Hologic (HOLX), the medical device company focused on women’s health, has still failed to particularly excite Wall Street analysts despite accepting a new $18.3 billion acquisition offer.

Claim 55% Off TipRanks

- Unlock hedge fund-level data and powerful investing tools for smarter, sharper decisions

- Discover top-performing stock ideas and upgrade to a portfolio of market leaders with Smart Investor Picks

Alternative asset manager Blackstone (BX) and private equity firm TPG (TPG) on Tuesday disclosed their offer to take the Massachusetts-based company private at a $76 per share upfront cost. The arrangement came with an additional $3 per share if Hologic’s global breast health business hits specific revenue targets over its next two fiscal years.

In addition, the agreement includes a 45-day window during which Hologic can shop around for better offers.

However, analysts from Raymond James (RJF), Leerink Partners, Needham, JPMorgan Chase (JPM), William Blair, and Stephens between Tuesday and Wednesday slammed Hold ratings on HOLX stock.

The Hold ratings continue Wall Street’s cautious approach to the company before the final offer was announced.

Why Are Analysts Still Holding Back?

Despite the Hold ratings, some analysts see the deal as beneficial for Hologic.

While Raymond James analyst Andrew Cooper described it as “a positive outcome for shareholders”, Leerink Partners analyst Puneet Souda noted the offer “makes sense” due to Hologic’s struggle with investors about its low-growth business segment. Souda believes the acquisition offers an opportunity for multiple businesses to be spun out of Hologic.

However, both Cooper and Souda noted that Hologic is unlikely to find a higher bidder, and the former even sees a limited upside to HOLX stock if the acquisition is completed.

Furthermore, Souda argued that Hologic’s breast health business — which accounts for about 40% of its revenue — continues to be plagued by several challenges that will delay its return to mid-single-digit growth. William Blair analyst Andrew Brackman echoed a similar sentiment in his analysis.

Chipping in, Needham analyst Michael Matson observed that the offer reflects a lower valuation multiple — meaning that investors are paying less for each unit of the company’s earnings — compared to peers in the large-cap MedTech market. However, Matson sees this as justified due to Hologic’s slower growth rate.

Is HOLX a Good Buy?

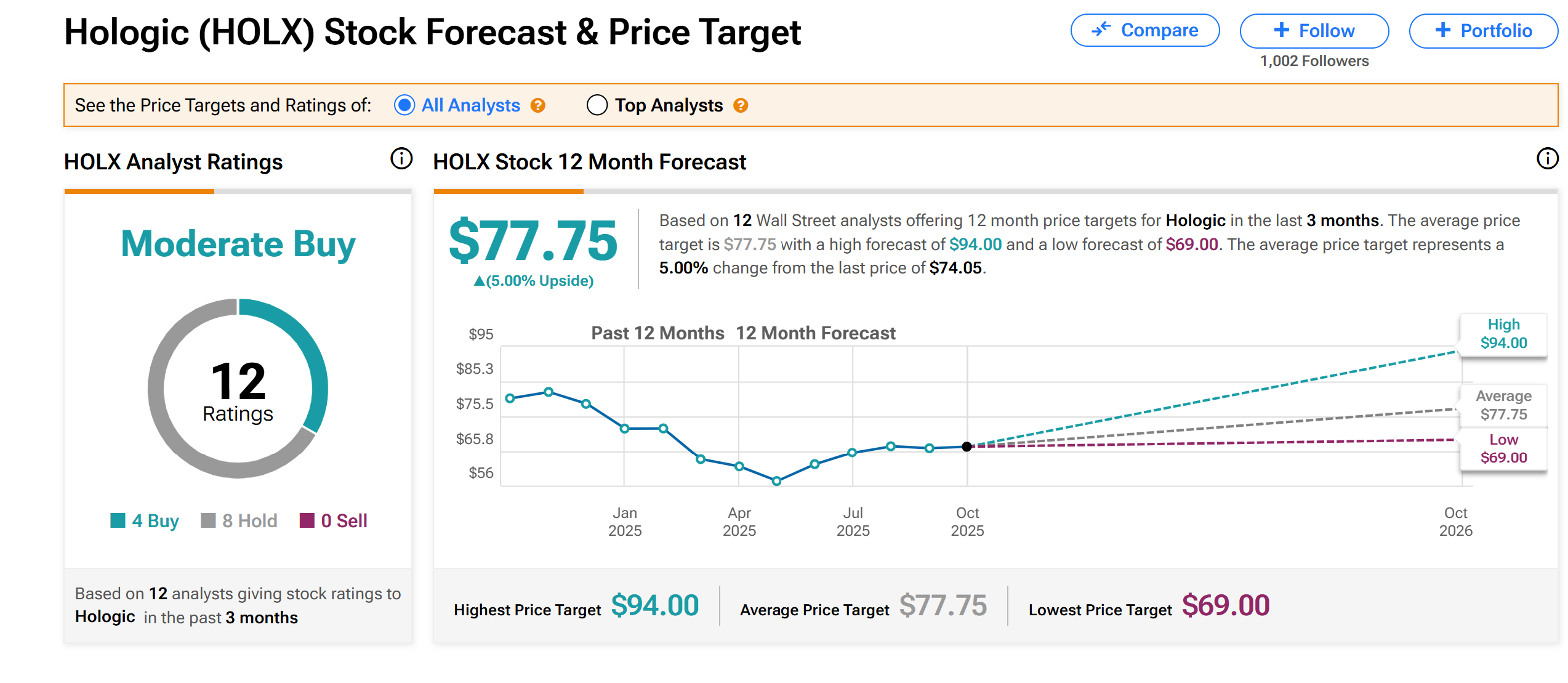

Across the larger Wall Street, Hologic’s shares continue to hold a Moderate Buy consensus rating based on four Buys and eight Holds assigned by 12 analysts over the last three months. However, the average HOLX price target of $77.75 indicates a 5% upside potential from the current level.