Medical Properties Trust (MPW), a REIT involved with medical properties (also known as MPT), recently reported its Q2-2024 earnings results, which I will discuss below. The quarterly results were characterized by significant asset impairments and valuation gains on asset sales. Furthermore, a reduction of the quarterly dividend to no more than $0.08/share was announced in a bid to preserve liquidity.

Claim 55% Off TipRanks

- Unlock hedge fund-level data and powerful investing tools for smarter, sharper decisions

- Discover top-performing stock ideas and upgrade to a portfolio of market leaders with Smart Investor Picks

Nevertheless, I am bullish on the stock due to its attractive valuation relative to private markets, with its debt-heavy capital structure well-positioned to benefit from Federal Reserve interest rate cuts in the next few years. That said, reducing leverage will remain a key priority for management in the years to come.

Medical Properties Trust’s Operational Overview

Medical Properties Trust, or MPT, is one of the largest owners of hospital real estate. As of Q2 2024, MPW managed a total of 435 properties. The significance of international operations increased following the latest asset sales in the United States, but international affairs are still less than half of the business.

MPT’s Q2-2024 results were characterized by continued impairments of about $700 million, primarily related to bankrupt tenant Steward Healthcare, but also gains on asset sales of $400 million. To adjust for these effects, MPT reports normalized funds from operations (an indicator similar to adjusted funds from operations, or AFFO, a cash-flow metric commonly reported by REITs).

In Q2 2024, normalized funds from operations were $0.23/share, down 52% year-over-year. The decrease was driven primarily by lower revenues due to asset disposals and Steward going into bankruptcy.

The company noted that the $0.23/share normalized funds from operations included a $0.01/share contribution from a joint venture in Massachusetts related to Steward. This contribution had to be written down due to the inability of the company and state regulators to find an acceptable way to restart Steward operations in the state.

As a result, the normalized funds from operations run rate is $0.22/share, with management optimistic about the restart of Steward facilities in other states.

Next, net debt amounted to $8.76 billion as the company finalized the sales of five Utah hospitals. Subsequent to quarter end, an additional $160 million in disposals were signed for seven freestanding emergency department facilities and one general acute hospital in Arizona. The capitalization rate achieved was below 7.5% — an attractive amount considering the company’s valuation.

Divided Cut Rationale

The other major announcement was a substantial reduction in the quarterly dividend to no more than $0.08/share until September 2025, with the caveat that the amount can be increased before that date if Steward’s hospitals are transitioned to new operators more rapidly.

The main factor driving the dividend cut is that even after the Arizona hospital sales, net debt will amount to $8.6 billion, or 76% of the company’s enterprise value. At the new dividend rate of about $0.08/share, the company will be able to retain about $300 million more annually to help pay down its massive debt pile.

This will also reduce the need to sell assets, which are likely to go up in value as the Federal Reserve potentially starts cutting interest rates in September 2024. In fact, current futures pricing predicts a Fed funds rate of about 3.25-3.50% in July 2025, some 2% lower than the current target range.

Given that the company has addressed all its 2024 debt maturities, refinancing its remaining debt down the line is likely to have a small impact on normalized funds from operations, assuming future interest rates fall as currently projected by the market, which is far from certain.

What Medical Properties’ Capitalization Rate Tells Us

It is always important to consider the capitalization rate (the rate of return on a real estate investment property based on its expected cash flows) of a REIT you invest in and not just the yield based on normalized funds from operations. Usually, to increase returns, REITs borrow from banks and other lenders. This often results in high normalized funds from operations yield.

However, if the REIT needs to sell a property on the market, the buyer will consider the capitalization rate, as it encompasses all cash flows of the property to equity and debt holders combined.

To arrive at Medical Properties Trust’s capitalization rate, we can combine the current normalized funds from operations run-rate amount and interest expense, multiply it by four since it is a quarterly number, and divide the result by the company’s enterprise value. Importantly, normalized funds from operations already exclude meaningful rent contributions from Steward Healthcare.

For Medical Properties Trust (MPT), the capitalization rate is calculated by annualizing the current quarterly normalized FFO run-rate and interest expenses, and then dividing by the enterprise value. In Q2 2024, MPT’s normalized FFO was $139 million, including $7 million from Massachusetts hospitals.

Adjusting for this, the quarterly run rate is $132 million ($528 million annual run rate). Combined with an interest expense of $101 million ($404 million annually), MPT produces about $932 million in annual cash flow. Given an enterprise value of about $11.5 billion, the market-implied capitalization rate is approximately 8.1%.

