Nebius Group (NBIS) stock has already delivered an extraordinary rally over the past 12 months, but I don’t think the bull case is exhausted yet. As demand for artificial intelligence (AI) continues to outpace available computing capacity among hyperscalers and model builders, Nebius has positioned itself to capitalize on one of the most significant bottlenecks in the AI infrastructure market.

Meet Samuel – Your Personal Investing Prophet

AMZO: built for a short position on AMZNAs I see it, the main reason NBIS stock has more room to run is that the Dutch-based AI-centric cloud platform has been able to convert capital into connected power and monetized capacity at an unusually fast pace. All signs point to this continuing this year and next. While funding and dilution remain real risks, the company’s ability to grow revenue and annualized recurring revenue per share should continue to justify a bullish view on the stock.

Why Nebius Sits at the Center of the AI Compute Shortage

Perhaps one of the most frequently repeated messages in recent earnings calls from hyperscalers like Amazon (AMZN), Microsoft (MSFT), Alphabet (GOOGL), and Oracle (ORCL) is that AI demand continues to outpace available supply. Nebius exists precisely to help solve that bottleneck.

In practice, Nebius acts as a safety valve for excess demand for computing power. The company offers customers access to dedicated AI data centers, next-generation graphics processing units (GPUs), secured power, and computing capacity that can be deployed on much shorter lead times.

In a market constrained by supply rather than demand, this matters enormously. If Nebius can convert capital into connected megawatts (MW) faster than its competitors, it can capture a meaningful portion of that pent-up demand. In my view, that is the essence of the Nebius thesis. Capital velocity is the company’s moat, and the most important metric to monitor is how quickly it can turn invested capital into connected MW and, ultimately, monetized Annual Recurring Revenue (ARR).

Execution Is Moving at Full Speed

So far, judging by the stellar performance of its stock price over the past 12 months, all signs point to Nebius executing at an exceptionally fast pace — possibly faster than most independent competitors.

In fact, in Q1, Nebius showed that it is effectively securing power, land, and contracts at a very rapid pace. First, the company delivered on the capacity commitments made to clients such as Microsoft and Meta Platforms (META). Then, it reiterated its target of 800 MW to 1 GW of connected power by the end of 2026, representing an expansion of roughly four to five times the approximately 220 MW expected by the end of 2025. It has already surpassed 3.5 GW of contracted power, exceeding its previous target of 3 GW, and has also raised its guidance to more than 4 GW by the end of 2026.

Furthermore, the guidance to reach $3–$3.4 billion in revenue in 2026, along with $7–$9 billion in ARR, essentially implies roughly $7–$11 million in ARR per connected MW by year-end 2026. In this case, the bull case — assuming that Nebius delivers 1 GW of connected power and is able to monetize it at $11 million in ARR per MW — would imply an annualized revenue run-rate of approximately $11 billion by the end of 2026.

The Market Is Already Betting on the High End

If Nebius’s level of activity remains stable throughout 2027, $11 billion in ARR by the end of 2026 would represent approximately the theoretical ceiling for FY2027 annual revenue. Consensus currently estimates FY2027 revenue at $10.9 billion, which suggests to me that the market is already anticipating Nebius reaching the higher end of its guidance.

That said, this would imply Nebius trading at a price-to-sales multiple of 4.6x FY2027 revenue, slightly above the industry average of 3.7x. Still, I believe that valuation is plausible given the competitive moat embedded in Nebius’s business model.

The Funding Question at the Heart of the Thesis

The main point of tension in the thesis, however, relates to funding. Expanding capacity by roughly four to five times in just over a year requires massive capex investments. In Nebius’s case, the company is guiding for $20–$25 billion in capex in 2026, which is roughly 600%-800% of revenue guidance for the same year.

The issue is that, in order to fund this expansion, Nebius has relied on the capital markets. In September 2025, the company completed a $1 billion Class A share offering, followed in November by an at-the-market program for up to 25 million additional Class A shares. More recently, the company also raised capital through convertible debt and warrants linked with Nvidia (NVDA).

Nebius has diluted shareholders by approximately 6.4% since the lowest point in its share count in 2025. This trend is likely to continue throughout 2026, as management has already indicated, although the company also expects to rely heavily on customer prepayments.

The market does not appear overly concerned about the dilution because, in this case, it appears to be value-accretive. ARR per share could grow by triple digits in 2026, which would more than offset the increase in the share count. As a result, there is still room for additional upside, provided that ARR per share continues to grow comfortably faster than dilution.

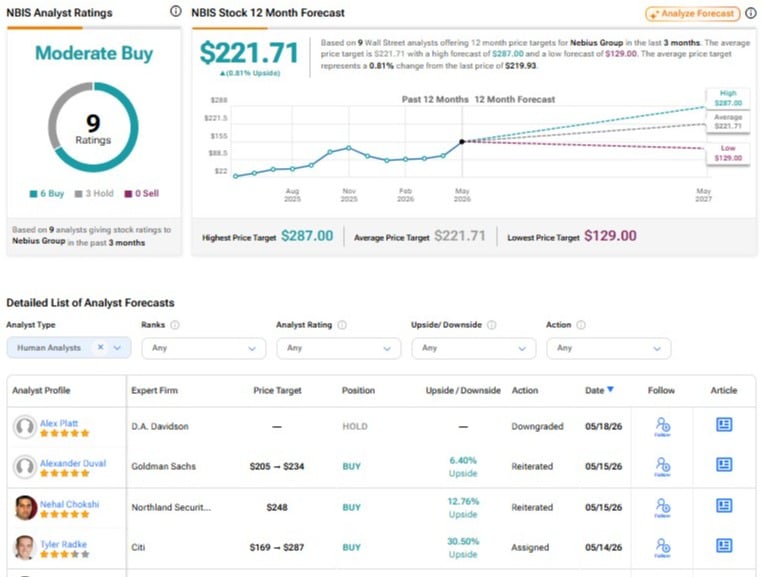

Is NBIS a Buy, According to Wall Street Analysts?

Nebius shares are currently rated a Moderate Buy based on Wall Street consensus. Of the nine analyst ratings issued over the past three months, six are Buys and three are Holds. The average price target for NBIS is $221.71, implying approximately 0.81% upside from the current share price.

Nebius Continues to Capitalize on a Massive Opportunity

I still view the Nebius thesis through a bullish lens. Even though the stock has performed extremely well over the past 12 months, I believe Nebius’s unique position to capitalize on a key bottleneck in AI infrastructure will continue to drive strong growth in ARR per share and, consequently, in the company’s valuation.

Funding will remain the primary focus, along with execution. However, I believe both risks are partially mitigated by the concrete evidence we have already seen. After all, Nebius has demonstrated that it can raise capital, deliver capacity, and monetize that capacity quickly — and appears positioned to continue doing so.