Berkshire Hathaway (BRK.B) looks like a Buy ahead of its Q1 earnings in early May, with three key drivers starting to come into focus. Accelerating buybacks, early signs of recovery at Burlington Northern and Santa Fe (BNSF) Railway, and the company’s ability to deliver consistent, low-volatility returns all support a more constructive outlook than the market is pricing in. While Berkshire is not typically driven by near-term catalysts, this combination could support further upside going into earnings.

Claim 55% Off TipRanks

Trade ARKK with leverageAgainst that backdrop, to beat consensus, the company will need to deliver earnings per share (EPS) above the current‑quarter consensus of approximately $5.05 and revenue above roughly $90–$93 billion, reflecting modest growth versus the prior‑year quarter. I rate the stock a Buy.

Buybacks as the Next Driver of Per-Share Value

Greg Abel, the successor to Warren Buffett after 60 years at the helm of Berkshire Hathaway, made it clear in his first shareholder letter that he doesn’t plan to change the company’s value investing philosophy.

He did, however, signal that the pace of execution could evolve. Share buybacks could be the first place where that shows up. Berkshire has always emphasized that it only repurchases shares when the price is below its own estimate of intrinsic value.

While Abel hasn’t explicitly signaled a change in the buyback policy, the combination of recent actions and the current setup is worth paying attention to. It points to a subtle yet potentially very meaningful shift. Market activity in early March suggests Berkshire may have quietly resumed buybacks after a long pause. On top of that, Abel himself bought about $15.3 million worth of shares, which reinforces the idea that the stock is trading below intrinsic value.

At the same time, Berkshire is sitting on roughly $373 billion in cash, around 37% of its market value, mostly parked in Treasuries and cash equivalents that are clearly under-earning.

If even part of that gets redirected into buybacks, as Abel’s stance seems to allow, the impact is pretty straightforward: fewer shares outstanding means higher earnings per share. Even without underlying growth, that alone lifts value per share. More importantly, it still preserves the flexibility to deploy cash when real opportunities — or crises — show up.

Breaking Down Berkshire’s Two Halves: Operations and Investments

Recognizing that Berkshire Hathaway is essentially a mix of insurance — its core business — energy, railroads, and a broad set of operating companies — helps isolate the pieces. On the investment side, Berkshire holds a sizable portfolio of equity investments, including its roughly $62 billion stake in Apple (AAPL), which remains its largest single‑stock holding even after recent trims.

On the operating side, the company is built around insurance as its central underwriting engine, with large contributions from energy, primarily Berkshire Hathaway Energy, and railroads, or BNSF.

BNSF as an Underappreciated Source of Earnings Upside

I want to zoom in on BNSF Railway. Acquired in 2010 for $34.5 billion, it remains one of the company’s largest operating businesses. This is often an overlooked part of the Berkshire thesis. It is considered “old economy” and has lagged behind peers like Union Pacific (UNP). It isn’t growing much and has basically faded into the background.

However, precisely because the market doesn’t pay much attention to this segment, surprises can come from it. In recent years, BNSF has lagged on margins and efficiency, largely because it avoided adopting Precision Scheduled Railroading (PSR). That model typically involves cost-cutting, headcount reductions, and route optimization.

Now that’s starting to change. The company is moving toward a cost restructuring with more operational flexibility and workforce adjustments. The impact is already showing up in expectations for 2025. Operating margins are modeled to rise toward the mid‑30% range from roughly 26%–27% in 2024, reflecting expectations for continued operating leverage across Berkshire’s portfolio. According to Berkshire, every 100-basis-point improvement in margin adds about $230 million in incremental cash.

Assuming, in an illustrative scenario, that each 100‑basis‑point margin improvement generates about $180 million in incremental after‑tax profit, this would translate to roughly $0.12 per share at Berkshire’s current Class‑A‑equivalent share count of about 1.45 million shares, with 1 Class A share convertible into 1,500 Class B shares. Under that same model, a 300‑basis‑point margin expansion could add roughly $0.35–$0.40 in incremental EPS. For context, Berkshire missed its FY2025 EPS consensus by about $0.46 per share — so this isn’t trivial.

