Last week’s focus was on rates, labor, and shipping. This week, the ground shifted under a few different feet. Shopify (SHOP) made headlines with a fresh distribution angle, Washington’s shutdown created a data fog that marketers hate, and the holiday machine just kicked into gear with October mega-promotions.

Claim 30% Off TipRanks

- Unlock hedge fund-level data and powerful investing tools for smarter, sharper decisions

- Discover top-performing stock ideas and upgrade to a portfolio of market leaders with Smart Investor Picks

In the meantime, oil and the dollar moved in ways that actually matter for merchant margins and cross-border conversion. Let’s stitch those threads together and see what they mean for SHOP, on which I am still Bullish.

ChatGPT Checkout: A New Top-of-Funnel for Merchants

This week, OpenAI introduced “Instant Checkout” within ChatGPT, partnering with Shopify at launch and using Stripe to handle payments. The feature debuts with single-item purchases, available now for U.S. Etsy (ETSY) sellers, with Shopify merchants to be added soon.

Multi-item carts are also on the roadmap. Users pay no fees, with costs borne by merchants. While SHOP stock rallied on the announcement, the bigger story is this: ChatGPT now offers a native shopping surface at the very point of discovery—creating incremental demand without redirecting users elsewhere.

Shutdown Fog and a Softer ADP Print

The U.S. government shut down on Oct. 1, potentially delaying the BLS jobs report and other key federal releases. Markets dislike uncertainty—especially with the Fed insisting policy remains “data dependent.” In the absence of official numbers, investors turned to private indicators: ADP reported a 32,000 drop in September private payrolls alongside softer wage growth. With this month’s labor report postponed as a result of the U.S. government shutdown, all eyes are, of course, on the U.S. non-farm payrolls figure in November.

With reliable data scarce and hiring momentum weakening, discount-rate pressure eases, but volatility picks up in long-duration names like SHOP. Worth keeping on the radar.

October Promo Wave: Demand Gets Pulled Forward

The holiday shopping season effectively kicks off next week. Amazon’s (AMZN) Prime Big Deal Days run Oct. 7–8, Target’s (TGT) Circle Week spans Oct. 5–11, and Walmart’s (WMT) Deals stretch from Oct. 7–12. These events typically front-load traffic, reset reference prices, and condition consumers to expect promotions earlier in the season.

For Shopify merchants, that means shifting ad spend into October, managing inventory more tightly, and testing free-shipping thresholds now—rather than waiting until Black Friday week. Strong early sell-through would provide a clean GMV read-through for SHOP heading into Q4.

Costs and Currency: Small Tailwinds Worth Circling

Two recent cost trends are moving in favor of merchants. First, oil has eased into the mid-$60s, bringing the U.S. average for regular gasoline down to about $3.16 per gallon. That can reduce parcel fuel surcharges and give consumers a bit more discretionary spending power.

Second, the dollar has weakened in recent sessions, supporting U.S. cross-border conversion and easing FX drag on reported results. Small shifts like these can have a meaningful impact across millions of carts and thousands of settlement lines.

Freight Cheaper, Last-Mile Pricier

On the shipping front, Drewry’s World Container Index fell another 8% w/w to $1,761/FEU as of Sept. 25—its 15th consecutive weekly decline—easing landed costs for importers stocking up ahead of Q4. Offsetting that, USPS peak-season surcharges take effect Oct. 5 through Jan. 18 across Priority Mail, Ground Advantage, and Parcel Select, with increases tiered by zone and weight. For merchants, this likely means more aggressive rate shopping and a greater push toward pickup or locally fulfilled options, where feasible.

Consumer Pulse and ISM: Cautious Vibes

Consumer sentiment softened again, with the Conference Board index down to 94.2 in September and the University of Michigan’s final read at 55.1. The ISM manufacturing PMI ticked higher to 49.1, but remains in contraction territory.

For Shopify sellers, this backdrop signals cautious, selective shoppers—making promotions critical. The environment favors tighter merchandising, sharper creative, and surgical discounting over broad markdowns that risk eroding margins.

