Realty Income Corp. (O) has faced challenges in recent years, with elevated interest rates weighing on shares (see chart below) of the real estate investment trust (REIT). Despite this, the company’s operational performance has remained strong , with its adjusted funds from operations per share reaching new heights. At the same time, the REIT’s legendary dividend, a favorite among income-oriented investors, continues to offer growth potential, making Realty Income Corp. a compelling pick for those seeking rising, dependable income. The stock’s valuation appears compelling, too. For these reasons, I am bullish on O stock.

Claim 55% Off TipRanks

- Unlock hedge fund-level data and powerful investing tools for smarter, sharper decisions

- Discover top-performing stock ideas and upgrade to a portfolio of market leaders with Smart Investor Picks

Why Realty Income Has Underperformed

If you’ve been following Realty Income for some time, you may agree that its extended underperformance is unusual, especially given its long-standing reputation as a Wall Street darling celebrated for its remarkable track record of dividend growth. As a reminder, the REIT has increased its dividend for 27 consecutive years. This feat has earned it the status of a “Dividend Aristocrat.”

However, elevated interest rates have created a challenging environment, affecting Realty Income and other REITs. Investors have gravitated toward lower-risk fixed-income investments, which offer quite high yields without the volatility of equity markets. Moreover, higher rates have curbed Realty Income’s growth prospects, as REITs heavily rely on external financing to expand their property portfolios.

This situation has placed significant pressure on Realty Income’s share price. While its portfolio remains robust and continues to produce excellent results, the broader market sentiment around REITs has been less favorable, with the rising cost of capital and slowing of deal activity acting as a headwind.

