Eyewear retailer Warby Parker (WRBY) delivered solid sales results in Q2, exceeding market expectations. The market has received this as a positive inflection point in gross margins and free cash flow, and the share price has climbed over 10% since. The company’s improved operational efficiencies, robust sales in single-vision glasses, and expansion into insurance partnerships present further upside growth potential. Warby’s unique market position and steady revenue growth separate it from industry peers, making it a solid option for investors, even if they don’t need glasses themselves.

Claim 30% Off TipRanks

- Unlock hedge fund-level data and powerful investing tools for smarter, sharper decisions

- Discover top-performing stock ideas and upgrade to a portfolio of market leaders with Smart Investor Picks

Warby Parker’s Strategic Growth Initiatives Bearing Fruit

Warby Parker manufactures and retails prescription glasses, contact lenses, and sunglasses. Initially an online-only retailer, the company has expanded sales to more than 200 retail locations across the U.S. and Canada.

The company has seen active customer growth for four consecutive quarters, ending Q2 with 2.4 million active customers – a 4.5% increase on a trailing 12-month basis. Average revenue per customer also saw an 8.8% growth. Management has identified three key strategies to drive this growth: ramping up marketing efforts to accelerate customer growth, turning its e-commerce channel back to positive growth, and significantly expanding its insurance offering.

Warby has recently seen an acceleration in its glasses business growth compared to the previous year, largely due to strategic investments in marketing, store expansion, and product innovation. It sees its glasses, particularly single-vision glasses, as a major revenue driver and is investing heavily in its marketing channels to attract more customers in this segment.

Further complementing its growth strategy, the company has announced an expanded in-network relationship with Versant Health, a subsidiary of MetLife (MET), which will bring millions of additional potential customers into Warby Parker’s network. This initiative, expected to be finalized before the end of the year, is projected to be a long-term tailwind over the next several years.

Warby Parker’s Recent Financial Results & Outlook

Warby Parker’s Q2 2024 earnings report was a mixed bag. Revenue of $188.2 million marked a 13.3% increase from last year while beating analysts’ expectations by $1.16 million. Additionally, the gross margin improved by 1.4 points to 56.0%. However, the company reported a GAAP net loss of $6.8M, an improvement of $9.2M compared to the previous period, primarily driven by the increase in revenue. Finally, the company missed consensus EPS projections of $0.05, landing at -$0.06.

The company ended the quarter with a cash and cash equivalents of $238.0M.

For the full year of 2024, management projects revenue between $757 million and $762 million and an adjusted EBITDA of $72.5 million (the midpoint of the range), which equates to a Margin of 9.5%. The company plans to open 40 new stores.

What Is the Price Target for WRBY Stock?

The stock is a bit volatile, with a beta of 1.95, though overall, it has been on an upward trend, climbing 34% in the past year. It trades at the higher end of its 52-week price range of $9.83 – $17.95 and demonstrates positive price momentum, trading above its 20-day (15.91) and 50-day (15.55) moving averages. With a P/S ratio of 2.6x, it trades in line with the Healthcare sector, though it appears relatively undervalued to the Medical Instruments & Supplies industry average of 4.8x.

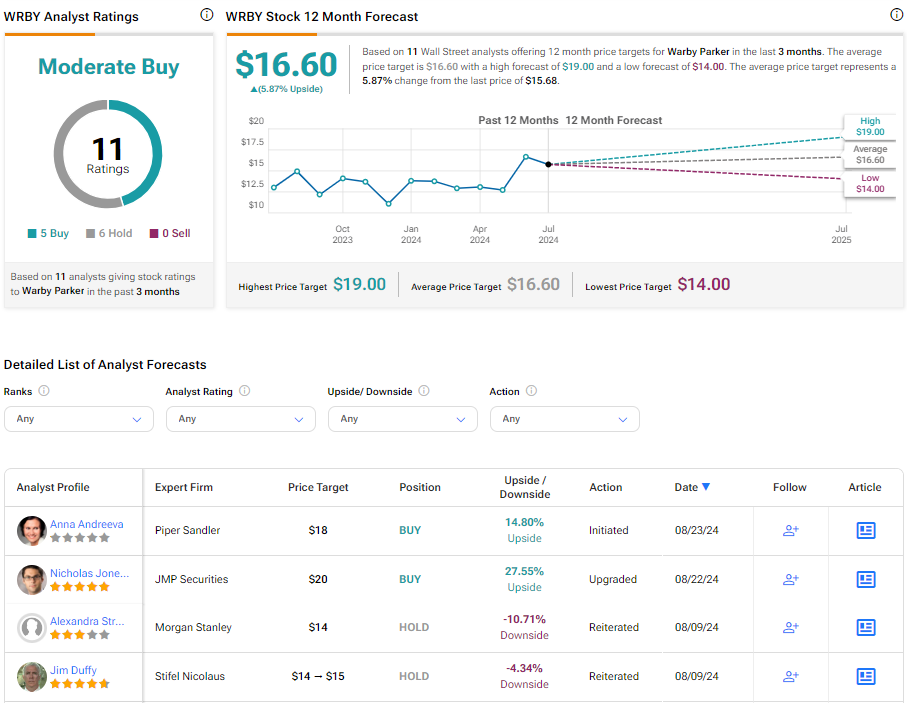

Analysts following the company have been cautiously optimistic about WRBY stock. For instance, JMP Securities analyst Nicholas Jones, a five-star analyst according to Tipranks’ ratings, recently upgraded the shares to Outperform with a $20 price target, noting consensus estimates for the company are too low. However, he warns that the path forward will likely remain volatile and non-linear.

Based on the recommendations and price targets assigned by 11 analysts, Warby Parker is rated a moderate buy. The average price target for WRBY stock is $16.60, representing a potential 5.87% upside from current levels.

Bottom Line on WRBY

Warby Parker is proving to be a formidable player in the eyewear industry. Despite missing earnings projections, recent financials show a spike in active customer growth and revenue, with promising signs that the trend will continue, given the company’s strategic marketing efforts, expansion of its e-commerce channel, and partnership with Versant Health. Warby’s market performance remains robust, making it a compelling investment option amidst a highly competitive market.