Peloton Interactive (PTON) rallied in pre-market trading after reporting better-than-expected revenues and its losses narrowed in the Fiscal fourth quarter. The exercise equipment company’s losses narrowed in the fourth quarter to $0.08 per share, compared to a loss of $0.68 per share in the same period last year. This was better than analysts’ estimates of a loss of $0.17 per share.

Claim 55% Off TipRanks

- Unlock hedge fund-level data and powerful investing tools for smarter, sharper decisions

- Discover top-performing stock ideas and upgrade to a portfolio of market leaders with Smart Investor Picks

PTON’s Q4 Revenue Shows Modest Growth

In terms of revenue performance, the company generated $644 million in the fourth quarter, up by 0.2% year-over-year, exceeding analysts’ expectations of $628.5 million. This marked the first instance of modest revenue growth since the second quarter of FY22.

Moreover, Peloton’s subscription revenue increased by 2.3% year-over-year to $431 million. This segment, where users pay a one-time delivery fee in addition to a monthly fee to rent stationary bikes, saw growth driven largely by the secondary market. Notably, used bikes in this market experienced a 16% year-over-year growth. Additionally, PTON highlighted that subscribers from the secondary market exhibit lower churn rates compared to rental customers.

Peloton’s Turnaround Plan Begins to Show Results

Turning to the broader company strategy, Peloton, which faced challenges following the resignation of its CEO Barry McCarthy, is now led by two of its Board members while it continues its search for a new CEO. In response to its struggles, the company undertook a significant restructuring plan, which included a 15% reduction in workforce and a major debt refinancing effort.

The results of this restructuring are evident. Peloton reported $70 million in adjusted Earnings Before Interest, Taxes, Depreciation, and Amortization (EBITDA), exceeding analyst expectations of $53 million. Furthermore, the company generated $26 million in free cash flows, a significant improvement from the negative $74 million reported in the same period a year prior. This achievement marks the second consecutive quarter of delivering adjusted EBITDA and positive free cash flows, a feat it had not accomplished since the COVID-19 pandemic.

PTON’s Q1 and FY25 Outlook Projected to Decline

Looking ahead, Peloton anticipates first-quarter sales to range between $560 million and $580 million, reflecting a 4% year-over-year decline. The company also projects adjusted EBITDA to be between $50 million and $60 million.

In addition, Peloton forecasts connected fitness subscribers to be between 2.88 million and 2.89 million, representing a 3% year-over-year drop. This decrease is attributed to a “seasonally low quarter for hardware sales” and a challenging macroeconomic environment.

For FY25, Peloton expects sales to be between $2.4 billion and $2.5 billion, with adjusted EBITDA projected to range from $200 million to $250 million.

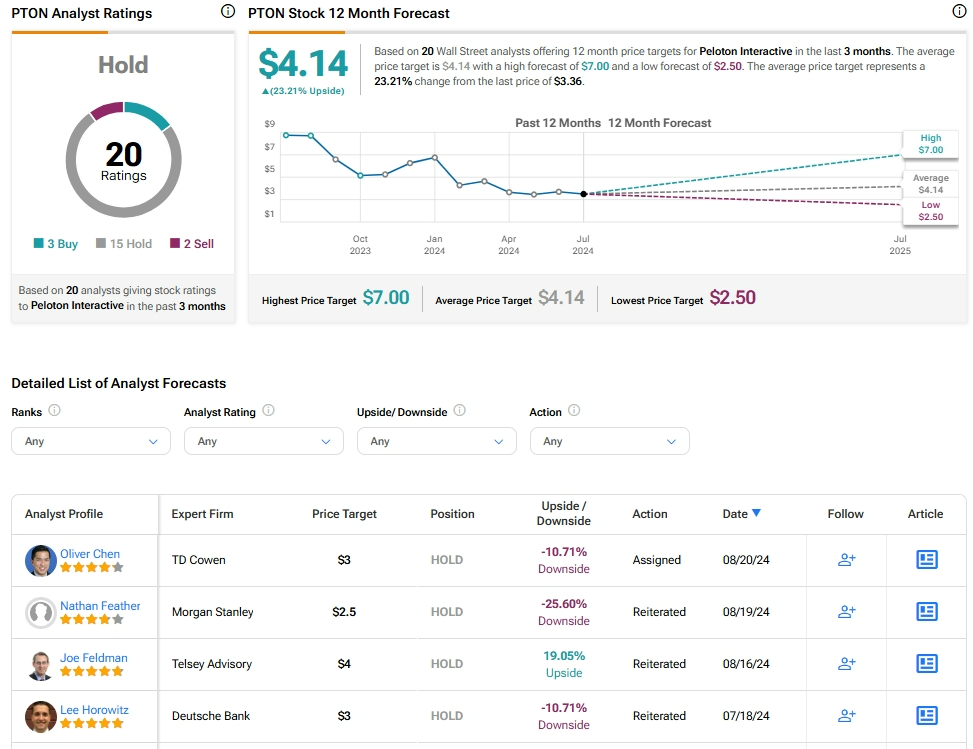

Is Peloton a Buy, Sell, or Hold?

Analysts remain sidelined about PTON stock, with a Hold consensus rating based on three Buys, 15 Holds, and two Sells. Over the past year, PTON has declined by more than 50%, and the average PTON price target of $4.14 implies an upside potential of 23.2% from current levels. These analyst ratings are likely to change following PTON’s results today.