Exxon Mobil (XOM) opened weaker even after a headline beat. Adjusted earnings came in at $1.88 a share versus $1.82 expected. Revenue landed at $85.3 billion, short of the $86.5 billion consensus.

Claim 30% Off TipRanks

- Unlock hedge fund-level data and powerful investing tools for smarter, sharper decisions

- Discover top-performing stock ideas and upgrade to a portfolio of market leaders with Smart Investor Picks

Profit fell to $7.55 billion from $8.61 billion a year ago as crude prices slid and costs rose. The stock was down about 2% premarket. It is still up 6.6% year to date.

Lower Oil Prices Pressure Margins and Cash

Declining benchmarks continue to bite. Oil futures are down roughly 16% this year, squeezing upstream margins and tempering cash generation. This explains why a clean EPS beat did not translate into a stronger tape.

Management highlighted relative performance against that backdrop. As CEO Darren Woods put it, “We delivered the highest earnings per share we’ve had compared to other quarters in a similar oil-price environment.” Investors, however, are focused on where margins go next if crude stays in the mid-60s.

Exxon Ramps Up Production

Exxon increases barrels while others pull back. Daily production rose to 4.77 million barrels of oil equivalent from 4.58 million last year, ahead of the 4.7 million many on the Street expected.

More barrels help offset weak prices, but they also raise the question of capital discipline if the macro softens further. The long-term plan still targets growth to 2030; near-term returns hinge on price, mix, and refining strength.

Exxon Guidance and Peers Shape the Trade

Exxon frames expectations around steady execution. Investors will watch any color on fourth-quarter run-rates, refining margins, and capital spend if crude drifts toward $60. These inputs will drive the next move in free cash flow and buybacks.

Peers matter too. Chevron’s (CVX) stronger print gives the group a reference point, but dispersion is likely as product cracks, chemicals, and project timing differ by company.

What Could Move the Stock Next

Three things drive the next leg: the path of crude, the pace of cost control, and how much upside refining can still deliver. If oil stabilizes and downstream stays firm, today’s weakness can fade. If prices slip again, the market will demand tighter capex and clearer return targets.

Bottom line, Exxon beat on EPS but the revenue miss and softer profit reminded investors that the macro still calls the tune. Shares can find their footing if cash flow trends improve into year-end; until then, the bias stays cautious

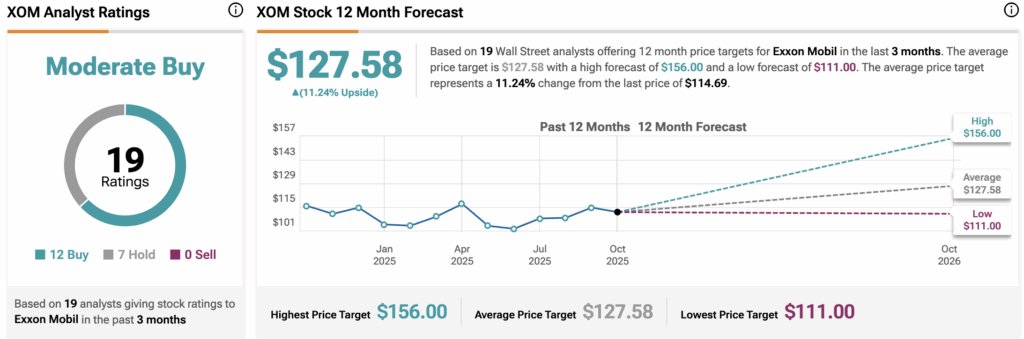

Is Exxon Mobil a Good Stock to Buy?

Wall Street’s consensus rating for XOM stock is a Moderate Buy, with an average analyst price target of $127.58, implying upside potential of 11.2% from current levels.

XOM shares have gained about 9.6% year-to-date.