Uber Technologies (UBER), the leading ridesharing company in the world, has seen a remarkable comeback from pandemic lows, as it turned profitable last year on the back of stellar revenue growth. The firm is shaping up to become a major wealth distributor in the long run, which is evident from the characteristics it shares with other leading wealth distributors. Uber’s aggressive expansion into new business verticals is also gaining steam, aided by the company’s commitment to innovation. I am bullish on Uber as I believe the company’s diversification efforts will lead to robust earnings growth.

Claim 30% Off TipRanks

- Unlock hedge fund-level data and powerful investing tools for smarter, sharper decisions

- Discover top-performing stock ideas and upgrade to a portfolio of market leaders with Smart Investor Picks

Uber Is Expanding Its Autonomous Ridehailing Business

My bullish stance for Uber primarily stems from the company’s diversification efforts that position it to benefit from technological advancements. In October 2023, the company partnered with Waymo to offer autonomous rides in Phoenix. In a major promising development, Uber announced last week that consumers in Atlanta and Austin, Texas, will also be able to hail Waymo autonomous rides on the Uber app starting in the first quarter of 2025. The expected success in these markets should create a platform for a nationwide launch of AV (autonomous vehicle) rides, subject to regulatory approvals.

Uber has been looking for strategic partners to expand its AV business. Examples include the company’s recent investment in Wayve, a UK-based tech company that develops embodied AI products for the autonomous driving industry. In addition to this, Uber has secured partnerships with General Motors (GM) and BYD Company Limited (BYDDF). These partnerships aim to boost Uber’s fleet of EVs and AVs, which is integral to the growth of its autonomous ridehailing business.

Uber’s ambitious AV expansion strategy bodes well with industry predictions for the exponential growth of this market segment. For instance, Cathie Wood’s Ark Invest projects the global autonomous ridehailing market to create $14 trillion in enterprise value through 2028 based on market revenue of $4 trillion. Ark believes widespread commercial adoption of autonomous ridehailing is just around the corner.

The Advertisement Business Boosts Uber’s Earnings Potential

Uber’s profitable expansion into the advertisement business is another positive development that has contributed to my bullish stance. Uber’s annualized advertising revenue run rate reached $900 million in 2023, almost doubling from the $500 million reported in the previous year. CEO Dara Khosrowshahi, speaking at the Goldman Sachs Communacopia & Technology Conference last week, claimed that Uber is now expanding into sponsor listing as well. According to CEO Khosrowshahi, this is a highly profitable business segment.

When Uber launched its advertisement business two years ago, the company had an initial goal of hitting an annualized revenue run rate of $1 billion by the end of this year. In early August, Uber reached this milestone ahead of its original timeline. The rapid growth of programmatic ads and playable ads contributed to this growth, while the company’s ad performance measurement tools attracted marketers.

To build on the strong momentum of the advertising business, Uber is focused on securing strategic partnerships with key industry players. As part of this strategy, the company partnered with T-Mobile US (TMUS) to offer in-car JourneyTV in approximately 50,000 vehicles by the end of this year. Since the advertising business enjoys higher profit margins compared to food delivery and ridesharing, Uber’s profitability is likely to improve with the growth of this business segment.

Uber Shares Several Characteristics with Leading Wealth Distributors

Uber’s diversification efforts discussed earlier set the foundation for the company to emerge as a highly diversified business in the long run, which is a common characteristic shared by large-scale companies that reward investors handsomely through dividends and stock buybacks. Uber’s dominance in the global ridesharing sector also paints a promising picture, as this industry is expected to grow at a CAGR of almost 19% through 2032 to reach a value of $480 billion, according to Fortune Business Insights.

Uber’s improving cash flow profile is another reason to believe the company is emerging as a future wealth distributor. The company first turned free cash flow positive in late 2021. Uber reported free cash flows of $1.4 billion and $1.7 billion for the first and second quarters of this year, respectively, suggesting that the company is well on track to exceed $5 billion in annual free cash flow.

