Shares in Microsoft (MSFT) sunk 2% in Tuesday’s after-hours trading despite the company posting a very strong earnings beat.

Meet Samuel – Your Personal Investing Prophet

- Start a conversation with TipRanks’ trusted, data-backed investment intelligence

- Ask Samuel about stocks, your portfolio, or the market and get instant, personalized insights in seconds

Specifically, FQ1 GAAP EPS of $1.82 beat Street consensus by $0.28. Similarly, revenue of $37.2B surged 12.4% year-over-year and topped consensus estimates by $1.42B. Operating income was $15.9B and increased 25% year-over-year.

Meanwhile the Intelligent Cloud (IC) segment reported revenue of $12.99B beating both guidance of $12.55-12.8B and the $12.73B Street consensus. And Azure growth of +47% CC came in a few points ahead of guidance/ expectations.

Revenue in Productivity and Business Processes (PBP) was $12.3 billion and increased 11% with Office Commercial products and cloud services revenue up 9% driven by Office 365 Commercial revenue growth of 21%.

“Demand for our cloud offerings drove a strong start to the fiscal year with our commercial cloud revenue generating $15.2 billion, up 31% year over year. We continue to invest against the significant opportunity ahead of us to drive long-term growth,” commented CFO Amy Hood.

Looking forward, guidance for 2Q21 slightly disappointed with implied Total Revenue of ~$40B (+8% Y/Y, vs. consensus +10% Y/Y), op. margins of 36.7% (vs. cons. 36.5%) and EPS of ~$1.62 (vs. cons. $1.61).

While MSFT did not formally guide to FY21, the company did note that it’s commercial segments (PBP and IC) will grow double digits in the fiscal year.

Following the report RBC Capital’s Alex Zukin reiterated his MSFT buy rating and $250 price target. He noted that shares dropped following the earnings call on “a combination of conservative revenue guidance (two of the segments were guided below consensus), deceleration in the implied Azure guide (~6pp by our estimates) and conservative FY21 commentary driven by MPC segment volatility.”

However the analyst is sticking to the bull side, telling investors: “Regardless of any near- term volatility in share price we continue to see a durable revenue and earnings compounder that is levered to some of the largest growth markets in software and would use any temporary weakness to add to positions.” (See MSFT stock analysis on TipRanks).

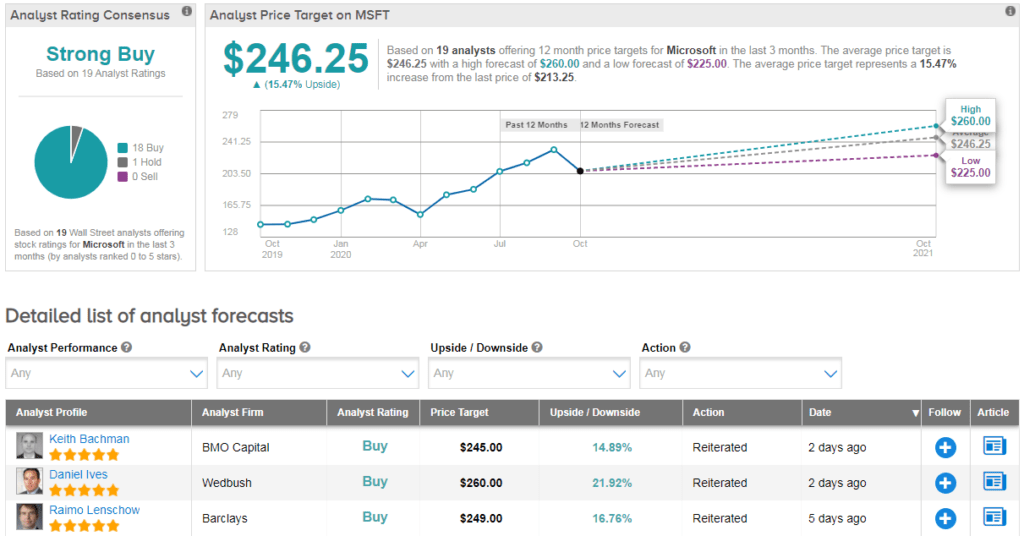

Overall, MSFT stock is trading up 35% year-to-date, and scores a bullish Strong Buy Street consensus. That’s with 18 recent buy ratings vs just 1 hold rating. The average analyst price target indicates 15% upside potential lies ahead.

Related News:

F5 Networks’ 1Q Outlook Beats The Street; Shares Gain 4.3%

Varonis Beats 3Q Profit Estimates; Shares Spike 9%

NXP Sees Higher 4Q Sales; Shares Rise