Earlier today, WELL Health Technologies (TSE: WELL) updated investors by providing preliminary results for its upcoming Q2-2022 earnings report. WELL Health expects robust Q2 results, including record quarterly revenues of over C$130 million. For context, revenue in Q2 2021 was just C$61.8 million, implying that the company grew at least 110% year-over-year in Q2 2022.

Claim 30% Off TipRanks

- Unlock hedge fund-level data and powerful investing tools for smarter, sharper decisions

- Discover top-performing stock ideas and upgrade to a portfolio of market leaders with Smart Investor Picks

This growth can be attributed to several factors, including a 50% year-over-year increase in total omnichannel patient visits (7% sequential growth) and WELL’s rapidly-growing U.S. businesses.

Two of WELL’s businesses, Wisp and Circle Medical, had a combined revenue run-rate of over C$115 million in June 2022. This is an improvement from the C$110 million revenue run-rate from last month and represents growth of more than 150% on a year-over-year basis.

The high growth does not come with unprofitability, as these two businesses generate positive adjusted EBITDA. Also, WELL Health expects C$23 million of adjusted EBITDA and C$15 million of shareholder free cash flow for the quarter ended June 30, 2022. In addition, CRH Medical (owned by WELL Health) delivered record results and organic growth, completing 125,160 patient cases for the quarter.

While the update should be viewed positively by investors, the stock only finished 1.2% higher today, which is not much for a stock as volatile as WELL Health.

Investors on TipRanks Seem Pessimistic About WELL Health

Despite WELL Health’s positive developments lately, investors who hold portfolios on TipRanks seem to view the stock negatively for the most part. Out of the 545,939 portfolios tracked by TipRanks, 0.2% hold WELL stock.

In addition, in the last 30 days, the number of TipRanks portfolios holding WELL stock dropped by 0.6%. In the last seven days, this number dropped by 0.5%. As a result, the stock’s sentiment is below the sector average, as demonstrated in the following image:

However, the average portfolio weighting allocated towards WELL Health among those who do have a position is 5.3%, which is respectable. Having a single stock make up more than 5% of a portfolio shows that there is some sort of conviction there in those that do hold the stock. However, it’s not a very high figure either.

Analysts Have the Opposite Opinion of TipRanks Investors

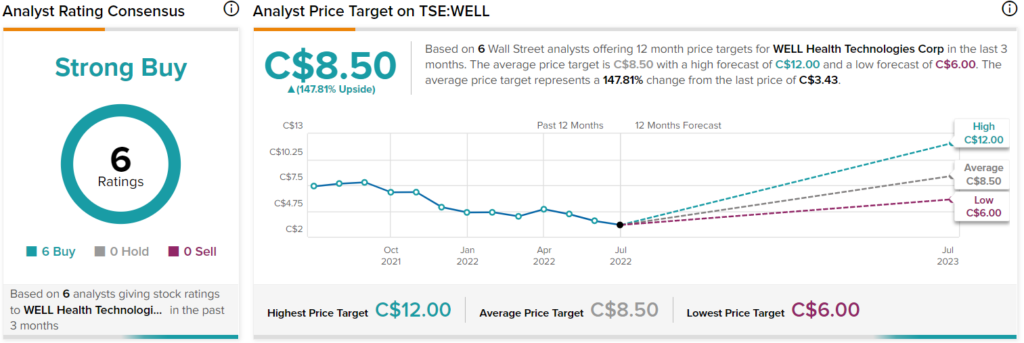

WELL Health earns a Strong Buy consensus rating from analysts. This is based on six unanimous Buy ratings assigned in the past three months. The average WELL Health price target of C$8.50 implies 147.8% upside potential. Analyst price targets range from a low of C$6 to a high of C$12.

Four of the six Buy ratings came from top Wall Street analysts. Rob Goff, ranked #132 out of 20,860 overall experts, is one of them. Goff gave WELL Health a C$11 price target three months ago.

Conclusion: WELL Health is Looking Healthy

WELL Health is continuing to expand its business at a rapid clip while maintaining positive adjusted EBITDA and free cash flow. Not many companies are able to grow by triple-digit percentages without sacrificing profits.

While WELL Health grows quite a bit through acquisitions, it also has solid organic growth, giving it a nice balance. WELL’s stock saw a muted response today, but, nonetheless, the news was positive for long-term investors.