One of the key factors contributing to this substantial growth in free cash flows is the company’s new business strategy, which focuses on inorganic growth opportunities, a significant change from the past when the company followed a growth-at-any-cost strategy centered around acquisitions and investments.

Commenting on Uber’s stance on capital allocation, CEO Dara Khosrowshahi said last week that the company is focused on maintaining a capital-lite business model. This strategy is likely to result in strong free cash flow growth as the company scales in the next few years. According to CEO Khosrowshahi, Uber will use most of these incremental cash flows to repurchase shares, reducing the share count.

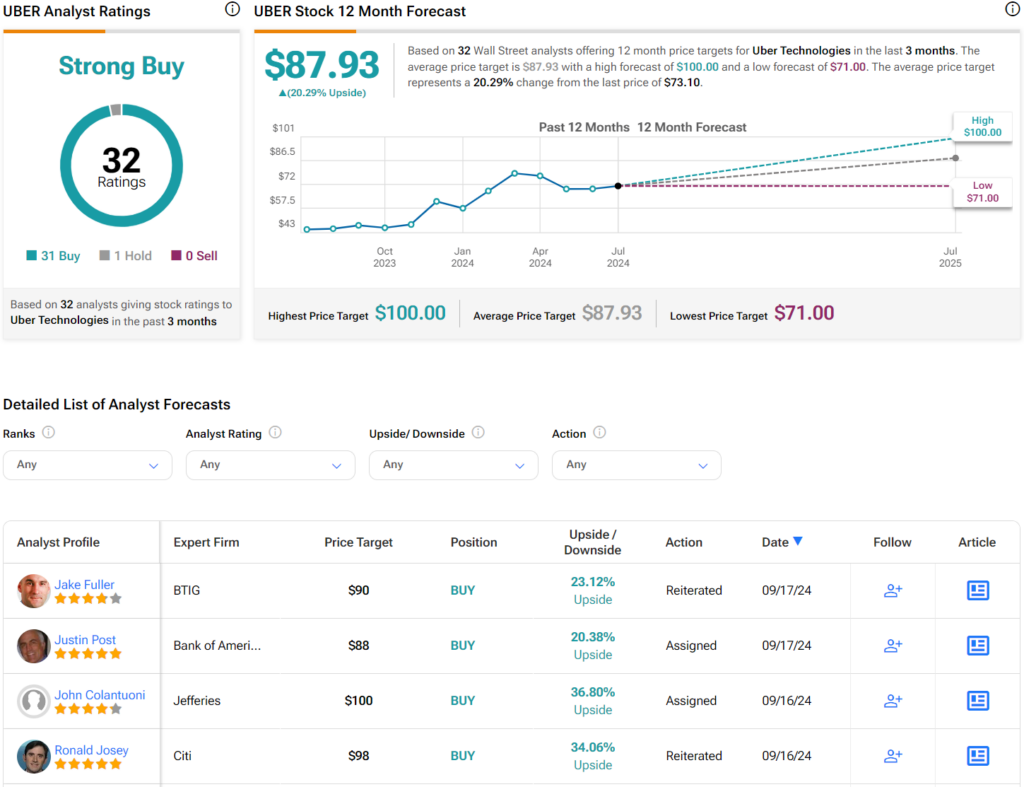

Is Uber a Buy, According to Wall Street Analysts?

Uber stock has appreciated 57% in the past 12 months but still seems attractively valued going by analyst expectations. Based on the ratings of 32 Wall Street analysts, the average Uber price target is $87.93, which implies upside potential of 20.3% from the recent market price.

I believe Uber’s continued investments in expanding the business beyond ridesharing and food delivery, coupled with a focus on repurchasing shares, will help its stock price inch toward the high-end analyst price target of $100 in the coming years.

Takeaway

Uber is well-positioned to benefit from the growth of the autonomous ridesharing industry. The company is strategically expanding into a few other profitable markets as well, including the advertising business. The company is also poised to distribute billions of dollars in incremental capital to shareholders in the long run, potentially helping the company emerge as a large-scale wealth distributor. Given these favorable developments, Uber stock remains an attractive bet despite recent gains.