DBS Group (DBSDF) expects its earnings to surpass S$10 billion ($7.4 billion) in the ensuing three to five years, as opposed to S$8.2 billion in 2022. The company’s solid financial position and initiatives to improve its technological skills may help it reach its profit goal.

Claim 30% Off TipRanks

- Unlock hedge fund-level data and powerful investing tools for smarter, sharper decisions

- Discover top-performing stock ideas and upgrade to a portfolio of market leaders with Smart Investor Picks

In its recently held Investor Day, the Singapore-based bank also revealed its target return on equity range of 15% to 17%. DBS also hinted at the potential for an increase in dividends or share buybacks.

Growth Drivers

The corporation anticipates accelerating growth in its Treasury Market division and Wealth Management section, along with higher sales for its global transaction services. According to DBS, these enterprises have the potential for substantial returns while requiring less capital.

Further, the company continues to be bullish about the advantages of digitalization despite recent setbacks in the form of interruptions in digital banking.

The company also sees growth potential in Taiwan, Indonesia, and India, notably in the areas of transaction banking, wealth management, small business financing, and unsecured retail lending.

Will DBS Shares Go Up?

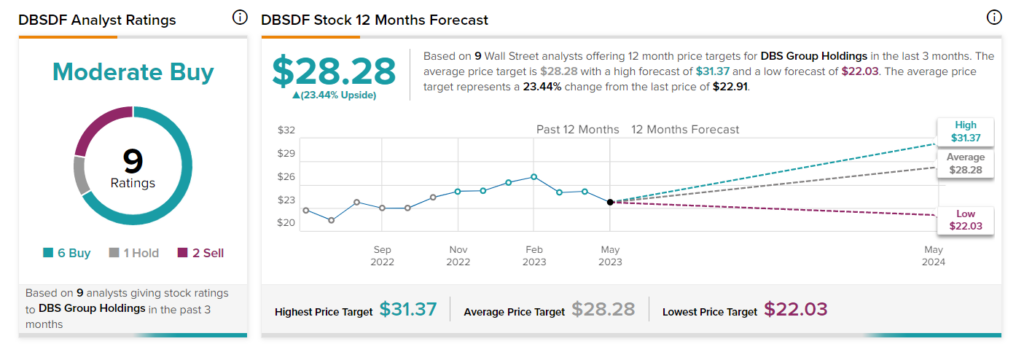

On TipRanks, the stock’s average analyst price target of $28.28 implies upside potential of 23.4% from the current level. Overall, DBS has a Moderate Buy consensus rating based on six Buy, one Hold, and two Sell ratings assigned in the past three months.