If the Federal Reserve finally confirms the rumors and cuts the benchmark interest rate, one of the beneficiaries could be credit services giant Mastercard (MA). Previously, Mastercard benefited from Americans turning to credit cards to make ends meet. However, with lower rates, it may be easier for borrowers to pay back their debt, thus saving Mastercard from the hassles of debt collection and charge-offs. Therefore, I am bullish on MA stock.

Claim 30% Off TipRanks

- Unlock hedge fund-level data and powerful investing tools for smarter, sharper decisions

- Discover top-performing stock ideas and upgrade to a portfolio of market leaders with Smart Investor Picks

Likely Rate Cuts Should Benefit MA Stock in the Long Run

Although the concept of rate cuts has been rumored for some time, there’s a growing sense that the Fed is serious about implementing them sooner rather than later. In June, the central bank implied that at least one rate cut could be due this year. In the most recent meeting, policymakers decided to keep the benchmark rate unchanged at 5.5%, per expectations.

However, the latest jobs report may have sparked a sense of urgency within the Fed. As TipRanks reporter Radhika Saraogi mentioned, in July, “Employers added 114,000 jobs compared to June’s revised gain of 179,000, which was way below the 176,000 jobs economists had anticipated. Adding to the negativity, the unemployment rate unexpectedly increased to 4.3% from 4.1% in the previous month, which stoked recession fears among investors.”

In other words, the Fed may have played coy about its monetary policy for too long. Concerns now exist on Wall Street that the central bank was far too cautious in using its influence to stimulate the economy. While policymakers have long talked about a soft landing for the economy, rising unemployment along with mass layoffs suggest that a lack of decisive action could indeed lead to a recession.

Therefore, it’s possible that the Fed is done playing games: it’s going to lower interest rates and do so right quick. That may ultimately benefit MA stock in the long run.

Previously, Mastercard represented somewhat of a beneficiary. Due to blistering inflation outpacing wage growth, many households turned to debt financing to stretch their budget. Predictably, this dynamic led to a skyrocketing of credit card balances in excess of $1 trillion. Such a framework helped boost the top and bottom lines of MA stock.

However, credit service firms later suffered from delinquencies and charge-offs. The latter accounting term refers to a situation where creditors believe that an underlying debt will unlikely be addressed and, therefore, must be written off. Even in cases where debt can be collected, it’s always a hassle to get the money owed.

Therefore, with the prospect that lower benchmark rates can help decrease the rate that card issuers charge, Mastercard is in a solid position to help its customers and, in doing so, help itself.

Financial Backdrop Looks Compelling for Mastercard

By logical deduction, lower rates should trickle down to lower financing costs for borrowers. That should provide MA stock with two benefits: reduce the number of delinquencies or other unfavorable events or actions (such as charge-offs) and encourage new borrowing. As such, analysts’ forward projections appear credible.

For Fiscal 2024, market experts believe that Mastercard’s earnings per share might land at $14.30, up 16.64% from last year’s print of $12.26. In the following year, EPS could potentially rise to $16.63, with a high-side estimate of $17.23.

On the top line, Fiscal 2024 revenue could clock in at $27.93 billion, up 11.3% from the prior year’s tally of $25.1 billion. In 2025, sales may expand to $31.33 billion, with an optimistic view of $31.8 billion.

Historically, Mastercard seems more than capable of delivering such numbers. For example, in the past year since the second quarter, the company posted an average EPS of $3.29. In contrast, analysts anticipated an average earnings of $3.19 per share. On the revenue front, the company has been consistently beating its sales targets from at least Q2 2022.

Now, if there is a detracting point about MA stock, it would be the valuation. Right now, shares trade hands at 16.2x trailing-year sales. That’s well above the credit service industry’s average multiple of 1.97x. That said, Mastercard commands a 25.5% market share of the U.S. credit card ecosystem, coming second to only Visa (V). Given the footprint and the reliable income stream, MA arguably deserves its premium.

Plus, an interest rate cut by the Fed won’t suddenly mean a paradigm shift where Americans refuse to use plastic. Instead, the reduced borrowing costs would make it easier for people to deal with their debt load. Ultimately, that should be helpful to MA stock, as it would mean fewer headaches chasing folks for money owed.

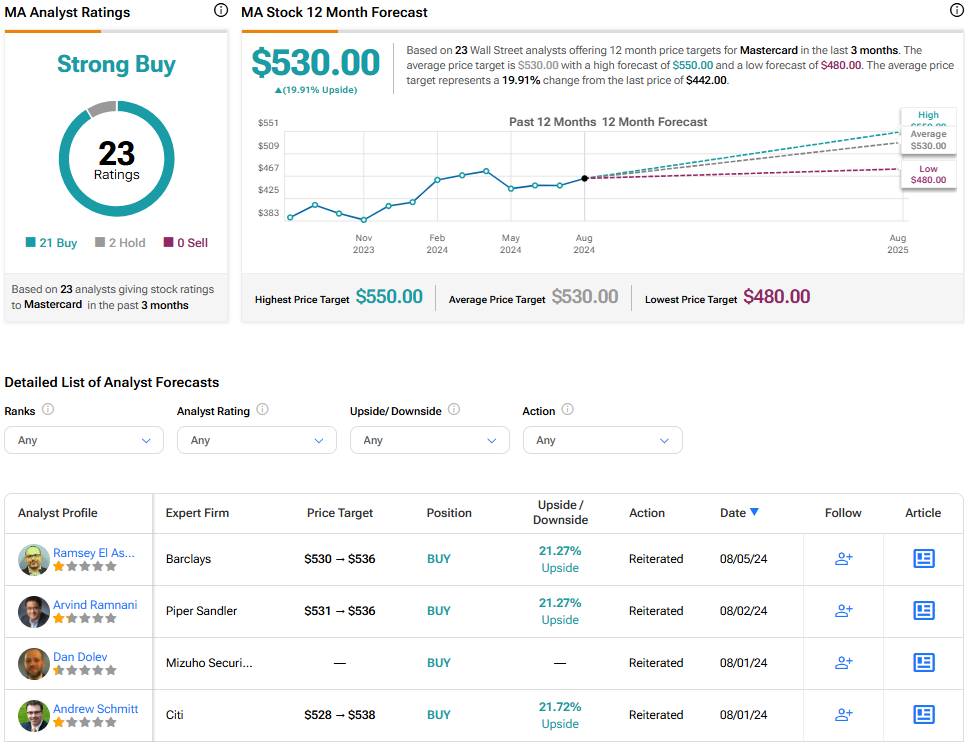

Is MA Stock a Buy, According to Analysts?

Turning to Wall Street, MA stock has a Strong Buy consensus rating based on 21 Buys, two Holds, and zero Sell ratings. The average Mastercard stock price target is $530, implying 19.9% upside potential.

The Takeaway: A Monetary Policy Shift Could Provide a Boost for MA Stock

While the Federal Reserve has been reluctant to reduce interest rates prematurely, signs of economic challenges may force a sense of urgency. If so, the much-rumored rate cuts could arrive sooner rather than later, which may benefit Mastercard. Thanks to lower borrowing costs, cardholders may be better able to pay off their debts, reducing headaches for the credit services firm. Plus, lower rates may encourage new borrowing, thus bolstering the financials undergirding MA stock.