Costco stock (NASDAQ:COST) presents a fascinating anomaly in the stock market. While undeniably overvalued, it enjoys a cult-like following, with investors willing to pay insane valuation multiples for a piece of the company. Consequently, shorting the stock is risky, even as its current price levels appear unjustifiable. In my view, therefore, prospective investors should pay close attention to Costco’s results and consider buying only after a substantial price drop. For now, I remain neutral on COST stock.

Claim 30% Off TipRanks

- Unlock hedge fund-level data and powerful investing tools for smarter, sharper decisions

- Discover top-performing stock ideas and upgrade to a portfolio of market leaders with Smart Investor Picks

Costco’s Cult-Like Following Drives a Cult-Like Valuation

Costco is known for having a cult-like following, which, in turn, drives a cult-like valuation. There are other cases in the market that attract investors willing to pay exorbitant multiples for a stake in the company. A prominent, albeit controversial, example is Tesla (NASDAQ:TSLA), where investors prioritize factors beyond traditional valuation metrics when assessing its investment case.

In any case, as shown in the chart above, COST stock has run up by nearly 67% over the past year, sustaining an impressive rally despite a comparatively modest rise in the company’s revenues or earnings, as we’ll soon discuss. Therefore, the stock’s valuation has expanded to extreme levels far exceeding those of its industry peers. For context, here is Costco’s current forward P/E ratio in comparison to other prominent retailers in descending order:

- Costco: 50.4

- Walmart (NYSE:WMT): 27.4

- BJ’s Wholesale Club (NYSE:BJ): 22.3

- Dollar General (NYSE:DG): 17.0

- Dollar Tree (NASDAQ:DLTR): 15.4

- Target Corporation (NYSE:TGT): 14.8

Clearly, Costco’s stock is outrageously more expensive than its peers. Interestingly, this has been a typical theme. In fact, over the past decade, Costco has never traded at a lower valuation than any of its industry counterparts. Then again, the valuation gap between Costco and its peers has never been wider. It’s like the market expects Costco’s growth to undergo a massive acceleration. However, this is likely not the case. Costco should keep expanding at a decent pace, yet not at one that implies growth rates over 20%.

Assessing Costco’s Growth Prospects

To assess Costco’s ongoing growth and whether it justifies its current valuation, let’s examine its past growth metrics, current growth, and future growth prospects. Regarding its past growth, the company’s revenues and earnings per share (EPS) have grown at compound annual growth rates (CAGR) of 8.7% and 11.8% over the past decade, respectively.

Shifting gears to Costco’s current growth, the company has managed to sustain similar rates lately. Net sales for the third fiscal quarter of Fiscal 2024 rose by 9.1%, while EPS grew by roughly 29% to $3.78. This growth was again driven by higher comparable sales, higher e-commerce sales, and a larger number of running locations. More specifically, total same-store sales for the period grew by 5.3%, e-commerce sales grew by 14.9%, and an additional 24 net new warehouses opened since the end of Fiscal Q3 of 2023.

The rather significant EPS gains may imply a potential acceleration in EPS, as I mentioned earlier. Yet, this is not the case. Costco enjoyed some margin tailwinds in the quarter, but for the full year, Wall Street expects EPS growth of 14% to $16.16. Finally, looking ahead, consensus estimates forecast that EPS over the next five years will grow at a CAGR of 9%. Clearly, these growth projections mirror current trends and do not indicate the multi-year acceleration that Costco’s current stock price appears to price in.

When Should You Consider Buying Costco Stock?

Determining the right time to buy Costco stock is hard. Six months ago, I would have suggested staying on the sidelines, as the shares seemed quite pricey. However, I would have been mistaken, as the market later drove the stock to even higher levels.

Naturally, as Costco stock has become even more expensive, I am now even further inclined to suggest avoiding investing at the current levels. Yet, I could again be wrong. Regardless, if you are one of those willing to pay a hefty price for this company, waiting for a potential dip might be worth it.

Is COST Stock a Buy, According to Analysts?

Checking Wall Street’s view on the stock, Costco Wholesale maintains a Strong Buy consensus rating based on 19 Buys and one six Hold recommendations assigned in the past three months, despite its already excessive gains. At $855.61, the average COST stock forecast implies a 0.9% downside potential, nonetheless.

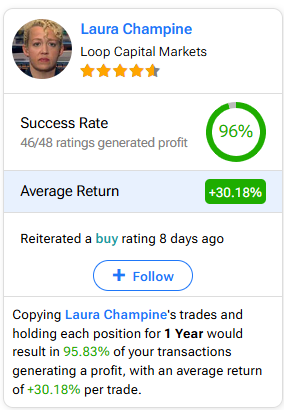

If you’re wondering which analyst you should follow if you want to buy and sell COST stock, the most accurate analyst covering the stock (on a one-year timeframe) is Laura Champine from Loop Capital Markets, with an average return of 30.2% per rating and a 96% success rate. Click on the image below to learn more.

The Takeaway

Overall, despite Costco’s impressive performance, its current stock price seems excessively high relative to its peers. Further, while the company’s growth is likely to be sustained at relatively strong levels, it can’t possibly justify the stock’s current valuation. Therefore, investors should exercise caution. Watching the company’s results closely and waiting for a significant price drop might provide a more favorable entry point, although such instances have been somewhat rare.