Within the online travel agency space, by a significant margin, no one connects as many travelers around the world as Booking Holdings (BKNG) does. Booking’s investment thesis is anchored in its unparalleled global reach and its leadership position in the online travel industry. Despite operating in a highly cyclical sector, the company’s extensive geographic diversification and its high-margin, asset-light business model give it a degree of defensiveness uncommon in the space—qualities that arguably support its premium valuation.

Claim 55% Off TipRanks

- Unlock hedge fund-level data and powerful investing tools for smarter, sharper decisions

- Discover top-performing stock ideas and upgrade to a portfolio of market leaders with Smart Investor Picks

BKNG’s stock price has grown 13% year-to-date and almost 200% over the past three years, suggesting an almighty up-trend is here to stay.

That said, Booking’s stock is expensive, and this remains a key hurdle to a more consistently bullish outlook. Given the company’s strong track record and the market’s high expectations, the investment case becomes increasingly sensitive to even modest disappointments. Results that fail to meet or exceed the upper end of guidance could undermine confidence in the near term.

While I continue to view Booking as a structurally sound, long-term outperformer due to its ability to consistently generate value, the current valuation suggests the stock may be vulnerable to a short- to mid-term pullback. With limited near-term upside, a Hold rating appears appropriate at this time.

Booking and Travel Experience Parallel Rebound

Taking a step back to a broader view, the travel sector has rallied in line with the overall market. However, some fundamental headwinds are beginning to re-emerge. This is especially true for airlines, particularly in the U.S., where carriers had been actively cutting capacity in anticipation of softer demand. Hotel average daily rates (ADR) have also shown volatility for some industry players, pressured by weaker consumer spending and a more devalued dollar, especially for companies with less international exposure.

In contrast, Booking has performed well, mainly because it’s significantly less reliant on the U.S. domestic market compared to many of its peers. According to TipRanks market data, the stock has outperformed the S&P 500 (SPX) in the past three months, supported by solid fundamentals that have remained in line with guidance.

