Athletic footwear and apparel giant Nike (NYSE:NKE) generated better-than-anticipated revenue for the fourth quarter of Fiscal 2023. However, the company’s earnings and outlook failed to impress investors, with NKE shares down about 3% in Friday’s pre-market trading. Higher costs and markdowns to clear inventory in a challenging macro backdrop impacted the company’s profitability.

Meet Samuel – Your Personal Investing Prophet

- Start a conversation with TipRanks’ trusted, data-backed investment intelligence

- Ask Samuel about stocks, your portfolio, or the market and get instant, personalized insights in seconds

Nike’s Q4 Earnings Hit by Markdowns

Nike’s Q4 FY23 EPS declined 27% year-over-year to $0.66, as the 5% rise in revenue was more than offset by lower margins. The company’s gross margin contracted 140 basis points to 43.6%. Higher markdowns, increased input costs amid an inflationary backdrop, a rise in freight and logistics costs, and currency headwinds weighed on the company’s gross margin.

Macro pressures continue to impact consumer spending. Amid high inflation, consumers are spending on essentials while moderating their discretionary expenditure. Like several other retailers, Nike also struggled with elevated inventory levels in recent quarters. At the end of Q4 FY23, Nike’s inventory stood at $8.5 billion, flat year-over-year but down when compared to $8.9 billion in the previous quarter.

Margin Outlook

While Nike expects its Q1 FY24 gross margin to decline 50 to 75 basis points, the company projects its full-year gross margin to improve. The company expects FY24 gross margin to expand by 140 to 160 basis points, driven by recovery from “transitory headwinds,” including more favorable ocean freight rates starting in the fiscal second quarter and a modest improvement in markdowns.

Management cautioned that it continues to operate in a promotional environment and will continue to “read and react.” Increased labor and fulfillment expenses are expected to keep product costs higher in FY24. To offset cost pressures, the company intends to increase its prices in FY24 by low single digits.

The company also expects its margins to benefit from the continued shift to a more direct business. Nike has been reducing its exposure to wholesale channels and focusing on its direct-to-consumer (DTC) channel. In Q4 FY23, Nike Direct revenue increased 15% while Wholesale revenue declined 2%.

While the company continues to believe in its direct-to-consumer strategy, it is selectively re-establishing some wholesale relationships. This month, Macy’s (NYSE:M) and Designer Brands (NYSE:DBI)-owned DSW announced that they would restart selling a range of Nike merchandise in October. During the Q4 earnings call, CEO John Donahoe said that the company is “selectively opening new doors.” He acknowledged that multi-brand wholesale partners play a very important role in reaching customers.

Is Nike a Sell or Buy?

Following the Q4 print in Thursday’s after-hours, Goldman Sachs analyst Kate McShane reiterated a Buy rating on the stock with a price target of $145. The analyst said that his constructive view on NKE remains intact following the results.

The analyst noted that Nike’s near-term growth and margins seem more challenged than his expectations due to wholesale shipment timing, liquidation sales, temporary cost pressures, and selling, general and administrative investments. That said, McShane believes that Q4 FY23 performance reinforced the several “key proofpoints” of his bullish thesis, including robust DTC momentum, and sequential improvement in inventory.

The analyst thinks that Nike’s ongoing sales momentum and innovation-driven market share gains are key indicators of the company’s ability to navigate challenging macro backdrops.

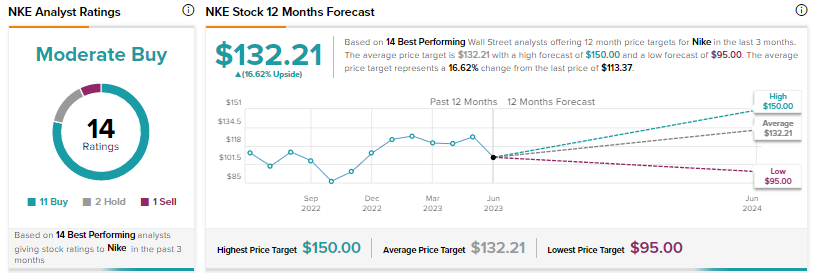

Wall Street is cautiously optimistic on Nike, with a Moderate Buy consensus rating based on 11 Buys, two Holds, and one Sell. The average price target of $132.21 implies nearly 17% upside.