Against Tech, Berkshire Holds Up Better Than Expected

Berkshire Hathaway is often seen as out of sync with the tech-driven market, despite its large stake in Apple. However, the past five years tell a different story. Despite lagging during periods of excessive speculation, Berkshire’s shares have actually outperformed tech-focused ETFs like ARK Invest’s (ARKK) — and have done so with significantly lower volatility.

That being said, the roughly 1.4x book value at which BRK.B trades today may not look particularly attractive at first glance. It becomes more reasonable when viewed through the lens of return quality. The market is paying not only for the assets on the balance sheet, but also for a business model that can compound more consistently over the cycle, with lower volatility and better downside protection.

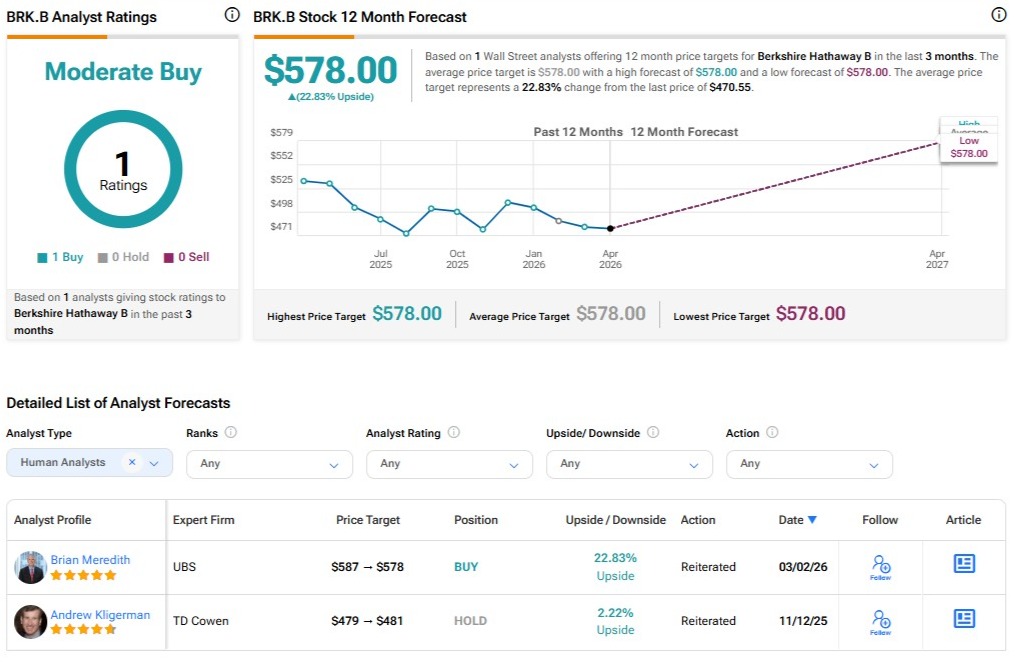

Is BRK.B a Buy, According to Wall Street Analysts?

There aren’t many analysts covering Berkshire Hathaway on Wall Street. Over the past three months, only Brian Meredith from UBS (UBS) has rated BRK.B a Buy, which still results in a Moderate Buy consensus. According to the analyst, his $578 price target, recently lowered from $587, implies about 22.83% upside from current levels.

A Confluence of Value Drivers

From a broader perspective, share buybacks could become a meaningful new driver of earnings per share, while BNSF is starting to show signs of recovery that the market arguably hasn’t yet priced in. At the same time, Berkshire — guided by the value-investing philosophy of Warren Buffett and Charlie Munger — continues to deliver more consistent returns with lower volatility, even in a market dominated by the tech narrative.

Overall, it’s a combination of smaller value drivers adding up. With that in mind, I see Berkshire Hathaway as well-positioned heading into Q1, and I see the stock as a Buy.