Intel (INTC), the long-established semiconductor company, recently fell 40% in price in just one month after a weak earnings report that significantly underperformed expectations. Management has lost investors’ confidence following this report, but it is still committed to developing a competitive foundry model to compete with other industry leaders. As a result, I am bullish on INTC despite the high risk the investment entails.

Claim 30% Off TipRanks

New trading tool for NVDA bearsIntel Is Potentially Significantly Undervalued

In my opinion, INTC stock is one of the most undervalued stocks in the semiconductor sector at the moment.

The company is strategically investing in its long-term future, particularly in artificial intelligence and chip manufacturing within the U.S. It might take some time. Still, I believe management is setting the company up for potentially strong long-term success.

Intel has a long history of innovation and market leadership, so I believe its extensive experience and infrastructure could enable it to capitalize on the growing demand for semiconductors related to AI. However, it faces competition from newer companies that have developed more robust moats in a shorter time.

The Company Faces Competitive Risks

As mentioned above, Intel is facing strong competition from companies like AMD (AMD) and Nvidia (NVDA) and intense market pressure from Taiwan’s famous Semiconductor Manufacturing (TSM). Contrary to Intel’s declining revenues and increasing debt, companies like TSM and Nvidia are growing exponentially, increasing margins, and becoming increasingly monopolistic. In my opinion this is a serious threat to Intel’s long-term success.

As the company may face further delays in manufacturing capacity expansion, Intel could conceivably be a value trap investment. For comparison, Intel’s three-year revenue growth rate is -11.2%, while TSMC’s is 17.3%.

Furthermore, the company announced the suspension of its dividend payments starting in Q4 2024, which will likely continue to sustain negative sentiment in the near term. The company faces significant execution risks, with ambitious initiatives such as the “five nodes in four years” initiative.

Past delays and manufacturing struggles affect investor confidence, and buying Intel stock for the long term is a bet on management’s ability to execute in a highly competitive environment.

Intel’s 18A Strategy

To stake a bullish position on INTC stock this days takes courage and belief, just like Intel’s 18A strategy. According to the company, 18A is a vital element of its roadmap to regain a leading position in semiconductor manufacturing and compete in the foundry market. Implementing cutting-edge technologies like RibbonFET (gate-all-around transistors) and PowerVia (backside power delivery) aims to offer superior performance and power efficiency to support high-performance computing demands.

The 18A node and strategy are part of its broader IDM 2.0 initiative and are essential for the company to compete with TSMC and Samsung (SMSN). If management successfully executes its 18A strategy, Intel could become the number two foundry by 2030.

This strategy is crucial for Intel and for manufacturing growth in the West to combat China’s play for global economic leadership. Intel is a beneficiary of the U.S. government’s CHIPS Act, which aims to strengthen domestic semiconductor manufacturing.

I believe governments in the West could become more pronounced in their support for Intel over the next decade, potentially supporting a rebound for the company from the present lows in financials and investors’ sentiment.

What Does Wall Street Say About Intel?

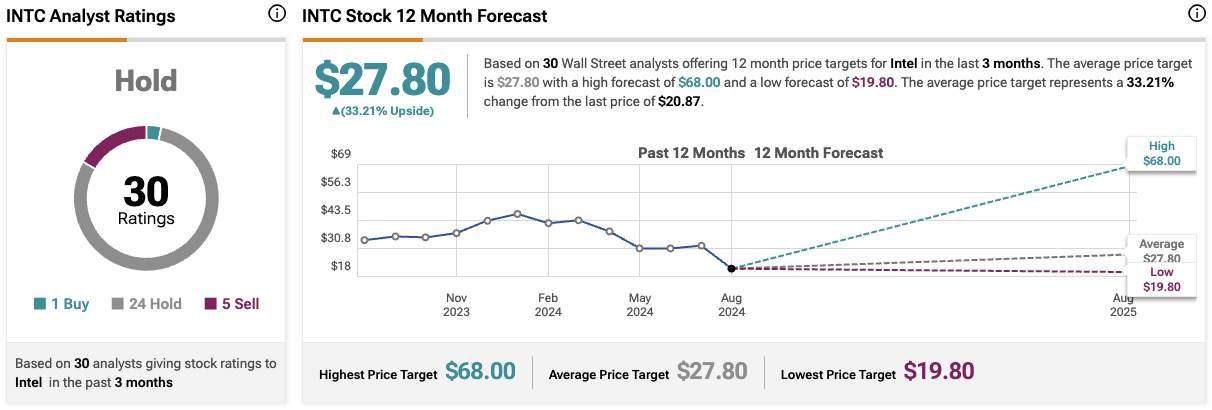

Turning to Wall Street, INTC stock is rated a Hold on consensus, with the average analyst 12-month price target of $27.80 indicating a potential 33.2% upside. Intel stock has one Buy rating, 24 Hold ratings, and five Sell ratings.

The relatively moderate sentiment from Wall Street on Intel is warranted because the investment is currently high risk. That being said, high risk often comes with high reward. I believe outsized returns are possible if one buys the stock now because its 18A strategy could lead to a competitive global foundry presence. This high upside potential is given credence by the one analyst who estimates a potential 12-month price of $68 is achievable.

Takeaway

INTC stock is potentially significantly undervalued, but it is also a high-risk play that has the potential to be a value trap. Whether the investment’s long-term returns are substantial or moderate depends on how management executes its 18A strategy and whether it positions itself as the West’s leading foundry.

In conclusion, I am bullish on Intel and believe that its management can put the company back on the competitive rails again. Therefore, I consider Intel to be a buy.