Bank of America (BAC) is standing at the edge of a transformative moment. A wave of deregulation is about to sweep through the financial sector, promising to loosen the tight capital and compliance rules that have weighed on banks for years.

Claim 55% Off TipRanks

- Unlock hedge fund-level data and powerful investing tools for smarter, sharper decisions

- Discover top-performing stock ideas and upgrade to a portfolio of market leaders with Smart Investor Picks

For BAC, this could mean more cash to lend, fatter investment banking fees, and juicier shareholder returns. While the stock has climbed to new 52-week highs, it is still priced as a value play. Therefore, I’m Bullish on BAC stock.

Unleashing Lending Power Through Deregulation

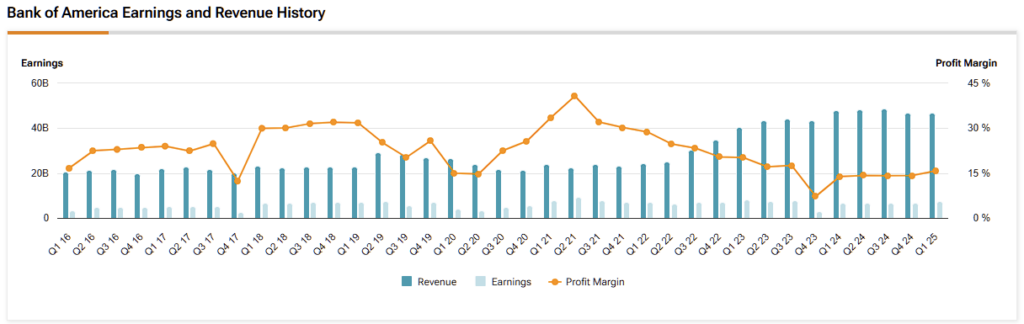

Momentum is building around deregulation, with major banks like Bank of America (BAC) poised to benefit. Potential rollbacks to Basel III capital requirements could unlock billions by lowering reserve thresholds, giving BAC more room to lend. In Q1, the bank reported $14.44 billion in net interest income on its $2 trillion deposit base, and analysts suggest that a looser regulatory environment could increase this figure by 6–7% this year, meaningfully boosting earnings.

At the same time, compliance costs—long a drag on profitability—may finally ease. BAC’s recent removal from a consumer watchdog’s oversight hints at a broader regulatory reprieve. If oversight continues to soften, the bank could not only lower expenses but also redirect capital toward growth areas like small business loans and mortgages.

Capital Markets Ready to Roar

Bank of America’s investment banking and trading divisions stand to gain significantly from a potential wave of deregulation. Looser rules tend to drive M&A activity, IPOs, and market volatility—ideal conditions for BAC’s Global Markets unit. In Q1, equities trading revenue surged 17% to a record $2.2 billion, and fixed income climbed 5% to $3.5 billion, as Main Street Data shows.

While investment banking fees dipped 3% to $1.5 billion, reflecting a broader slowdown in U.S. M&A, CEO Alastair Borthwick pointed to a strengthening deal pipeline. A more business-friendly climate under the Trump administration could accelerate this recovery.

Meanwhile, the ongoing market resilience, even amid geopolitical tensions, signals investor optimism regarding pro-growth policies.

For BAC, that translates into more opportunities to capitalize on volatility. Should deregulation spark renewed corporate deal flow—or support BAC’s push into digital assets, such as its proposed USD-backed stablecoin—the bank could unlock new revenue streams and deepen its market advantage.

Shareholder Returns Set to Shine

Deregulation could be a goldmine for BAC’s shareholders as well. With less capital tied up, BAC can ramp up buybacks and dividends. In Q1, earnings rose 11% to $7.4 billion, backed by a robust Common Equity Tier 1 ratio of 11.8%, well above the 10.7% minimum. This gives BAC plenty of room to return capital if these ratio requirements go down.

Today, it has a $0.26 quarterly dividend yield of 2.25%, which the company has grown for 11 straight years, with 16 years of dividend growth to boot, according to TipRanks data.

Meanwhile, projected buybacks for the year reach $18 billion, screaming confidence. In fact, BAC trades at a buyback yield of 4.3% on recent repurchases, which, along with the dividend, form a blended yield of 6.5%. Not bad for a company expected to see notable growth in the near term. In the meantime, the payout ratio stands at just 28.4% this year’s consensus EPS estimate of $3.66, so an acceleration in the rate of dividend hikes is indeed possible.

A Bargain Hiding in Plain Sight

At today’s share price, BAC stock is trading at its 52-week highs, but in my view, it’s still a steal. Consensus EPS estimates project 14% growth to $3.66 in 2025, followed by an acceleration to 17% growth to $4.25 in 2026.

Yet, BAC trades at just 12.7x 2025 EPS, which is significantly below that of some of its competitors. For context, JPMorgan’s (JPM) 15x and Wells Fargo’s 13.5x multiples are higher, despite BAC outpacing their growth forecasts.

Tariff fears and potential rate cuts (which could possibly shave $3.3 billion off net interest income if rates drop 100 basis points) could spook investors. However, BAC’s strong wealth management inflows and trading gains suggest that the impact may not be as harsh on a consolidated basis.

What is the Price Target for Bank of America?

Wall Street’s stance on Bank of America stock is quite bullish. As things stand, BAC carries a Strong Buy consensus based on 18 Buy and two Hold ratings in the past three months. BAC’s average 12-month price target of $49.50 implies a potential upside of approximately 6%, suggesting that many analysts believe the stock could continue to rise despite trading just below 52-week highs.

Deregulation Tailwinds Could Power Next Leg of BAC Growth

Bank of America is approaching a pivotal moment, with potential deregulation poised to unlock fresh growth opportunities. Positioned to boost lending, energize its capital markets division, and enhance shareholder returns, BAC looks compelling—especially at just 12.7x earnings and with EPS expected to rise 14–17% in the near term.

While macroeconomic risks, such as trade tensions and interest rate shifts, remain, the bank’s strong balance sheet and diversified operations provide a solid foundation for continued performance and investor upside.