Hims & Hers Health (HIMS) is trying its best to stay relevant in the multi-billion dollar obesity treatment market. Despite a few setbacks in recent months, its stock has strengthened. The up-and-coming telehealth player offers a direct-to-consumer platform providing access to a wide range of health and wellness products and services.

Claim 55% Off TipRanks

Trade AMZN with leverageHowever, dark clouds are brewing. Market goliath Amazon (AMZN) recently entered the telehealth market, while HIMS is set to lose its grip on one of its most lucrative drugs later this year. So, despite the company’s innovative niche and strong performance to date, I’m leaning bearish on HIMS stock. Both Morgan Stanley and Bank of America expect the stock to underperform over the coming twelve months, rating it as a Hold.

HIMS initially focused on discrete conditions like erectile dysfunction and hair loss. More recently, the company has forayed into weight loss solutions following the advent of drugs like Eli Lilly’s (LLY) Zepbound (tirzepatide) and Novo Nordisk’s (NVO) Wegovy (semaglutide).

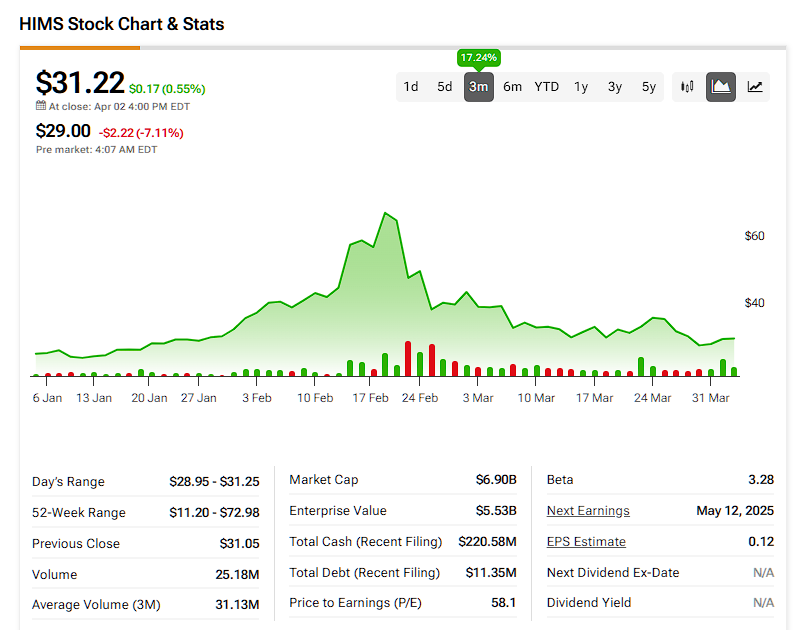

While semaglutide was in short supply throughout 2024, HIMS provided compounded semaglutide, accelerating growth. In recent months, Eli Lilly and Novo Nordisk resolved the shortages, leaving HIMS without compounded semaglutide. Upon closer inspection, the company’s strategy to maintain its grip on the obesity treatment market appears uninspiring. As a result, HIMS’ premium P/E ratio of 58.1 may be unwarranted, given uncertainties surrounding its weight-loss segment — leaving me bearish on HIMS stock.

Can HIMS Cope Without Its $300M Revenue Catalyst?

HIMS introduced compounded semaglutide in May 2024. GLP-1 drugs, like semaglutide, contributed nearly $300 million to the company’s full-year 2024 revenues. Given that the company generated a total of $1.5 billion last year, this implies that GLP-1 drugs comprised 20% of total revenues. This is far from negligible and significant enough to raise concerns among analysts and existing shareholders.

On February 21, the FDA said semaglutide shortages had been resolved, leaving compounders with limited time to stop production. Days later, HIMS revealed its 2025 guidance.

For Q1, HIMS anticipates revenue of ~$530 million, with an adjusted EBITDA margin of ~11.5%. Full-year 2025 revenue is projected to be around $2.35 billion, with adjusted EBITDA margins of ~12.5%. During the earnings call, HIMS management forecasted that its weight-loss segment should contribute at least $725 million to its bottom line.

Weight-Loss Strategy Breakdown

With compounded semaglutide’s exit imminent, HIMS is shifting its attention to another GLP-1 drug, liraglutide. Also known as “Victoza,” liraglutide lost exclusivity in 2024, flooding the market with generic and compounded drugs. Unfortunately for HIMS, liraglutide is an inferior drug to semaglutide in many ways. For starters, patients taking liraglutide tend to lose half the weight as those taking semaglutide. Also, liraglutide is injected daily, whereas semaglutide is injected weekly. That’s 365 needle injections per year compared to 52.

