The dramatic market selloff during the first quarter of 2025 has created the opportunity for investors to buy some promising tech stocks at surprisingly cheap valuations, and social media platform Pinterest (PINS) is a strong example. I’m bullish on Pinterest based on its incredibly cheap valuation, massive share repurchase program, revenue growth, and user growth. Furthermore, the stock receives an Outperform-equivalent TipRanks Smart Score, while Wall Street analysts rate it a Strong Buy with a potential upside of approximately 70% over the next 12 months.

Claim 55% Off TipRanks

- Unlock hedge fund-level data and powerful investing tools for smarter, sharper decisions

- Discover top-performing stock ideas and upgrade to a portfolio of market leaders with Smart Investor Picks

What is Pinterest?

If you’re not already familiar with Pinterest, it’s a platform with 553 million monthly active users that describes itself as “a visual search and discovery platform where people find inspiration, curate ideas, and shop products—all in a positive place online.”

I believe this emphasis on being a positive place online is more than just fluff and could be a real differentiator for the company going forward. In a very polarized climate in the U.S., where political discourse is prevalent on social media platforms like X and Facebook, there is little in the way of divisiveness on Pinterest.

Users are more likely to post curated collections of the aesthetics they like for their dream kitchen remodel or spring wardrobe than they are to argue about the political controversies of the day, which I believe can be a real differentiator for Pinterest, making it relevant and giving it a unique selling point in a crowded social media landscape.

Pinterest is Surprisingly Cheap

Pinterest is down nearly 30% from its 52-week high, and shares are now surprisingly cheap. The stock now trades at under 17x consensus 2025 earnings estimates, meaning it is significantly more affordable than the broader market — the S&P 500 (SPX) currently trades for 20.5x 2025 earnings.

Not only is Pinterest cheaper than the broad market index, but it’s also cheaper than its major social media and internet peers. For example, the much larger Meta Platforms (META) trades for roughly 23x 2025 earnings estimates, Snapchat (SNAP) trades for about 25x, Spotify trades for 50x, and Reddit (RDDT)’s valuation is more than 95x. Pinterest looks even cheaper when looking ahead to 2026, as shares trade for a dirt cheap valuation of under 14x 2026 earnings estimates. On a price-to-sales basis, shares of Pinterest are also quite palatable, trading at just under 5x.

No matter how you slice it, Pinterest stock is cheap, making it a far more affordable entry into social media exposure for investors. Meanwhile, RDDT stock is the standout outperformer.

Pinterest is Humming Along

Shares may be priced like this is a declining company, but Pinterest is performing quite well as a business. Last quarter, Pinterest recorded its first-ever billion-dollar quarter of revenue when it grew revenue 18% year-over-year to $1.15 billion. For the full-year, Pinterest’s revenue grew by an impressive 19% to $3.64 billion in 2024.

Zooming further out, Pinterest’s long-term revenue trajectory has been strong. Its 2024 revenue of $3.64 billion is more than double the $1.69 billion the company brought in just four years ago in 2020 and more than triple the $1.14 billion it brought in 2019. Pinterest’s user base is also growing, as its global active monthly users totaled 553 million, which is an 11% year-over-year increase.

Returns to Shareholders

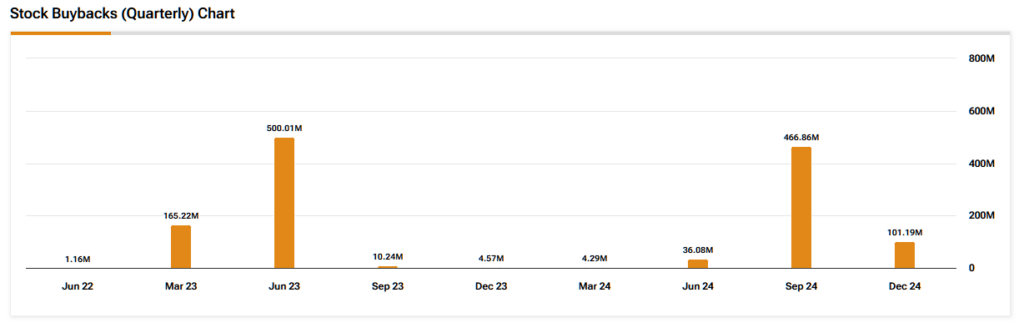

Pinterest is not a dividend stock. But it has some significant returns to shareholders in store for its investors. Last November, the San Francisco-based company announced a new $2 billion stock buyback program. Pinterest’s market capitalization is just $21.7 billion, so this is a relatively large program enabling Pinterest to repurchase nearly 10% of its market cap.

Share buybacks can be accretive to shareholders as they reduce a company’s shares outstanding and increase earnings per share. Plus, most importantly, shares are cheap right now, making this buyback program even more attractive.

Is PINS Stock a Good Buy?

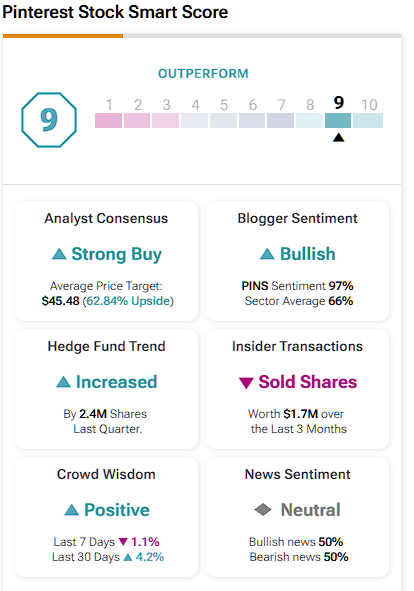

Turning to Wall Street, PINS earns a Strong Buy consensus rating based on 26 Buys, six Holds, and zero Sell ratings assigned in the past three months. The average analyst PINS stock price target of $45.48 per share implies almost 70% upside potential from current levels.

PINS’ Strong Smart Score

In addition to this favorable rating from analysts, Pinterest receives an attractive Outperform-equivalent Smart Score of 9 from TipRanks’ Smart Score system. The Smart Score is a proprietary quantitative stock scoring system created by TipRanks. It gives stocks a score from one to ten based on eight market key factors. The lowest score is 1, and the highest is 10. A Smart Score of 8 or above is equivalent to an Outperform rating.

Bright Future Ahead for PINS Stock

I’m bullish on Pinterest and believe it represents an attractive buying opportunity for investors amid the current market downturn, which has seen tech stocks sell off dramatically. Pinterest is growing users and revenues while trading at a relatively cheap valuation. Also, it plans to return significant capital to shareholders via its $2 billion share buyback program going forward. With all that in mind, I’m stoutly bullish on this visual social media specialist.