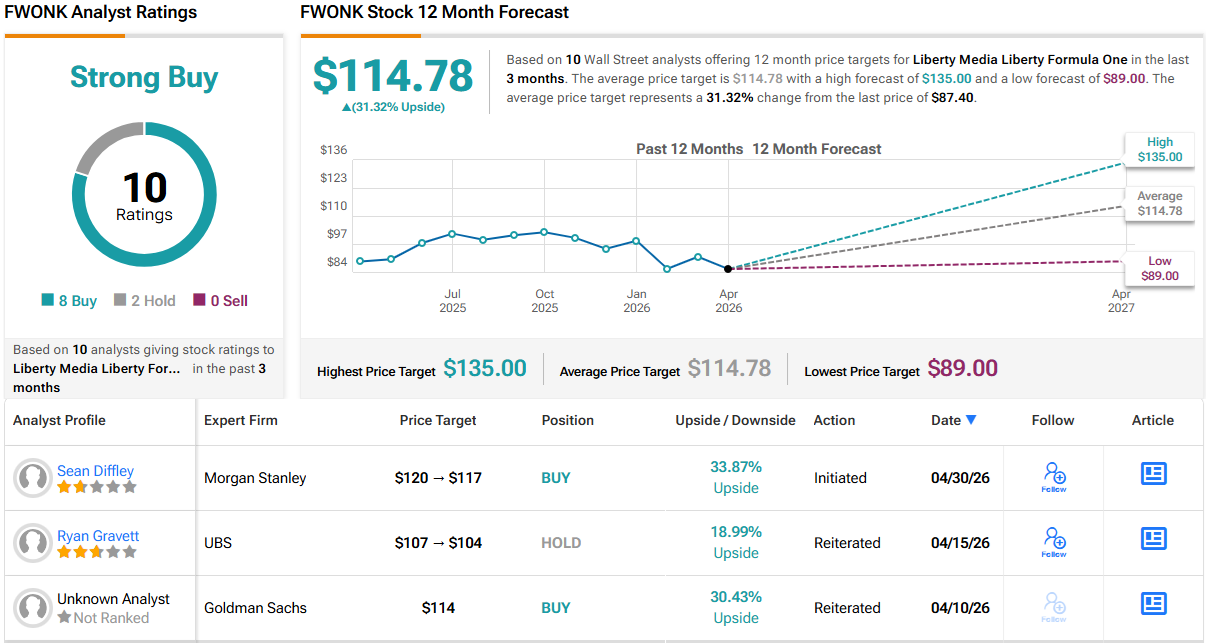

Quantifying his stance, Diffey rates FWONK stock as Overweight (i.e., Buy), and sets a $117 price target that implies a one-year gain of ~34%. (To watch Diffley’s track record, click here)

Overall, there are 10 recent analyst reviews on record for this stock, and the 8 to 2 split, favoring Buys over Holds, supports a Strong Buy analyst consensus rating. The shares are priced at $87.40 and have an average target price of $114.78, together indicating a 31% upside for the next 12 months. (See FWONK stock forecast)

TKO Group Holdings (TKO)

Next up is TKO Group Holdings, formed from the 2023 merger of two giants in the entertainment industry, the Ultimate Fighting Championship (UFC) and the legendary World Wrestling Entertainment (WWE). Today, TKO boasts that it reaches over 1 billion fans worldwide; features over 500 live events every year, drawing in over 3 million attendees; and can be experienced everywhere – the company has a presence in over 210 countries and territories around the world. TKO is a $14 billion enterprise, and in addition to WWE and UFC, its portfolio includes Professional Bull Riding (PBR) and the Zuffa Boxing professional promotion.

Live events and extreme sports are not the limit for TKO. The company also controls the IMG international sports marketing agency, which has been in the business for 65 years, and On Location, a leader in the worldwide market for experiential hospitality with over 20 years’ experience in bringing people to the best premium live events.

TKO’s chief business arms – UFC, WWE, and PBR – are together among the most popular sporting events in the world. UFC regularly brings in millions of viewers for its special TV broadcasts, while WWE has more than 1 billion followers on its social media platforms – including over 100 million subscribers on its YouTube channel. PBR, while not a combat sport, has a strong niche in the Western Lifestyle segment and has been expanding in recent years. The franchise reached 28 million viewers in the US last year.

