Amid ongoing macro uncertainty, Joyce Chang, Chair of Global Research at JPMorgan, says a more persistent force is shaping the market – AI. Rising investment and spending are driving earnings growth and supporting the broader market, particularly through continued buildout in data centers, cloud infrastructure, and related supply chains.

Meet Samuel – Your Personal Investing Prophet

- Start a conversation with TipRanks’ trusted, data-backed investment intelligence

- Ask Samuel about stocks, your portfolio, or the market and get instant, personalized insights in seconds

In fact, JPMorgan recently raised its S&P 500 target to 7,600, citing stronger AI-driven earnings expectations. Explaining the reasoning, Chang says, “I think the big story, and the reason we’re seeing markets at new highs, is the emergence of Anthropic’s ethos, which has really helped re-ignite a very bullish AI trade that has been the story all year. The S&P 500’s performance is increasingly tied to the AI theme – not just in terms of breadth, but also in how it’s expanding into other markets. It starts with data centers, where we’re looking at roughly $5 trillion in financing needs through the end of the decade, but it also extends to the broader buildout. It’s no longer just tech hardware and semiconductors. We’re now seeing this expand into small caps, credit markets, and even private markets.”

Against this backdrop, Mark Murphy, a senior software analyst at JPMorgan, is highlighting stocks with direct exposure to the theme. Using the TipRanks database, we’ve pulled two of his picks – familiar names worth a closer look.

Adobe, Inc. (ADBE)

We’ll start with one of the world’s leading software companies, Adobe. With a market cap of $101 billion, it plays a central role in content creation and digital publishing. Its PDF format is widely used, and its suite of tools for photo editing, web design, and graphic creation is deeply embedded across industries.

Adobe’s chief product is the Creative Cloud, the company’s subscription-based, full-service software package that includes all of these tools. The Creative Cloud is considered a professional standard by graphic designers, content editors, and online publishers, and its specific apps include Photoshop, Illustrator, InDesign, Acrobat, and Premiere Pro. In addition to the apps, subscribers can access Adobe’s resource libraries, with fonts, images, and other usable specialist items.

More recently, Adobe has been pushing deeper into AI. In late April, the company announced that its tools would integrate with Claude AI, allowing users to access Creative Cloud capabilities through AI-driven workflows.

In another expansion move, Adobe recently completed its previously announced acquisition of Semrush, a brand visibility platform. The deal, first disclosed last November, is aimed at integrating Semrush’s capabilities to support AI-driven tools and agents that enhance users’ branding efforts.

AI has been big business for Adobe recently, and in the company’s fiscal 1Q26 report, Adobe noted that its AI-first annual recurring revenue has tripled over the past year. Total revenue, at $6.4 billion, was a company record, up 12% year-over-year, and beat the forecast by $120 million. At the bottom line, Adobe’s non-GAAP EPS of $6.06 was 19 cents per share better than had been expected.

Yet, Adobe shares are down about 28% this year as concerns that AI could erode its core business model weigh on the stock, with cheaper and more automated design tools raising the risk of lower demand for its subscription-based products.

For JPM’s Mark Murphy, the pressure reflects near-term uncertainty rather than a break in the thesis, as he continues to point to Adobe’s strong industry position and long-term ability to monetize AI.

“We continue to lean favorably on Adobe fundamentals given its fairly durable growth rates, incremental AI monetization opportunities over time, and largely favorable customer and partner checks, while acknowledging a rapid pace of technological change and early-stage experimentation with AI pricing models. We remain impressed by a fast pace of innovation as Adobe continues to build an end-to-end tapestry of creative tools, positioning it well for IT vendor consolidation efforts, with emerging growth catalysts developing in the long run alongside an elite profitability structure and well-diversified, scaled install base,” Murphy noted.

