LVMH Moet Hennessy Louis Vuitton (FR:MC) (LVMUY), the world-famous luxury conglomerate, has been experiencing slower growth over the last 12 months compared to historically. However, current conditions are likely to ease. As a result of the lower demand in the luxury market, LVMH stock has dropped 24% from its all-time high. This opens up a significant long-term value opportunity, and its all-time high could be reached again in 12 months and sustained over the long term. Therefore, I am bullish on LVMH stock.

Meet Samuel – Your Personal Investing Prophet

- Start a conversation with TipRanks’ trusted, data-backed investment intelligence

- Ask Samuel about stocks, your portfolio, or the market and get instant, personalized insights in seconds

Broad Luxury Market Slowdown Inhibits Growth

China has historically been a significant driver of growth for luxury brands, including LVMH. However, weaker asset markets and subdued consumer confidence in the country have tempered spending among affluent Chinese consumers. While there is some latent demand, the recovery has been slower than anticipated.

Furthermore, inflation, interest rate hikes, and geopolitical tensions have lowered the broader consumer sentiment for luxury goods, particularly in key markets like Europe and the U.S.

LVMH’s recent fundamental growth is often compared to the exceptionally high rates seen post-pandemic, when demand surged as economies reopened. For example, the Fashion and Leather Goods division reported a deceleration from high single-digit growth in previous quarters to just 2% in Q1.

In addition, the Wines and Spirits division saw a 12% decline in revenues in Q1. While the 11% increase in organic revenues in Selective Retailing, driven by Sephora, was strong, it was not enough to offset declines in other areas.

Undervaluation Opportunity and Long-Term Growth Catalysts

If the company achieves its 10-year average EPS (without non-recurring items) growth rate of 16.9% annually from 2024-2034 and just 4% annually from 2034-2044, the stock is undervalued by approximately 22% based on discounted earnings analysis. This includes the company’s weighted average cost of capital of 9.55% as the discount rate.

The discounted earnings analysis certainly adds a margin of safety to the investment thesis, but what I think is even more promising is the long-term potential for higher growth rates to resume. LVMH’s future strategy is significantly hinged on Gen Z consumers, who are expected to account for 70% of luxury spending by 2025. Management is positioning brands like Off-White and KidSuper to capture a significant share of this growing market segment.

I think that as younger generations (who are much more willing to spend on luxury goods) age, the market here could compound significantly. In other words, LVMH is strategically raising a generation on its brands, which could expand as their budgets increase with age.

There is also the broader macroeconomic question, including interest rates and inflation, which I mentioned previously. While this does not affect the upper class as much as the middle and lower classes, the impact is still felt. In addition, a substantial portion of upper-middle-class customers would likely have dropped out of the luxury market completely as the economy tightened.

Moving forward, the economy could begin to ease over the next few years, both in the United States and abroad. Recent data suggests that inflation is beginning to moderate, and the Federal Reserve has implemented interest rate hikes to control inflation. The European Union, China, and emerging markets are also managing to sustain what looks like moderate future economic growth over the next five to 10 years.

Risks and the Long-Term Holding Strategy

Despite my optimism for LVMH over the next five to 10 years, there is currently a risk of further geopolitical upheaval on a more severe scale. If this were to happen, it is conceivable that supply chains would be disrupted, and luxury goods would become far less in demand due to further budgetary constraints. Moreover, international trade could be severely controlled.

However, geopolitical tensions have the potential to cause largely sector-independent recessions, and simply holding cash would negate a large amount of potential growth and expose capital to high inflation. The threat is likely not high enough to deter investing as a whole right now, so I remain bullish on LVMH and many other non-defense stocks.

LVMH could be bought at the present valuation and achieve 12-month price growth of circa 25% as the market for luxury goods begins to expand. Over a longer time frame of 10 years, a CAGR of roughly 15% seems achievable to me. Therefore, this is not a high long-term alpha opportunity, but it is a stable investment, and the near-term alpha potential is significant based on the present undervaluation.

LVMH Is a Buy, According to Analysts?

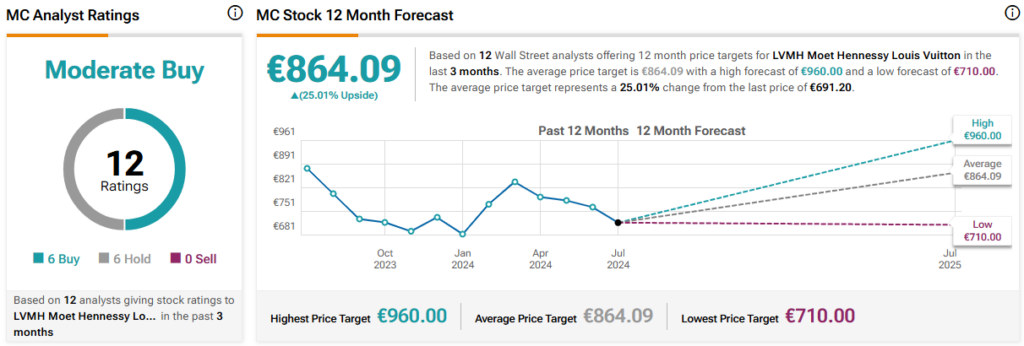

Turning to Wall Street, LVMH has a Moderate Buy consensus rating based on six Buys, six Holds, and zero Sells assigned in the last three months. At €864.09, the average LVMH price target implies ~25% upside potential.

The Bottom Line on LVMH Stock

LVMH is currently a value opportunity, and whether investors choose to hold it for 12 months for shorter-term alpha or many years as a stable investment, the rewards currently outweigh the risks. I think my 15% price CAGR could be easily outperformed if the company manages to capitalize on the Gen Z market and further consolidate itself internationally; therefore, my estimate is conservative.