That kind of reach brings in revenue, and in 4Q25, the last period reported, TKO’s revenue hit $1.04 billion. This was up 12% year over year and beat forecasts by $14.6 million. At the bottom line, the company reported a net loss of $0.03 per share, missing estimates by 25 cents as higher operating expenses, including increased SG&A costs and higher amortization tied to WWE media-rights accounting, weighed on profitability. The result compared unfavorably to the $0.38 positive EPS recorded in 4Q24. We’ll see the company’s next set of financial results today after market close.

For analyst Sean Diffley, the bigger picture remains intact. In his view, the core business is still highly durable, with long-term media agreements providing unusual visibility into future revenue streams while the company continues expanding into adjacent opportunities.

“TKO offers the one-two punch of highly visible and recurring core businesses from locking in multi-year media rights deals on the UFC and WWE, with relatively inexpensive call options on upside to their guidance on partnerships, site fees and Zuffa Boxing. EBITDA margins are approaching 40% this year and FCF conversion is best-in-class. 2026 is a self-proclaimed ‘year of execution’ after securing 2 historic US media rights deals with the UFC going to PSKY/CBS in a $7.7bn 7-year deal and WWE Premium Live Events (PLEs) going to DIS/ESPN in a $1.6bn 5-year deal, both of which increase the coverage, reach and popularity of the properties in the US. The company has outlined 2030 targets for Partnerships and Marketing of $1.2bn and Financial Incentive Packages (FIPs) / site fees target of $380-420mn by 2030, which appear to be conservative,” Diffley wrote.

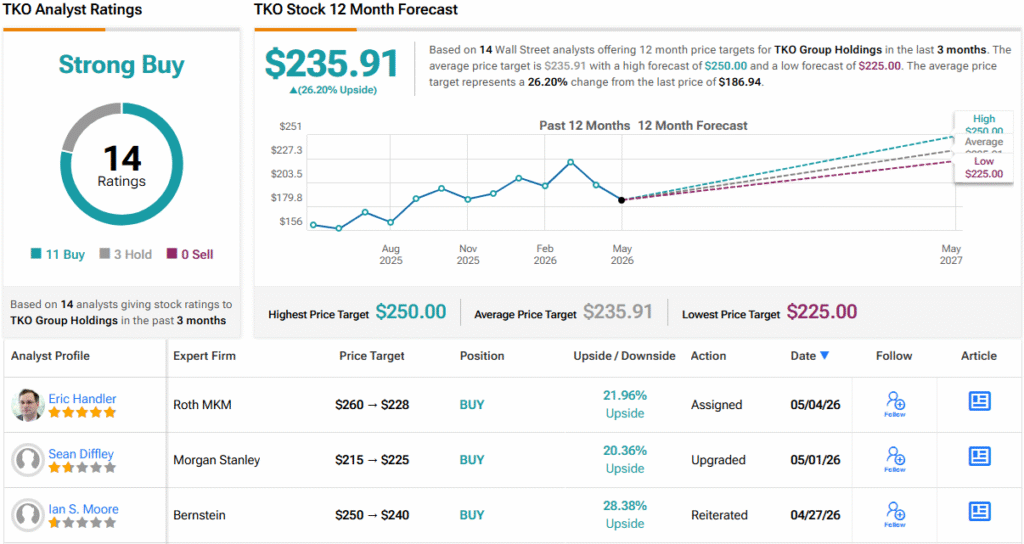

Looking ahead, the analyst sets an Overweight (i.e., Buy) rating on the shares, and gives the stock a $225 price target that suggests a one-year upside potential of 20%.

Overall, there are 14 recent analyst reviews on this stock, and they split to 11 Buys and 3 Holds for a Strong Buy consensus rating. The shares are priced at $186.94 and have an average price target of $235.91, implying that a 26% gain lies on the one-year horizon. (See TKO stock forecast)

Disclaimer: The opinions expressed in this article are solely those of the featured analyst. The content is intended to be used for informational purposes only. It is very important to do your own analysis before making any investment.