Palantir (PLTR) has been one of the market’s hottest stocks, surging over 151% year-to-date and reaching a new 52-week high. The stock has plenty going for it, but should investors chase the stock here or wait for a better entry point? I’m negative on shares of Palantir at this point in time, based on its astronomical valuation, which leaves little room for error, recent insider selling, its unfavorable analyst outlook, and its unfavorable rating from TipRanks’ proprietary Smart Score system.

Claim 30% Off TipRanks

New trading tool for NVDA bears

Concerns Over PLTR’s Nosebleed Valuation

While the AI powerhouse is profitable, it trades at an unsustainable valuation relative to its earnings. Palantir currently trades at an incredible price-to-earnings ratio of 116.6x based on consensus 2024 earnings estimates, making it over four times more expensive than the broader market, as the S&P 500 (SPX) trades at 24.4 times earnings.

It’s hard to understate just how steep this valuation is—Nvidia (NVDA), which I own and is often criticized as a prime example of overvalued stocks riding the AI hype, appears relatively cheap next to Palantir. Nvidia trades at a much more modest 46.8 times its January 2025 earnings estimates. You can cut Palantir’s multiple in half and it would still be more expensive than Nvidia.

Even when looking forward to next year, Palantir’s shares appear to be priced for perfection, trading at 96.1 times forward earnings estimates. Though Palantir is a strong company with an exciting future, such a nosebleed valuation offers investors little margin for error. Stocks with these high multiples can quickly decline if growth slows, earnings disappoint, or if the enthusiasm surrounding AI diminishes.

Palantir Seems Ahead of its Skis

Of course, there’s more to investing than simply looking at price-to-earnings multiples. So let’s give Palantir another chance by examining other metrics, such as the PEG ratio (price/earnings to growth ratio). This valuation metric often favors growth stocks like Palantir because it factors in earnings growth.

The PEG ratio is a stock’s price-to-earnings ratio divided by its earnings growth rate. The lower the PEG ratio, the more attractive a stock looks based on this metric. Investors who use this metric typically view a PEG ratio of under 1.0x to be attractive. So how does Palantir look based on this metric? Unfortunately, with a PEG ratio of over 10, Palantir still looks to be ahead of its skis.

Next, let’s take a look at Palantir on a price-to-sales basis, a metric sometimes favored by growth investors that is often used when evaluating early-stage tech and software stocks. It’s hard to make the case that Palantir is a buy using this metric, with a steep price-to-sales ratio of 38.9. Many shrewd software investors believe that paying more than 15 times sales for a business is an overpay, and Palantir clocks in at more than double that number. Even fellow software powerhouses like ServiceNow (NOW) trades at a far cheaper price-to-sales multiple of 17.4 times sales.

What Are Insiders Doing?

Meanwhile, key Palantir insiders are selling shares in droves.

Co-founder and Chairman Peter Thiel recently sold nearly $600 million worth of shares at the end of September (at an average share price of $36.90), and another batch worth $457 million on October 1 (at an average share price of $36.85) cashing in on over $1 billion worth of shares. Also, co-founder and CEO Alex Karp sold nine million shares on September 17th for an average price of $36.18 (worth over $325 million), which is well below the stock’s current levels.

Insiders can sell shares for various reasons, and Thiel and Karp are entitled to realize some profits from their involvement in the company’s success. However, their significant selling suggests that even they acknowledge it might be time to cash in on some gains.

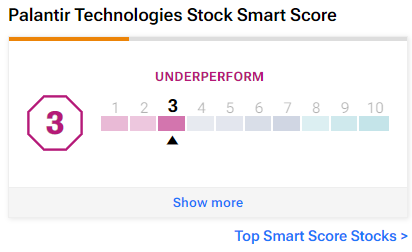

Underwhelming Smart Score

Sell-side analysts are cautious about Palantir, and Smart Score is also skeptical. The Smart Score is a quantitative stock scoring system created by TipRanks. It gives stocks a score from one to 10, based on eight key market factors. Scores of eight, nine, or 10 are considered equivalent to an Outperform rating. Meanwhile, scores of four, five, six, or seven are considered Neutral, and scores of three and below are considered Underperform-equivalent.

A Smart Score of three places Palantir squarely in the Underperform-equivalent category, adding to the reasons that investors should wait for a better entry point into the stock.

Is PLTR Stock a Buy?

Turning to Wall Street, PLTR earns a Hold consensus rating based on two Buys, five Holds, and four Sell ratings assigned in the past three months. The average PLTR stock price target of $27.78 implies 35.59% downside potential from current levels.

While analysts certainly aren’t right all the time, there is power in the wisdom of the crowd. The fact that Palantir has managed to run so far beyond the average price target of 11 analysts gives credence to the idea that the stock has become overheated.

No Need to Chase PLTR Stock

Palantir is a cutting-edge company and an exciting stock that has become a favorite of retail investors eager to invest in the future of AI-powered solutions. While I understand the enthusiasm (and have owned the stock in the past), it’s difficult to justify buying the stock today at these levels.

Palantir could indeed be a strong long-term investment, but I’m bearish on Palantir for the immediate future based on the spate of insider selling, its Underperform-equivalent Smart Score, unfavorable analysts’ estimates, and ultimately, its unsustainable valuation, which gives investors little room for error and no real margin of safety.

I believe that interested investors will likely have multiple opportunities to purchase the stock at more attractive entry points than its current trading price.