Despite a challenging 2024, indie Semiconductor(INDI) anticipates substantial growth in 2025 and beyond, mainly due to the rising demand for electric vehicles (EVs) and autonomous vehicles (AVs). The company is a leader in crafting next-generation semiconductors, photonics, and software platforms to drive the automotive revolution in vision and radar for advanced driver-assistance systems (ADAS).

Claim 30% Off TipRanks

- Unlock hedge fund-level data and powerful investing tools for smarter, sharper decisions

- Discover top-performing stock ideas and upgrade to a portfolio of market leaders with Smart Investor Picks

The company boasts a strategic backlog of $7.1 billion, which it projects will fuel a revenue surge of over 40%, surpassing $300 million, helping the company achieve breakeven and eliminate the need for additional capital in 2025. The stock trades at an attractive valuation, making it a potentially appealing option for investors interested in the growing ecosystem enabling the next generation of smart vehicles.

A Pioneer in a Growing Market

Indie Semiconductor develops high-performance, energy-efficient technology for Advanced Driver-Assistance Systems (ADAS), in-cabin user experiences, and electrification applications. Its mixed-signal System-on-Chips (SoCs) supports various edge sensors, including Radar, LiDAR, Ultrasound, and Computer Vision. Clients include leading automotive Original Equipment Manufacturers (OEMs) around the world.

The company has recently launched a safety-integrated chip (IC) for vehicle powertrain applications. The IC has been certified by SGS-TÜV Saar as ASIL-D, the highest safety level in the ISO 26262 standard, ensuring the highest level of functional safety. Indie has also extended its photonics offerings to include in-house integration, packaging, and system test capabilities.

These developments will cater to the growing market for optical components in automotive applications, which will be valued at an estimated $6.5 billion in 2023. The company expects the first production deployments of its safety IC and commercial photonics integration solutions in the second half of 2025.

A Substantial Backlog Suggests Strong Growth Potential in 2025

Indie Semiconductor recently reported Q3 results. Revenue of $53.97 million surpassed analysts’ forecasts by $0.39 million while marking a year-over-year decrease of 10.8%. The non-GAAP gross margin for the quarter increased to 50.4%. At the same time, the GAAP operating loss of $49.9 million was a substantial decline from the $136.2 million loss reported in the same period a year ago. The GAAP loss per share was $0.09, which aligned with expectations.

The growing demand for advanced driver-assistance systems (ADAS), in-cabin user experience, and electrification has helped drive the 12% year-over-year increase in the strategic backlog, currently at $7.1 billion. Management expects revenue to increase by over 7% in Q4 2024 and anticipates a return to an industry-leading growth trajectory in 2025 and beyond.

The Shares Reflect Positive Momentum and Value

The stock has been highly volatile, sporting a beta of 2.64, traveling downward and shedding 33% over the past year. Yet, while it trades near the lower end of its 52-week price range of $3.16 – $7.82, a recent rebound in the shares — up 23% in the past three months, has it showing positive price momentum by trading above the 20-day (4.27) and 50-day (4.28) moving averages. It trades at a relative discount to industry peers, with its P/S ratio of 1.74x, below the Information Technology sector average of 3.43x.

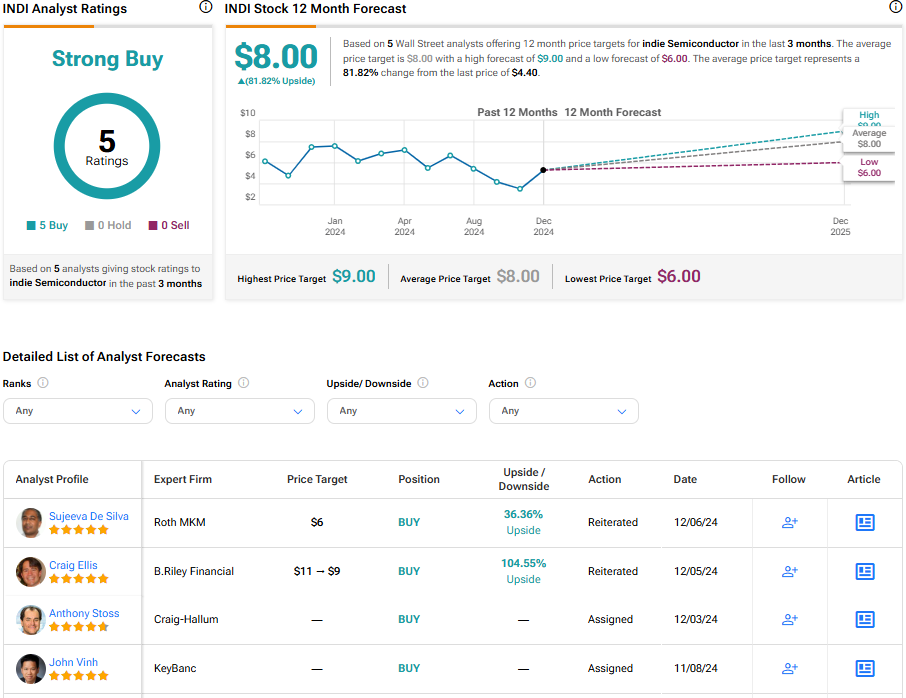

Analysts following the company have been bullish on INDI stock. For example, Roth MKM’s Sujeeva De Silva recently reiterated a Buy rating on the shares while raising the price target to $6, noting the company’s opportunities to drive growth across auto user experience and safety applications in the next several quarters.

Indie Semiconductor is rated a Strong Buy overall, based on the recent recommendations of five analysts. The average price target for INDI stock over the next 12 months is $8.00, representing a potential upside of 81.82% from current levels.

Indie Semiconductor in Summary

Indie Semiconductor is poised for significant growth in 2025 and beyond, fueled by the burgeoning demand for EVs and AVs and the company’s robust $7.1 billion backlog. With projections of revenue exceeding $300 million and a path toward breaking even in 2025, indie is an intriguing prospect for investors intrigued by the cutting-edge development of smart vehicles.