Generative AI has reinvigorated energy discourse and Vistra Corp. (VST) is in the middle of the bullish narrative. Appreciably ahead of the S&P 500 Utilities index YTD performance of approximately +24%, Vistra stock has risen more than 200% during the same period. Following last week’s 11% price correction, there is still time to adopt exposure to economic cycle-resistant Vistra stock ahead of the presidential election and the Q3 2024 earnings release scheduled for November 7th. I believe there is more upside potential.

Claim 30% Off TipRanks

- Unlock hedge fund-level data and powerful investing tools for smarter, sharper decisions

- Discover top-performing stock ideas and upgrade to a portfolio of market leaders with Smart Investor Picks

Preparing for the Energy-Loaded Future

On Thursday’s appearance at the Detroit Economic Club, former President Trump noted that his administration, if elected, would double the nation’s electricity capacity by removing bureaucratic and environmental barriers. Regardless of who wins the U.S. election, it is certain that other countries like China have drastically accelerated their own power-generating capacity in a push to handle increasing demand.

China is actually expected to represent 60% of the world’s renewable capacity by 2030, according to the IEA. It also has 27 nuclear reactors presently under construction, more than any other country. The stakes are perfectly clear. Any nation that cherishes a competitive economy, and therefore a geopolitical edge, must have abundant and cheap energy. Germany, for example, suffered an economic downturn following the sabotage of the Nord Stream pipelines.

Today we investigate what role Vistra will play in the world’s energy supply.

Vistra’s Expanded Portfolio

Based in Texas, Vistra holds around 41,000 MW of capacity that powers 5 million residential, commercial and industrial retail customers. Although mainly concentrated in Texas, the company covers 18 states with the second largest nuclear power fleet in the United States. I’m bullish on Vistra’s positioning.

As of October 2024, Vistra’s power generation capacity is comprised of 60% gas, 20% coal, 15% nuclear and 4% renewables. In the last two years, the company has acquired Tricor Group, Energy Harbor and Vistra Vision LLC — the latter deal is not yet closed.

Altogether, these acquisitions added $13 billion worth of assets to Vistra’s energy portfolio. After receiving favorable approvals under the existing Biden admin and the Inflation Reduction Act (IRA), Vistra has elevated its nuclear capacity to over 6,400 MW.

How Does Vistra Secure Profitability?

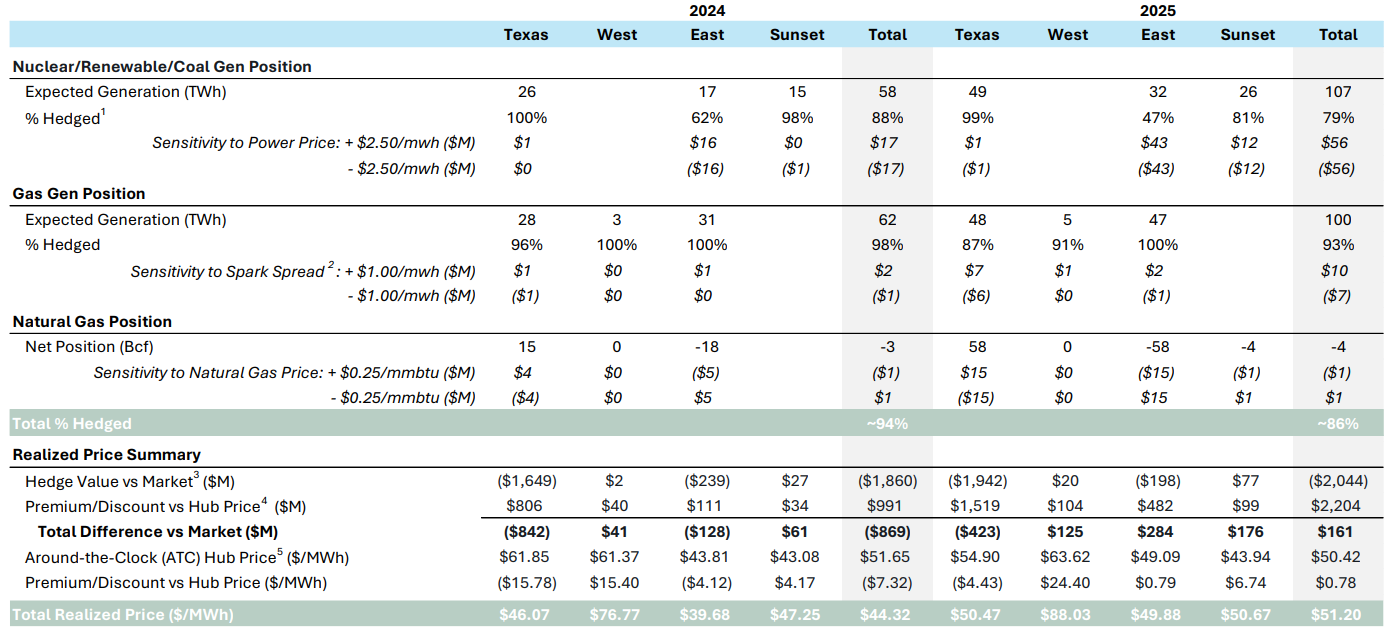

Given that fuel costs are often subject to volatility, utility companies often resort to hedging programs in order to lock in prices and power sales via futures, options or forward contracts. For the remainder of 2024, Vistra has hedged 94% of earnings to secure predictable cash flows, having generated a record $1.4 billion of adjusted EBITDA in Q2 2024.