The capitalization rate allows investors to compare REITs with different levels of financial leverage (the portion of the enterprise value funded by debt, which, at Medical Properties Trust, is about 76%, a very high amount) since it looks at cash flows at the enterprise level rather than to shareholders specifically. The high amount of financial leverage exposes MPT to excessive interest rate risk.

The cap rate is also useful when comparing the absolute return potential of Medical Properties Trust as an investment and makes it easy to compare it to other alternatives, such as government bonds. For instance, the 10-year U.S. government bonds currently yield around 3.97%.

We can also use it to compare the company’s valuation relative to disposal prices achieved in private markets. Given the below 7.5% capitalization rate achieved on Arizona disposals, we can determine that Medical Properties Trust is undervalued. For instance, if the company were to trade at a market-implied cap rate of 7.5%, the share price would have to rise to $6.40/share.

We can arrive at the $6.40/share indicative target price by dividing the $932 million in annual cash flows against a required rate of return of 7.5%. We get an enterprise value of $12.43 billion or a market capitalization of $3.83 billion after deducting net debt of $8.6 billion. Finally, we divide the $3.83 billion market capitalization by the number of shares outstanding (600 million) and get a fair value of about $6.40/share.

Lastly, the 8.1% cap rate represents the expected return before considering leverage, inflation adjustments, or rental growth, and includes management overhead, unlike private market transactions that often exclude this cost.

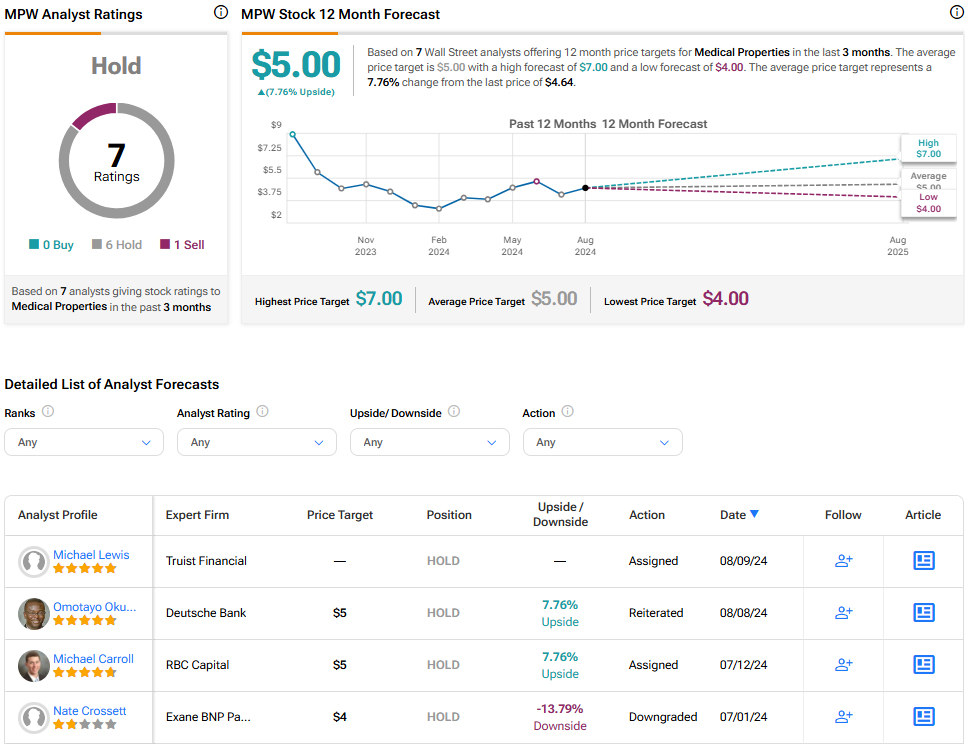

Is MPW Stock a Buy, According to Analysts?

Turning to Wall Street, Medical Properties Trust earns a Hold consensus rating based on zero Buys, six Holds, and one Sell rating. Additionally, Medical Properties stock’s average price target is $5.00, implying 4.38% upside potential.

The Takeaway

Medical Properties Trust’s Q2-2024 results were characterized by significant asset impairments and gains from asset sales. The company continues to access private markets at attractive terms to reduce its leverage, but it also cut its dividend to preserve liquidity and reduce the need for future asset sales.

I am bullish on MPW stock, as its enterprise-level valuation remains attractive relative to private markets. Further, the company’s debt-heavy capital structure will benefit immensely if the Federal Reserve cuts interest rates, as markets currently expect. With the dividend cut out of the way, I expect the stock to rise significantly over the next few years as its operations stabilize. Even so, the need to preserve liquidity will remain as the company slowly pays down debt.