Bitcoin’s retreat has left a visible scar on Strategy’s (MSTR) share price. The token has dropped about 30% to roughly $85,000 since early October, a decline driven by a more hawkish-than-expected Federal Reserve and a broader shift toward risk-off positioning across markets. The downturn has triggered forced unwinds in leveraged positions and in holders of Bitcoin ETFs, intensifying the selloff. For a company that has rebranded itself as a “crypto treasury,” this kind of move hits like a freight train.

Claim 30% Off TipRanks

- Unlock hedge fund-level data and powerful investing tools for smarter, sharper decisions

- Discover top-performing stock ideas and upgrade to a portfolio of market leaders with Smart Investor Picks

Strategy’s common stock has fallen more than 50% to around $177, a steep drop from the $543 level it reached a year ago. The equity now trades close to net asset value rather than the hefty premium it once enjoyed. Its $8 billion pile of convertible bonds has also felt the pressure, particularly a $3 billion issue that now yields almost 8% and can be put back to the company in 2028.

Strategy Preferreds Offer Double-Digit Income

Behind the wreckage in the common sits a different set of securities that are suddenly drawing attention. Strategy has issued about $8 billion of preferred stock across five deals this year. The four U.S. issues trade on Nasdaq (NDAQ) under the tickers Stretch (STRC), Stride (STRD), Strife (STRF) and Strike (STRK). These preferreds are perpetual and sit above the common in the capital stack, delivering fixed dividends that have long appealed to income investors.

The recent selloff has pushed yields into eye-popping territory. Strategy’s preferreds now offer between 10% and 15%, some of the richest payouts in a roughly $300 billion preferred market where big bank issues from the likes of JPMorgan (JPM) and Bank of America (BAC) yield around 6%. Capital Group holds more than $1 billion of these preferreds, and Bill Miller’s income fund owns STRD, which currently yields close to 15%. “Saylor has figured out a way to create debt and preferred structures that appeal to different investors’ risk/reward tolerances,” Miller said.

Saylor Points to Bitcoin War Chest as Backstop

Credit agencies are far less enthusiastic. S&P Global (SPGI) Ratings assigns Strategy a low-junk B minus rating and warns about its “narrow business focus, high Bitcoin concentration, and low U.S. dollar liquidity.” The company must cover roughly $700 million a year in preferred dividends while its software business barely breaks even and Bitcoin generates no cash yield.

Management argues the balance sheet has more than enough firepower. Strategy controls about $55 billion of Bitcoin, roughly 3% of the circulating supply. CEO Phong Le reminded investors on the third-quarter call that “We could sell high-basis Bitcoin to cover our dividend needs on our preferred stock.” In a post last week, the company said that “at current Bitcoin levels, we have 71 years of dividend coverage assuming the price stays flat.” Insiders, including Le, have been buying several of the preferred issues alongside outside institutions.

Investors Weigh Tail Risk Against Coverage Math

The real nightmare scenario is a deep and lasting collapse in Bitcoin that erodes the cushion behind both debt and preferreds. Bears such as Peter Schiff argue that the whole model “relied on income-oriented funds buying ‘high-yield’ preferred shares” and that the promised yields “will never actually be paid.” If that were true and funds began dumping their holdings, Strategy could lose access to one of its key funding tools.

Supporters counter that the company has powerful incentives to keep preferred dividends flowing, even if that means parting with some Bitcoin. Because the payouts are treated as a return of capital rather than ordinary income, investors also get tax deferral until they sell the securities, which sweetens the proposition. For those comfortable riding Bitcoin’s roller coaster, the common stock still looks like a gamble. The preferreds, however, offer a high-yield way to bet that Michael Saylor and his “crypto treasury” can keep the lights on through the next cycle.

Is Strategy a Good Stock to Buy?

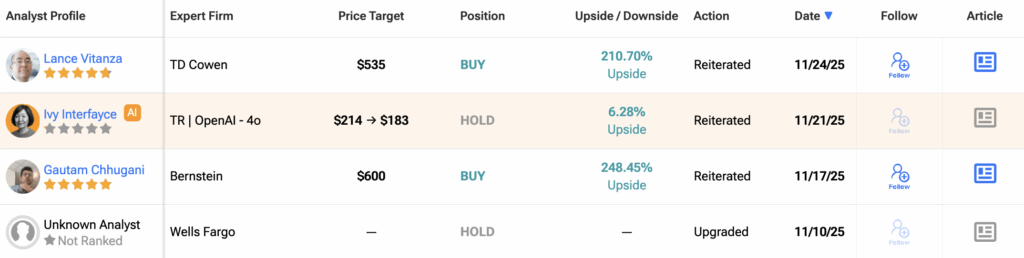

Turning to TipRanks, analyst data shows Wall Street remains firmly optimistic about Strategy despite the stock’s slide and the volatility in Bitcoin. In total, 14 analysts have weighed in over the past three months, and the consensus rating sits at Strong Buy. Out of these calls, 12 analysts call the stock a Buy, two say a Hold, and none recommend a Sell.

The average 12-month MSTR price target comes in at $524.08, which implies roughly 204% upside from the recent close.