Shares of used-car company Carvana (CVNA) have taken investors on a roller coaster ride since going public in 2017. Carvana priced its IPO at $15, and the stock soared to a record high of $361 in August 2021. The bear market in 2022 drove CVNA stock to less than $5, and shares have rallied a monstrous ~2,800% since the start of 2023. Nonetheless, I am cautiously bullish on CVNA stock due to its improving profitability, steady revenue growth, and massive addressable market.

Claim 55% Off TipRanks

- Unlock hedge fund-level data and powerful investing tools for smarter, sharper decisions

- Discover top-performing stock ideas and upgrade to a portfolio of market leaders with Smart Investor Picks

An Overview of Carvana

Valued at $15.1 billion by market cap, Carvana operates an e-commerce platform for buying and selling used cars in the U.S. It allows customers to look for vehicles and inspect them using 360-degree vehicle imaging technology, obtain financing and warranty coverage, and purchase the vehicle.

A Focus on Margin Expansion

Carvana delivered its best financial results in company history, reporting an adjusted EBITDA (earnings before interest, tax, depreciation, and amortization) margin of 7.7% and a net margin of 1.6%. In terms of its EBITDA margin, Carvana claims to be the most profitable public automotive retailer in the U.S.

Additionally, Carvana returned to revenue growth, increasing sales by 17% year-over-year despite reduced marketing spending and constrained inventory. The company emphasized that it reported a positive net income for the third consecutive quarter, with its adjusted EBITDA exceeding capital expenditures and interest expense for the first time ever in Q1 of 2024.

With sales of $3.06 billion, Carvana’s EBITDA stood at $235 million. Capital expenditures were $18 million, and cumulative interest expenses were $172 million.

According to Carvana, it managed to achieve record sales and profit margins amid a weak macro environment that challenged unit economics and volume. Its national inventory, coupled with a tech-enabled transaction platform integrated with a new supply chain, has allowed it to conduct operations efficiently in a low-margin sector.

For instance, Carvana reported a GAAP (generally accepted accounting principles) operating income of $134 million in Q1, even as retail used vehicle sales fell 10% compared to 2019. It also returned to sales growth in the March quarter after posting six consecutive quarters of declines.

Revenue Growth and a Massive Market

According to a report from Mordor Intelligence, Carvana is part of the U.S. used-car market, which was forecast to grow from $195.84 billion in 2021 to $302.47 billion in 2027. For context, Carvana’s sales totaled $11.22 billion in the past 12 months, meaning it still has plenty of room to grow.

While the used-car market in the U.S. is forecast to grow by more than 7% annually over the next five years, Carvana’s sales are forecast to grow by 15.7% to $12.46 billion in 2024 and by 14.2% to $14.23 billion in 2025.

Carvana is growing at a far higher pace than the broader market. If it can account for 10% of the market by 2027, annual sales should surge to $30 billion in the next four years.

Risks: Cyclicality, Profit Margins, and Debt

A tech-based model has meant that Carvana has focused on delivering a better car-buying experience for its customers compared to legacy brick-and-mortar players. However, investing in the company carries certain risks.

First, Carvana is part of a cyclical sector, making it sensitive to macro factors such as interest rate hikes and consumer spending. While interest rate cuts are forecast to begin this September, the Fed might be compelled to reverse its stance if inflation raises its ugly head once again.

Second, Carvana has yet to gain investor confidence, given its extremely low net income margins, which suggests that potential shareholders should remain cautious about the company’s long-term prospects.

Third, Carvana is not completely out of the woods, even though it underwent a debt restructuring process in 2023. It ended Q1 with $172 million in interest expenses, higher than its GAAP operating income of $134 million. It suggests Carvana is not generating enough profits to service its debt and might be forced to raise additional capital, leading to shareholder dilution or higher debt.

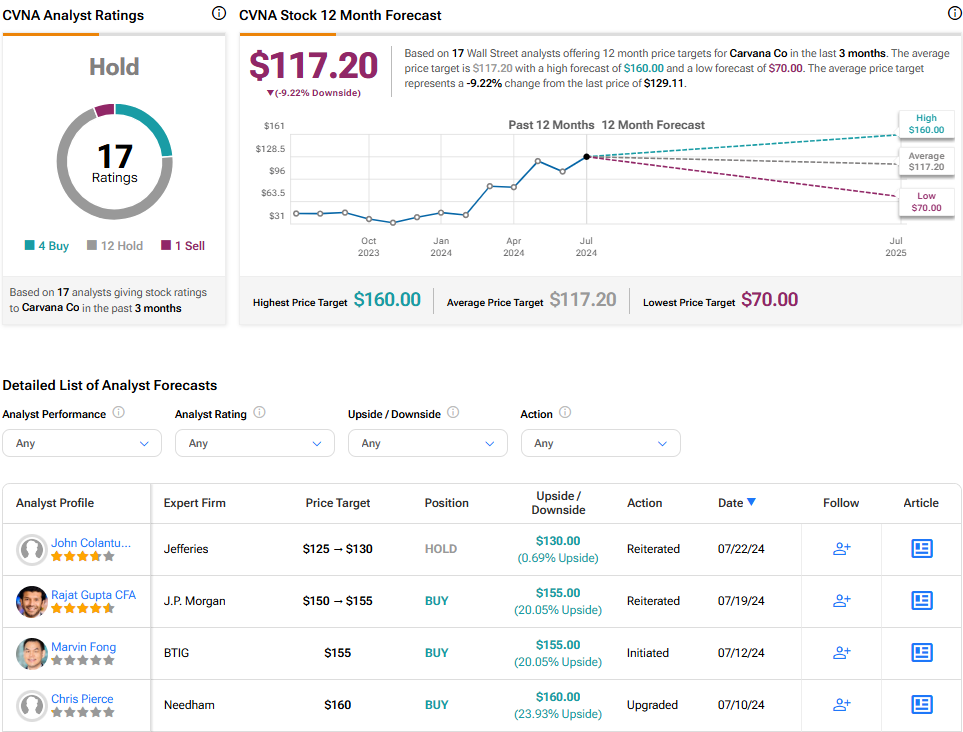

What Is the Target Price for CVNA Stock?

Out of the 17 analysts tracking Carvana, four have Buy ratings, 12 have Hold ratings, and one recommends a Sell, indicating a Hold consensus rating. The average CVNA stock price target is $117.20, indicating downside potential of 9.2% from current levels.

The Takeaway

Carvana is a company navigating an uncertain and volatile macro environment. While it is improving its profit margins and shoring up its balance sheet, it remains a high-risk investment, especially if the economy enters a recession. Alternatively, it is part of an expanding addressable market, allowing it to keep growing at a reasonable pace in the upcoming decade.