What to Watch Next Week—and How It Affects SHOP

- FOMC minutes (Wed, Oct. 8): With official data in limbo, the minutes from the Sept. 16–17 meeting will be scoured for how “modestly restrictive” policy still is and how comfortable the committee feels about cutting again without a complete data deck. A dovish-leaning tone supports long-duration multiples (SHOP’s included); a hawkish tint would likely pressure them.

- Promo sell-through (Oct. 5–12): I’ll be watching early commentary and third-party trackers around Target/Amazon/Walmart events. Strong unit growth with limited return rates would be incrementally bullish for Shopify’s Q4 GMV cadence. Weak sell-through or heavy discount dependency, however, would argue for a more promotional holiday, which could dent merchant gross margin (and, by extension, take-rate optics).

Is Shopify a Buy, Sell, or Hold?

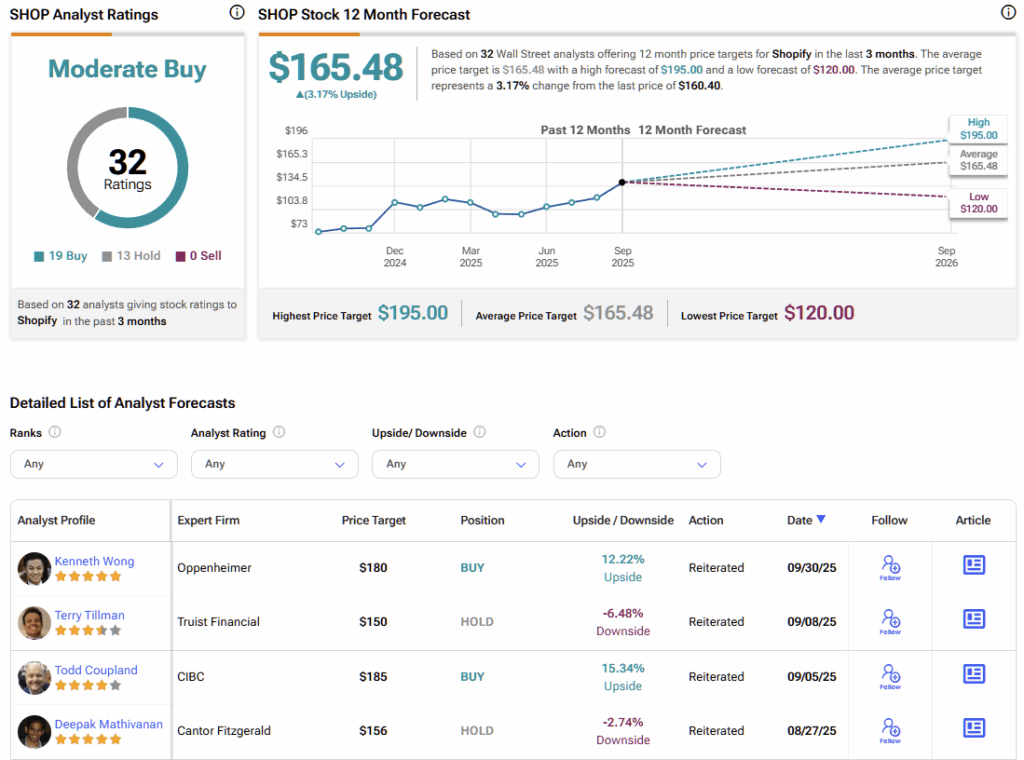

Wall Street remains relatively bullish on Shopify, with the stock carrying a Moderate Buy consensus rating based on 19 Buy and 13 Hold recommendations over the past three months. Not a single analyst is bearish on SHOP. In the meantime, SHOP’s average stock price target of $165.48 — which is a few cents higher from last week — suggests ~3% upside from current levels.

Why I Stay Bullish on SHOP Into Year-End

This week’s incremental news leans pragmatic: a new conversational-commerce on-ramp via ChatGPT, cheaper ocean freight, and a softer dollar and gasoline prices provide small but meaningful offsets to USPS peak surcharges and a still-cloudy macro backdrop.

I remain Bullish on SHOP, with near-term attention on two factors: (1) whether the ChatGPT channel delivers early conversion lift for merchants, and (2) how next week’s October promos drive GMV without eroding margins. Both will be critical to sustaining positive sentiment into year-end.