Spirit Airlines (NYSE:SAVE) shares are under pressure in the premarket session today after the air carrier’s first-quarter revenue declined by 6.2% year-over-year to $1.27 billion. Additionally, its net loss per share of $1.46 lagged expectations by $0.01. In comparison, Spirit had incurred a net loss per share of $0.82 in the year-ago period.

Meet Samuel – Your Personal Investing Prophet

- Start a conversation with TipRanks’ trusted, data-backed investment intelligence

- Ask Samuel about stocks, your portfolio, or the market and get instant, personalized insights in seconds

Spirit’s Weak Q1

Spirit’s first-quarter performance was impacted by adverse weather, air traffic-associated delays, and operational challenges in Haiti. Moreover, the company’s aircraft utilization during the quarter shrank by 7.1% to 10.4 hours due to aircraft availability bottlenecks.

Furthermore, while Spirit’s capacity increased by 2.1%, its load factor contracted marginally by 10 basis points to 80.7%. Its total revenue per passenger declined by 8.1% to $117.03. Importantly, its fare revenue per segment shrank by 16.3% to $48.08.

Spirit’s Rebound Efforts, Post-Deal Fallout

This weak performance follows the termination of Spirit’s merger deal with JetBlue (NASDAQ:JBLU). In Q1, Spirit received a payment of $69 million from JetBlue associated with the scrapped deal. Now, it is banking on streamlining resources, improving working capital, and boosting liquidity to drive performance. Importantly, Spirit expects these efforts to lead to an improvement of $450 million to $550 million in its cash levels this year. The company had a total available liquidity of $1.2 billion at the end of Q1.

Last month, Spirit deferred all aircraft deliveries from Airbus (OTC:EADSY) that were scheduled to be delivered in Q2 2025 through the end of 2026 to 2030-2031. The company expects this move to improve its liquidity by nearly $230 million.

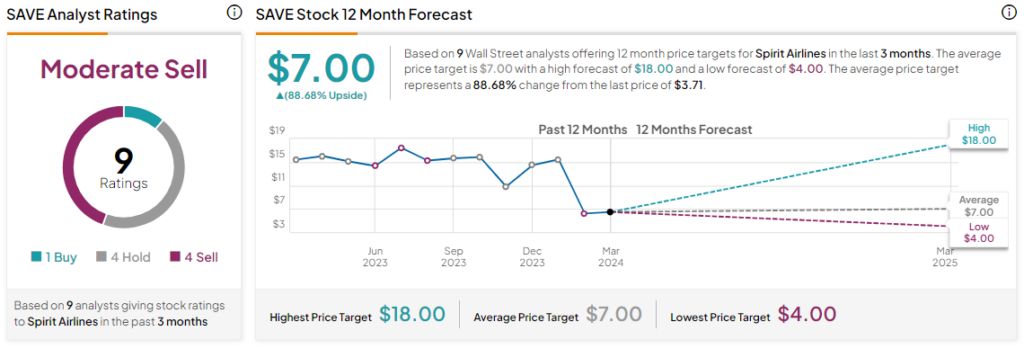

What Is the SAVE Stock Price Forecast?

Spirit’s share price has tanked by nearly 75% over the past year. Overall, the Street has a Moderate Sell consensus rating on Spirit, alongside an average SAVE price target of $7. However, analysts’ views on the company could see changes following today’s earnings report.

Read full Disclosure