Share Growth Despite Sector Weakness

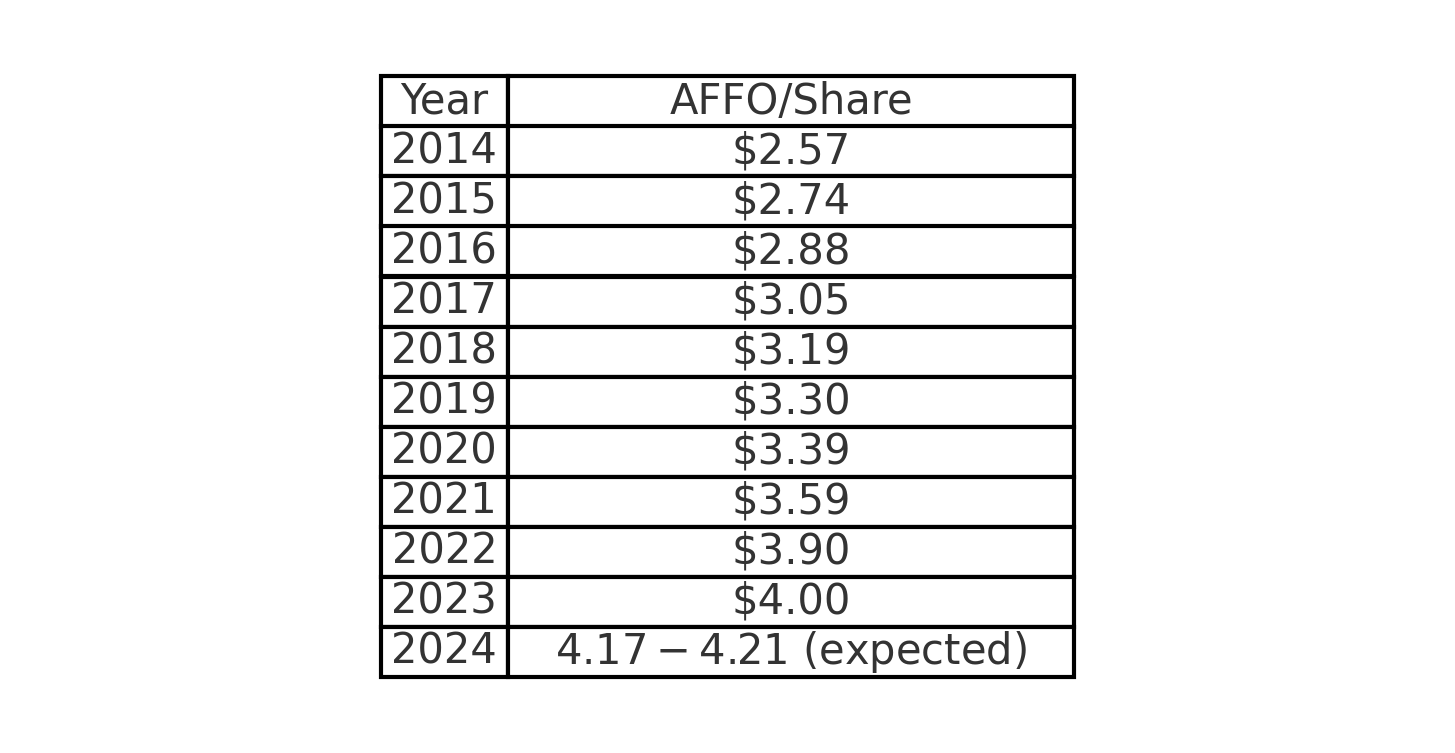

Despite the lackluster sentiment, Realty Income Corp. has delivered remarkable AFFO/share growth, which is why I remain bullish outlook on its investment case. This is true even as its interest expenses have risen. To illustrate how terrific the performance has been, and continues to be, here’s Realty Income’s AFFO/share over the past decade:

Even with interest rates peaking above 5% last year, Realty Income Corp. has continued to grow its AFFO/share, flexing its operational strength. The third quarter of 2024 further highlighted this resilience, with Realty Income’s revenues rising 26% to $1.33 billion and AFFO/share growing 3% to $1.05. Of course, the topline growth stems largely from last year’s Spirit Realty Capital acquisition and several property purchases, including 82 acquisitions in Q3 alone.

However, what’s important is that these investments have proven accretive to per-share AFFO, the key metric for REIT investors. Therefore, you can see why management felt confident enough to once again raise its full-year guidance to $4.17-$4.21. This implies another record despite the continuously tough macro-environment affecting the real estate sector.

The Dividend Growth Case

Another reason I’m bullish on O stock is its dividend. Given Realty Income’s stellar performance, the REIT should have no trouble growing its dividend, which is why I see the stock’s investment case as remaining strong. The midpoint of management’s AFFO/share guidance implies a healthy payout ratio of 76%, providing ample room for further dividend increases. Recently, Realty Income raised its monthly dividend once again, reminding us of its dedication to rewarding shareholders.

Another appealing factor for income investors is Realty Income’s valuation. With the stock trading at about 13 times this year’s expected AFFO/share, today’s multiple is at the low end of the past decade’s range. I believe this compression in valuation offers a decent margin of safety for new investors, while the 5.7% dividend yield seems substantial, especially considering the frequent dividend hikes. For context, Realty Income is the highest-yielding large-cap retail REIT.

Is O Stock a Buy?

Wall Street analysts appear generally positive towards Realty Income’s stock, which currently has a Moderate Buy rating comprised of three Buys and seven Hold ratings assigned over the last three months. At $63.78, the average Realty Income stock forecast implies 15.29% upside potential from current levels.

For the best guidance on buying and selling Realty Income stock, look to Simon Yarmak. He is the most accurate and profitable analyst covering the stock (on a one-year timeframe), boasting an average return of 2.62% per rating and a success rate score of 56%.

Conclusion

It’s evident that Realty Income’s recent underperformance can be attributed to external factors such as elevated interest rates rather than any fundamental weakness in its business. As its results indicate, the company has shown remarkable resilience, achieving consistent AFFO/share growth and maintaining its reputation as a Dividend Aristocrat despite a challenging environment. Given these factors, along with the appeal of its dividend, substantial yield, and relatively cheap valuation, I view Realty Income Corp. as an attractive choice for income-focused investors.