Murphy backs that view with an Overweight (i.e., Buy) rating on ADBE, alongside a $420 price target, pointing to a potential 67.5% upside over the next year. (To watch Murphy’s track record, click here)

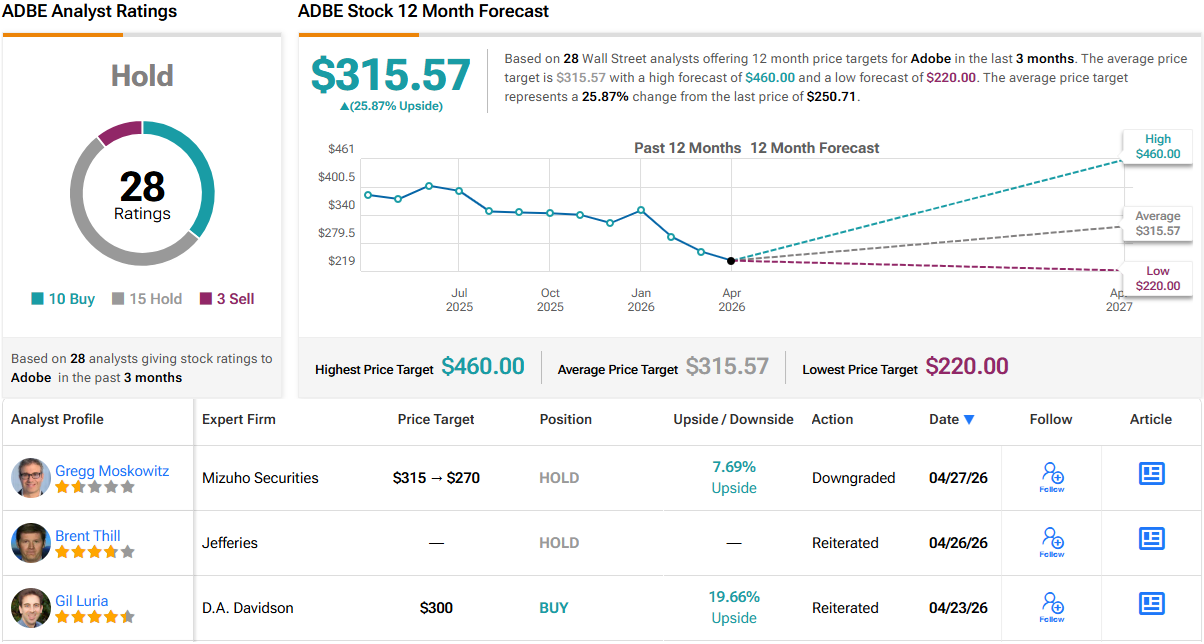

Across the Street, however, sentiment is more balanced. Based on 28 recent analyst reviews, the stock carries a Hold (i.e., Neutral) consensus, with 10 Buys, 15 Holds, and 3 Sells. At the current price of $250.71, the average price target of $315.57 points to a still-meaningful 26% upside over the coming 12 months.(See ADBE stock forecast)

Salesforce (CRM)

Next under the JPM microscope is Salesforce, the industry leader in CRM and a survivor of the dot.com bubble of the late 90s. Salesforce has long been known for its suite of software tools, all designed to put customer relationship management on a new footing. The company was a leader in cloud-based subscription software services, and today, its Agentforce platform brings humans and agentic AI together to modernize the CRM tool suite. Through Agentforce, Salesforce provides users with autonomous AI, unified data, and its Customer 360 apps on a single integrated platform.

Bringing AI into the picture did not change Salesforce’s essence, which is its expertise in CRM. The company has built up a successful record over more than 25 years, and it is known for its quality tools in data management, marketing, online commerce, sales, and customer service. All of this is done on the cloud, which minimizes infrastructure on the user end.

What the addition of AI did do was keep Salesforce at the leading edge of its field. The company’s agentic AIs are designed to work with the human workforce, bringing a 24/7 digital capability that supplements, rather than replaces, human agents. The effect is to put an unlimited customer service force into play, matching the fast pace of action in the digital economy.