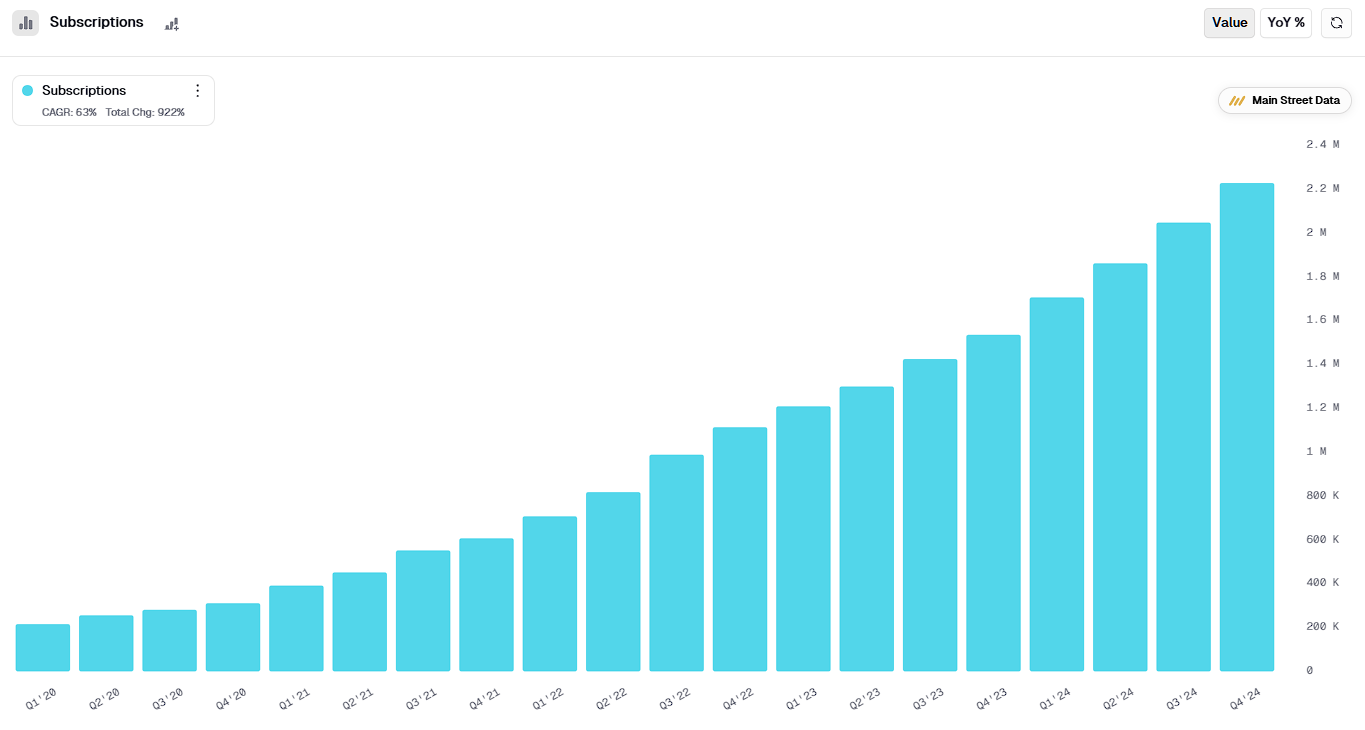

A significant uncertainty is how HIMS’ semaglutide subscribers adjust to the changes. The telehealth pioneer grew its subscriber count from 1,537,000 in 2023 to 2,229,000 in 2024, driven mainly by compounded semaglutide.

On April 1, Hims announced plans to offer branded tirzepatide (Zepbound) on its platform to “expand access.” However, HIMS’ $1,899 per month price on Zepbound (also including medical consultations and ongoing support) is over $1,000 the cost of Zepbound via Eli Lilly’s own pricing through LIllyDirect, where Zepbound is available starting at $349 for self-paying customers. All things considered, it is difficult to envisage HIMS being a go-to spot for weight loss solutions without compounded semaglutide.

Market Risks and Pipeline Opportunities

Fortunately, HIMS is not totally dependent on its weight loss segment. Revenues excluding GLP-1s grew 43% year-over-year to over $1.2 billion last year. Its offerings span many health categories, including skin care, mental health, and supplements. Its brand is appealing and resonates with its target market. Its subscription model provides a reliable source of income. Finally, HIMS is a leader in a large and expanding telehealth sector.

On the flip side, HIMS faces high customer acquisition costs that limit profitability. Its marketing expenses in Q4 were $221 million, representing nearly 50% of revenue. In parallel, the telehealth market is very competitive, and there are now many companies that resemble HIMS like Ro, Keeps, and Roman.

Amazon is the elephant in the room (and now the telehealth market). In November, the online shopping king unveiled “Amazon One Medical,” which is described as a low-cost telehealth service with treatments for common conditions such as men’s hair loss and erectile dysfunction, on-demand messaging visits, and free medication delivery for Prime members.

This makes Amazon a direct competitor to HIMS. While Amazon does not succeed in every venture, a direct B2C telehealth platform has many synergies with its existing business, including delivery and subscriptions. In addition, Amazon has more than 200 million global Prime members and an unmatched ability to advertise to everyone.

Is HIMS Stock a Buy?

On Wall Street, HIMS stock has a consensus rating of Hold based on five Buy, six Hold, and two Sell ratings over the past three months. HIMS’s average price target of $46.50 per share implies approximately 49% upside potential over the next twelve months.

Just yesterday, Craig Hettenbach of Morgan Stanley maintained a Hold rating on HIMS with a price target of $60. He, too, is unconvinced that HIMS’ expanded weight loss offerings will be enough to meet its goals.

Elsewhere on Wall St., Bank of America maintained its Underperform rating, citing revenue generated from Zepbound as “immaterial.” They also expressed concern over the company’s margins, which could fall further given the switch towards selling lower-margin branded drugs through its telehealth platform. Remember that HIMS’ gross margins fell from 83% in Q4 2023 to 77% in Q4 2024 due to its revenue contributions increasingly favoring its weight loss segment.

Pricey Pivots and Amazon Market Entry Cast Doubt on 2025 Growth

In summation, Hims’ post-semaglutide strategy does not stir confidence. Its pivot to an inferior GLP-1 compounded drug and a costly subscription for a branded drug raises questions about its ability to meet lofty expectations in 2025. While HIMS finds success in segments outside of weight loss, the competitive landscape in telehealth is shifting, as evidenced by Amazon’s entry into the space.

While its brand has power, I’m afraid its services lack differentiation and may not compete effectively with others, like Amazon, in terms of price. Given the confluence of factors overshadowing the stock, it is hard to envision HIMS outperforming market expectations for the foreseeable future.