Procore Technologies (PCOR), a tech firm providing streamlined construction solutions, posted top-and-bottom-line beats for Q2. However, on the Q2 earnings call, management announced organizational changes that paused investors’ enthusiasm and caused the share price to drop over 20%. These changes are being made to help the organization surpass $1 billion in full-year revenue, which would increase the share price. Investors may want to monitor developments closely and look for signs that the realignment drives sales to higher levels.

Claim 30% Off TipRanks

- Unlock hedge fund-level data and powerful investing tools for smarter, sharper decisions

- Discover top-performing stock ideas and upgrade to a portfolio of market leaders with Smart Investor Picks

Procore’s Evolving Services

Procore Technologies is a player in the construction management software industry. Its cloud-based platform simplifies construction projects by facilitating collaboration between various stakeholders, including owners, contractors, architects, and engineers. Its services cater to the construction industry’s commercial, residential, industrial, and infrastructure sectors.

The company is making key changes to its go-to-market operating model. It is transitioning from a matrixed organization structure to a general manager model, a move adopted by companies of similar size globally to address coordination and alignment issues across departments in various geographies. This new model should enhance the speed at which the company can respond to customer needs by having combined teams reporting to general managers.

Procore’s Financial Results & Outlook

Procore delivered a strong performance in the second quarter of 2024, outpacing market expectations. The company reported revenue of $284 million, 24.3% higher than last year and exceeding analysts’ estimates by $8.77 million. The GAAP gross margin was 83%, and the non-GAAP gross margin was 87%. The GAAP operating margin was reported at -5%, and the non-GAAP operating margin was 17.6%. Lastly, earnings per share (EPS) of $0.39 beat consensus projections by $0.14.

Management has also issued guidance for Q3, projecting revenue from $286 million to $288 million, translating to a year-over-year growth of 15%-16%. The predicted non-GAAP operating margin for the same period is 9%-10%. For the full year 2024, management expects revenue to range between $1,141 million and $1,144 million, marking a year-over-year growth of 20%. The projected non-GAAP operating margin for the year stands at 10%-11%.

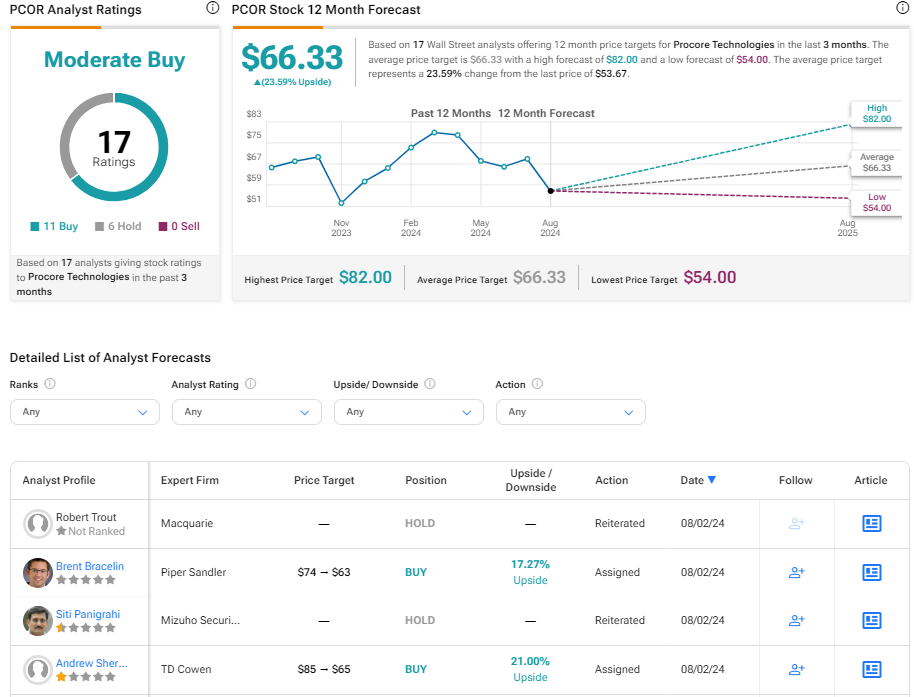

What Is the Price Target for PCOR Stock?

The stock has been volatile with a beta of 1.43. The stock was slightly up year-to-date before the post-Q2 earnings drop. It now trades toward the low end of its 52-week price range of $48.11 – $83.35 and demonstrates negative price momentum, trading below the 20-day (68.00) and 50-day (67.96) moving averages. Despite the recent price decline, the shares trade at a rich valuation relative to the Application Software industry, with a P/S ratio of 7.0x, compared to an industry average of 6.3x.

Analysts following the company have been cautiously optimistic about the stock, though many have shifted price targets downward since the Q2 earnings call. For example, KeyBanc analyst Jason Celino lowered the price target on the shares from $79 to $68 while maintaining an Overweight rating, noting that the unexpected organizational changes could impact near-term execution. However, he views the price pullback as a buying opportunity.

Based on the recommendations and price targets assigned by 17 analysts, Procore Technologies is rated a Moderate Buy overall. The average price target is $66.33, representing a potential 23.59% change from current levels.

Bottom Line on PCOR

Despite recent strong Q2 performance, organizational changes are causing investors to hesitate. The company’s realignment should optimize its ability to respond to customer needs and set it toward $1 billion in full-year revenue. The share price’s post-Q2 dip may be viewed as a buying opportunity, though as the shares trade at a premium, investors might want to observe progress toward sales growth first.