Earlier last month, Salesforce announced that it is deepening and expanding an existing AI partnership with Google Cloud, a move that will permit agentic AIs to execute complete workflows on the Slack and Workspace tools, while Agentforce and Gemini together provide behind-the-scenes intelligence and context. The aim is to eliminate context switching and data loss as users and agents work across systems.

On the financial side, Salesforce released its fiscal 4Q26 results in February and showed a top line of $11.2 billion, up 12% year-over-year and $9.4 million better than had been anticipated. The company’s bottom line figure of $3.81 represented a non-GAAP EPS that beat the forecast by 76 cents per share. Free cash flow in the quarter rose year-over-year from $3.8 billion to $5.3 billion.

However, Salesforce shares are down 31% this year as concerns grow that AI could disrupt its core business model, with worries that automation may reduce demand for seat-based SaaS products adding pressure.

Against that more cautious backdrop, JPMorgan’s Mark Murphy has taken a closer look at the stock and remains generally impressed with the company.

“We maintain our view that Salesforce has transformed into a highly profitable and cash-generative business, and we continue to see eventual upside from current levels as the company balances growth with profitability and FCF generation while infusing Generative AI capabilities into its clouds. We view FCF/Sh as the appropriate lens for the company and believe the thesis should remain intact as Salesforce continues to grow, albeit at a slower rate, and show meaningful Op margin expansion, which should be tracked by FCF margin over time,” Murphy noted.

On that basis, Murphy assigns CRM an Overweight (i.e., Buy) rating, with a $320 price target that implies a potential one-year gain of 74%.

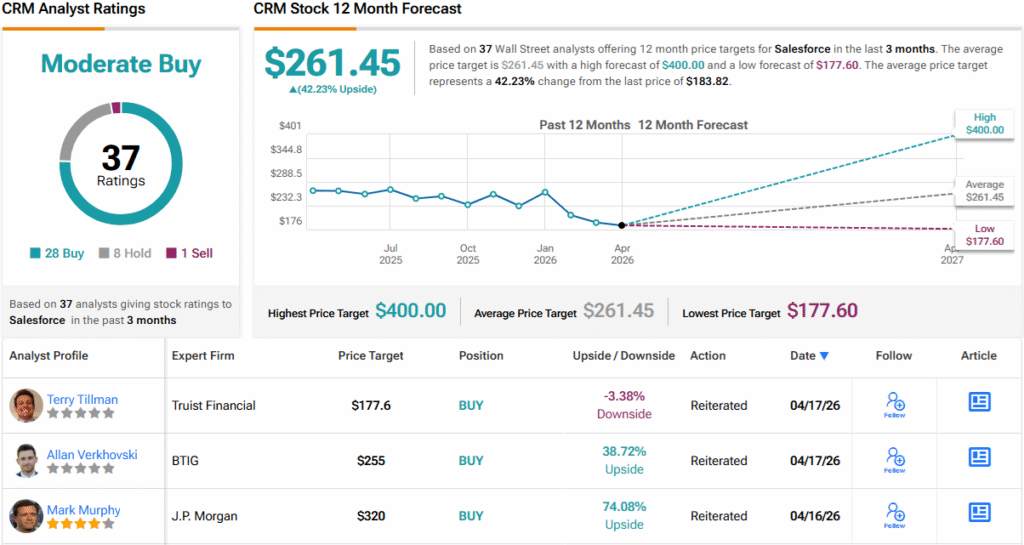

For the Street as a whole, CRM gets a Moderate Buy rating, based on 37 reviews, with a breakdown of 28 Buys, 8 Holds, and 1 Sell. The stock’s $183.82 selling price and $261.45 average target price together indicate a one-year upside potential of 42%. (See CRM stock forecast)

Disclaimer: The opinions expressed in this article are solely those of the featured analyst. The content is intended to be used for informational purposes only. It is very important to do your own analysis before making any investment.