First Solar (NASDAQ:FSLR), the world’s largest thin-film solar module manufacturer, has recently dropped 24% from its all-time high. Prior to this drop, I considered the investment to be overvalued, but following the pullback, I am bullish on it over the next year. Wall Street’s EPS and revenue estimates are very high for the remainder of 2024 and for 2025. Therefore, I think the stock is likely to considerably outperform the S&P 500 (SPX) over the next year.

Claim 30% Off TipRanks

- Unlock hedge fund-level data and powerful investing tools for smarter, sharper decisions

- Discover top-performing stock ideas and upgrade to a portfolio of market leaders with Smart Investor Picks

A Premium Valuation with High Momentum

In my research on First Solar, I noticed that the stock is richly valued at the moment. This is made evident by the fact that the stock’s P/S ratio has expanded from 2.4x as a 10-year median to around 6.9x today. This is warranted because the company has been growing much faster recently compared to historically. For example, First Solar has delivered revenue growth of 26.5% over the last year compared to its 4.3% five-year average.

However, in my opinion, the present high valuation is unlikely to be sustained over a longer-term horizon of five to 10 years. I predict a contraction in its growth rates and, hence, a contraction in its valuation multiples is likely over the next four to five years. This is especially true if Trump is elected to the White House in November because he has much more support for fossil fuels and less emphasis on clean energy than Biden.

Therefore, the opportunity here for First Solar investors is more likely to be significant over one to two years as a momentum investment. The recent 24% pullback in price provides a reasonable entry point for investors who are looking for near-term alpha. With the December 2024 full-year EPS growth estimate at 69.2% and 61.8% for December 2025 on Wall Street, I think 2025 will be a prosperous year for First Solar stock.

Industry Tailwinds Are Currently Driving Growth

Government policies and incentives like the Inflation Reduction Act are providing substantial tax credits and financial benefits for companies involved in renewable energy production. Furthermore, the cost of solar photovoltaic systems has been declining due to technological advancements and economies of scale. Solar energy is now more competitive in terms of price per kWh than fossil fuels.

As a result of the broader market drivers, I think the long-term growth of First Solar is likely, making the current momentum investment even more worthwhile because it is not just hinged on present conditions. However, I think that in the second half of Fiscal 2025, First Solar shareholders may wish to assess the valuation of the company again to see if it is worth holding on to.

In my opinion, it would not be unreasonable if the stock regains approximately 20% in price over the next 12 months. However, I think such a gain would again lead the stock into overvalued territory. If my price target of approximately $275 is met in July 2025, I think the stock would be worth selling because, following this, I expect contractions in valuation multiples and growth rates to potentially introduce downside volatility before the stock becomes more reasonably valued again. Then, more moderate growth may resume at about 10% per annum in price.

The Solar Growth Runway Is Not Linear

Historically, the growth in the solar energy markets has fluctuated from periods of high regional enthusiasm to periods of lower adoption based on a lack of emphasis placed on broader green energy initiatives. For example, tariffs on imported solar panels imposed in 2018 temporarily dampened growth in the U.S. market, which can affect overall sentiment even if First Solar’s panels are still competitively priced.

Furthermore, in the current high interest rate environment, there is less likelihood of borrowing to finance utility-scale solar power plants.

Additionally, the federal debt in the United States is also getting out of control, surpassing $34 trillion recently. I think it is likely in the medium-term future that the United States government will place less emphasis on clean energy. This shift will be driven by geopolitical pressures related to the growing power of China, Russia, and Iran, significantly impacted by the compounding U.S. debt.

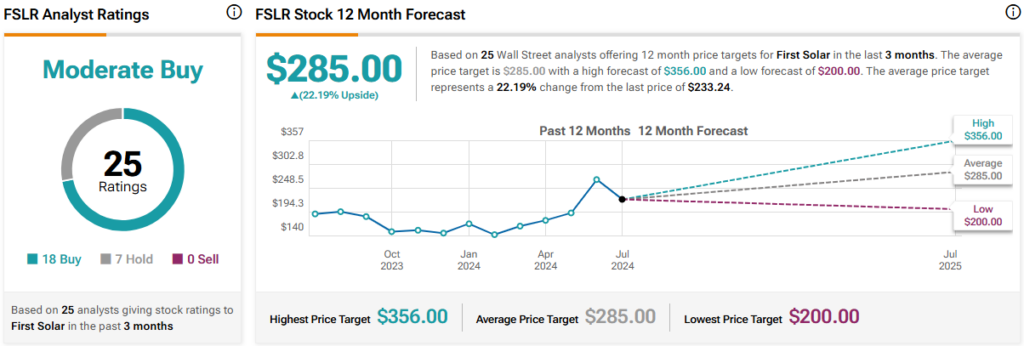

First Solar Is a Buy on Wall Street

Turning to Wall Street, First Solar has a Moderate Buy consensus rating based on 18 Buys, seven Holds and zero Sells assigned in the last three months. At $285.00, the average First Solar price target implies ~22% upside potential.

I think Wall Street is largely accurate here that the next 12 months are likely to see great growth for the stock, and I primarily attribute this to momentum and the near-term results that I outlined above.

Takeaway: First Solar Has Near-Term Alpha Potential

Based on my research and analysis, after the recent 24% pullback in stock price, I think First Solar could deliver outsized returns over the next 12 months. However, following this, I think achieving alpha becomes less certain and believe it is likely the stock will be overvalued by the middle of Fiscal 2025.

Due to the potential for the Trump presidency to also knock U.S. support for solar energy, the core market for First Solar, I think long-term growth expectations should be more moderate than in the near term. However, FSLR is still a Buy, worth owning for at least 12 months, in my opinion.