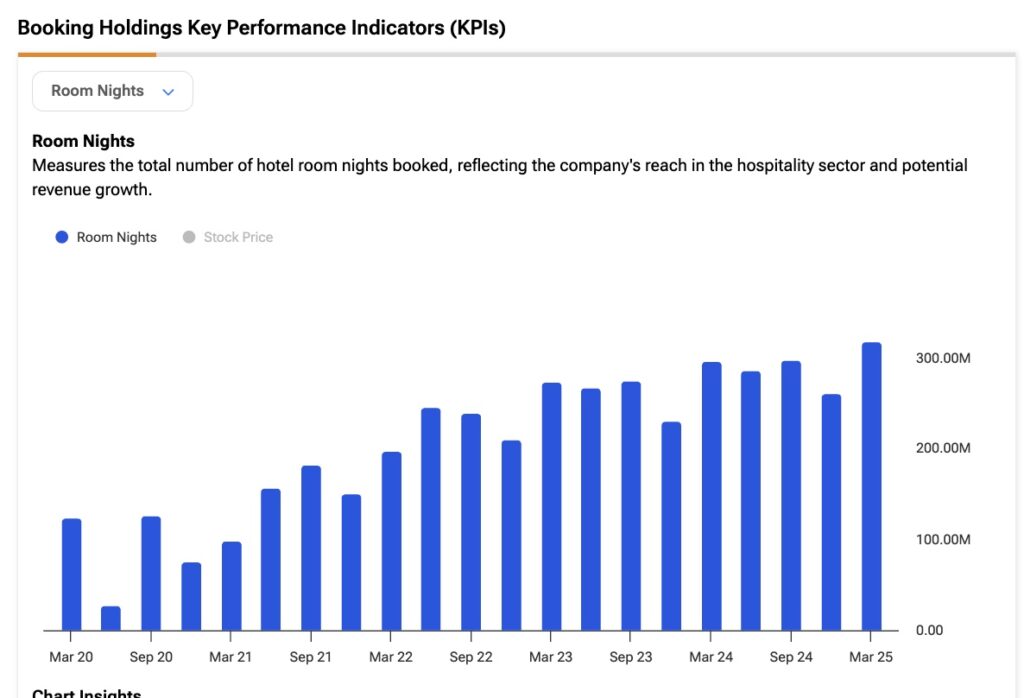

One of the highlights of the quarter was the company reporting 319 million room nights in Q1, a strong result in a challenging environment, up 7% year-over-year from 300 million, although slightly below the high end of guidance. Gross bookings also grew 7% YoY to $46.7 billion, thanks to Booking’s highly diversified global footprint.

On the bottom line, adjusted EPS came in at $24.81, reflecting a solid 22% increase year-over-year. Free cash flow followed a similar trajectory, reaching $3.2 billion, up 23% from the prior year.

This strong profitability reflects Booking’s ability to drive high volumes of transactions at robust operating margins, currently at 22.3%. As an asset-light platform business with strong operational efficiency, Booking consistently converts a large share of its profits into free cash flow, ultimately translating into more long-term value for shareholders.

Why BKNG’s Capital Efficiency Stands Out

When evaluating a company with a high and steadily growing capacity to generate free cash flow, much of that strength can be attributed to Booking’s consistently impressive return on invested capital (ROIC).

Using the traditional ROIC formula—NOPAT (the net operating profit after tax) divided by invested capital—we get a clear picture. Based on the $7.89 billion in EBIT generated over the last twelve months, and applying a tax rate of 19.4%, Booking’s NOPAT comes out to $6.36 billion for the period.

Now, considering invested capital, which refers to the total capital committed to the company’s core business, even as an asset-light company, Booking operates with a notably negative operating net working capital of approximately $11 billion. This significantly lowers its capital base. Adding back the other long-term operating assets (such as property, plant, and equipment and intangibles), we arrive at an invested capital figure of approximately $11.1 billion.

Combining these numbers yields an ROIC of approximately 57%—an exceptionally high return. To put that in perspective, if we assume a weighted average cost of capital (WACC) of around 8%, Booking is generating returns far above its cost of capital. That means the company isn’t just covering its cost of capital, but it’s creating substantial economic value for shareholders. While this is hardly breaking news to anyone following the stock, it strongly reinforces the bullish, value-oriented case for BKNG.