Since April 2020, the average price of electricity in U.S. cities has increased by almost 35%. According to the IEA’s Short Term Energy Outlook (STEO) published on Tuesday, electric power demand will reach a record high of 4,163 billion kWh in 2025, versus 4,000 billion kWh back in 2023.

Despite the renewables push, the main sources of power largely remain the same. IEA projects gas contribution to decrease from 42% in 2024 to 39% in 2025, while coal’s share should slip from 17% to 16%. Renewable energy, which is Vistra’s smallest power source, is only expected to increase by 2%, from 23% to 25%.

In the meantime, Vistra is 86% hedged for 2025 and 55% hedged for 2026. On top of the production tax credit (PTC) as a federal incentive for nuclear power, Vistra is looking for an extra $400 million tax credit in 2024 (excluded from outlook).

Having acquired Vistra Vision and 6,400 MW of new nuclear capacity, the company expects more PTC-driven revenue figures moving forward. In its Q2 2024 earnings report, Vistra raised its 2025 adjusted EBITDA midpoint guidance from $4.55 – $5.05 billion to $5.2 – $5.7 billion.

Data Centers and Texas Advantage

Due to unfavorable regulations, heavy taxation, security issues and high electricity rates, many tech companies are moving from California. That includes companies like Tesla (TSLA), SpaceX, Hewlett Packard (HPQ) and Oracle (ORCL). All of these companies have moved their headquarters to Vistra’s home state of Texas, which is a very favorable development.

Although California remains the U.S. tech hub, the migration trend is obvious. With that trend comes increased demand for data centers powering AI products. The IEA expects a 60 TWh increase in electricity consumption for data centers by 2026, representing ~4% to 6% of total U.S. electricity demand.

Vistra has made strategic partnerships, having already signed two renewable power purchase agreements (PPAs) with Amazon (AMZN) and Microsoft (MSFT) worth 600 MW of electricity. From this burgeoning sector, Vistra expects a 35 GW demand rise from 2023 to 2030.

Moreover, for the electrification of the Permian Basin, located in western Texas and southeastern New Mexico, Vistra expects an additional 20 GW of demand. Given that it takes time to build new power plants, especially nuclear, it is reasonable to predict that Vistra will continue to reap PTC benefits at even greater levels. If former President Trump wins his second term in this year’s election, it is likely that Vistra will accelerate its pilot programs in the deployment of small modular reactors (SMRs).

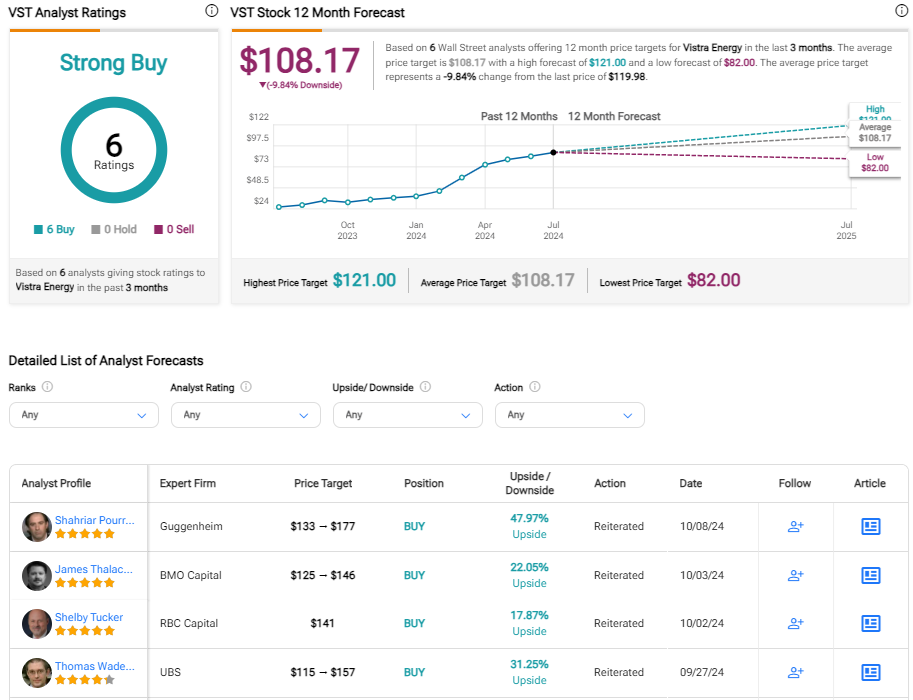

Is Vistra a Buy According to Wall Street Analysts?

At a current stock price above $120/share, VST stock is nearly double its 52-week average of $66.51, but still meaningfully below the 52-week high of $143.87 per share. Of the six Wall Street analysts who have issued ratings on VST over the past 3 months, all six have a Buy rating. There are no current Hold or Sell ratings. The average VST price target is actually $108.17 per share, about 10% below the recent market price.

Investors should be reminded that Vistra has approved $2.25 billion worth of stock buybacks, which could support the share price.

Conclusion

Already enjoying defensive qualities as a utility company, Vistra is bound to be a beneficiary of the data center drive and the tech exodus from California. Moreover, the shift toward nuclear power gives Vistra more leverage while securing PTC tax credits.

Additionally, Vistra’s expansion into renewables and energy storage is yet to pay dividends. Although bullish investors have already pushed VST stock higher on these business opportunities, I believe there’s room for VST shares to rally further. I hold a bullish view of Vistra Corp. stock.