Despite posting top-and-bottom-line beats, footwear giant Crocs (CROX) has encountered a rough patch after the release of its third-quarter earnings report, as shares have fallen by over 15%. The company’s downward revision of the full-year revenue forecast for its brand, HEYDUDE, has particularly raised concerns among investors, with the anticipated full-year sales drop of 14.5% marking a steeper decline than previously predicted.

Claim 55% Off TipRanks

- Unlock hedge fund-level data and powerful investing tools for smarter, sharper decisions

- Discover top-performing stock ideas and upgrade to a portfolio of market leaders with Smart Investor Picks

The outlook for the HEYDUDE brand remains uncertain, causing analysts to lower their projections for the company’s future performance in the near term. However, the Crocs brand remains strong overall, and value-oriented investors might find this a tempting buy-on-the-dip opportunity.

Analysis of Crocs’ Recent Results

Crocs produces and sells casual footwear and lifestyle accessories under the Crocs and HEYDUDE brands. Its product portfolio ranges from clogs and sandals to sneakers and slippers. The company targets different demographic segments—men, women, and children. It utilizes various distribution channels to reach its customers, encompassing online and offline avenues such as wholesalers, retail stores, e-commerce sites, third-party marketplaces, and kiosks/store-in-store locations.

The company reported that consolidated revenues grew by 1.6% in the third quarter to reach $1.06 billion, with Direct-to-Consumer (DTC) revenues rising by 4.4, while wholesale revenues decreased by 1.4%. The gross margin improved to 59.6% from 55.6%. However, selling, general, and administrative expenses saw a spike of 18.1%, representing 34.2% of revenues, rising from 29.4%. The operating income of $270 million marked a 1.5% decrease, whereas earnings per share (EPS) of $3.60 exceeded estimates by $0.49.

As of the quarter’s end, the company had cash and cash equivalents of $186 million compared to $127 million in the previous year. Inventories were at $367 million, down from $390 million the previous year. Total borrowings were $1.42 billion, a substantial decrease from $1.94 billion in 2023.

Looking ahead to the fourth quarter, CROX’s management expects revenues to remain flat or increase slightly compared to the fourth quarter of 2023. The Crocs brand is predicted to grow approximately 2% while the HEYDUDE brand is expected to decline by 4% to 6%. The company’s outlook for the 2024 Fiscal year anticipates revenue growth of 3% compared to 2023, alongside an 8% growth in revenues for the Crocs brand and a decrease of roughly 14.5% for the HEYDUDE brand.

Is CROX a Buy?

The stock has been on an upward trajectory, climbing roughly 25% over the past year. It trades near the middle of its 52-week price range of $74.00 – $165.32 and shows negative price momentum by trading below its 20-day (134.17) and 50-day (136.30) moving averages. Yet, with a P/E ratio of 8.4x, it appears to be trading at a steep discount to the Footwear & Accessories industry average P/E of 27.67x.

Analysts following the company have maintained a bullish posture on CROX stock while trimming their price targets. For example, despite maintaining a Buy rating, BofA Securities has cut the price target for Crocs’ shares from $179 to $149. Similarly, Barclays has lowered its price target for Crocs from $164 to $125 but retains an Overweight rating on the shares.

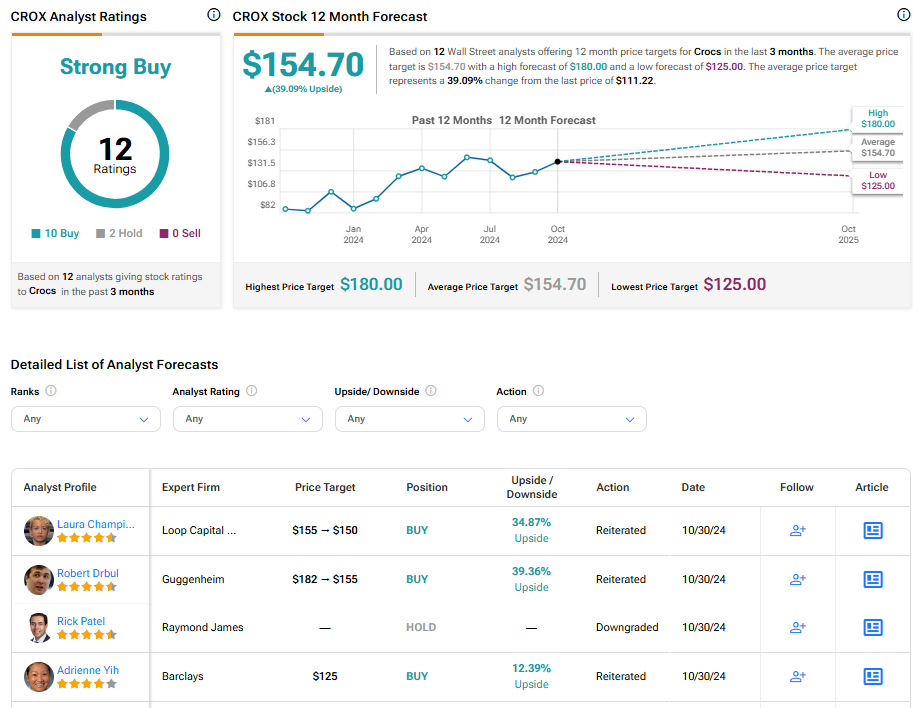

Crocs is rated a Strong Buy overall, based on the cumulative recommendations of 12 analysts. Their average price target for CROX stock is $154.70, representing a potential upside of 39.09% from current levels.

Final Considerations on CROX

Despite recent disappointing forecasts for the HEYDUDE brand, Crocs continues to demonstrate resilience with steady growth in consolidated revenues, an improved gross margin, and a significant decrease in total borrowings. While investors may want to continue monitoring HEYDUDE’s trajectory, the Crocs brand’s solid fundamentals and robust performance, coupled with an attractive valuation, may present a captivating buying opportunity for value-oriented investors on the prowl for a potential rebound.