Quality Commands a Premium Valuation

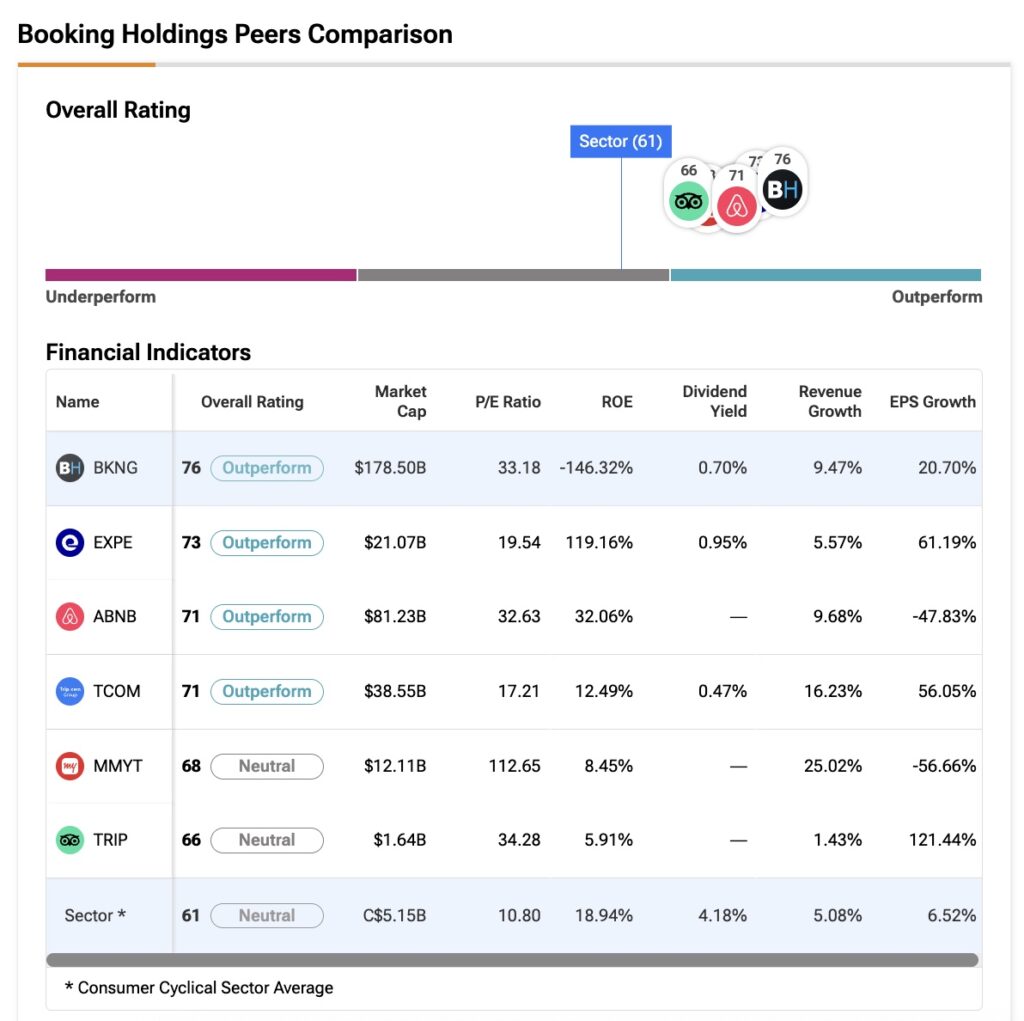

Naturally, a business with this level of operational quality comes at the cost of trading at arguably stretched valuation multiples. For example, compared to Expedia (EXPE)—which operates a similar OTA (online travel agency) model but is smaller in scale—Booking trades at a forward P/E of 25x, more than double Expedia’s 11x based on Fiscal 2025 estimates.

Even relative to its own historical average, Booking is trading about 17% above its five-year average multiple, reflecting, in my view, a premium tied to the perception of lower risk and higher execution consistency. It’s a high bar for a high-quality company, and the market seems to be pricing in very few chances of underperformance.

Another useful complementary metric in Booking’s case—especially given its clean capital structure and net cash position—is earnings yield based on enterprise value. Since the company has little to no net debt, its enterprise value is essentially equal to its market capitalization, which means the operating earnings yield serves as a good proxy for the return on capital from another perspective.

For instance, over the last twelve months, Booking’s earnings yield stood at 4.5%, based on $7.8 billion in operating profit and an enterprise value of $179.4 billion.

That yield is well below the company’s estimated WACC, reinforcing the idea that Booking is far from cheap and that near-term upside appears limited. In that sense, there’s a low margin of safety in going long at these levels, even though the business remains structurally excellent.

What is the Stock Market Prediction for BKNG?

The market consensus on BKNG remains mostly bullish, with 18 out of 28 analysts rating the stock a Buy, while the remaining ten maintain a Hold. That said, valuations don’t exactly scream “cheap” at current levels. In fact, the average price target of $5,489.22 implies a modest 2.5% downside from the latest share price.

Booking’s Pricey Levels Have the Stock on Edge

Booking is currently priced for perfection, and that sets a high bar that could limit the upside from here, especially in a sector as cyclical as travel. Even so, Booking remains the most defensive name among its peers, thanks to its global scale, asset-light model, and strong execution.

For now, supportive macro rebound trends and the company’s highly efficient metrics help sustain the bullish momentum. Still, at current levels, I don’t see much of a margin of safety to justify going long with greater confidence.