Cisco Systems’ (CSCO) dividend growth has gradually decelerated in recent years. While the networking and technology infrastructure leader has consistently hiked its dividend every year since initiating payouts in 2011, the rate of these increases has become increasingly modest. However, with the company likely to announce another dividend hike next quarter, there is a case to make that this trend could be reversing. Strong earnings and a favorable business environment may enable a more substantial raise this time around, boosting investor interest in the stock. Accordingly, I am bullish on Cisco Systems.

Claim 30% Off TipRanks

- Unlock hedge fund-level data and powerful investing tools for smarter, sharper decisions

- Discover top-performing stock ideas and upgrade to a portfolio of market leaders with Smart Investor Picks

Cisco Set to Boost Dividend Growth

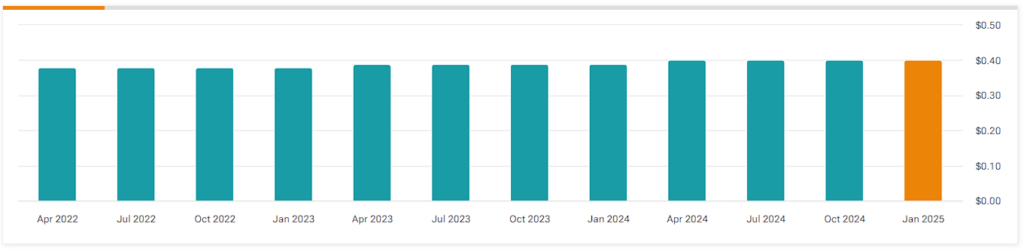

Just in case you’re unfamiliar with Cisco Systems’ dividend history or could use a quick refresher, the company has consistently shown its commitment to returning value to shareholders since initiating dividend payments in 2011. The company now counts 13 consecutive years of annual dividend hikes, backed by its mission-critical business model, which supports stable revenue and earnings growth over time.

However, recent dividend increases have notably decelerated. Since 2019, Cisco has been increasing its dividend by just a cent per quarter year over year. Last year’s dividend hike, which raised the quarterly dividend from $0.39 to $0.40 per share, represented a mere 2.6% increase—the slowest in its history. Dividend growth investors, therefore, may have been disappointed, as these increases have barely outpaced inflation. Nonetheless, I believe that the upcoming quarter could mark a change in this trend, with the potential for a more significant dividend increase.

Q1 Results Could Sustain Heftier Dividend Increases

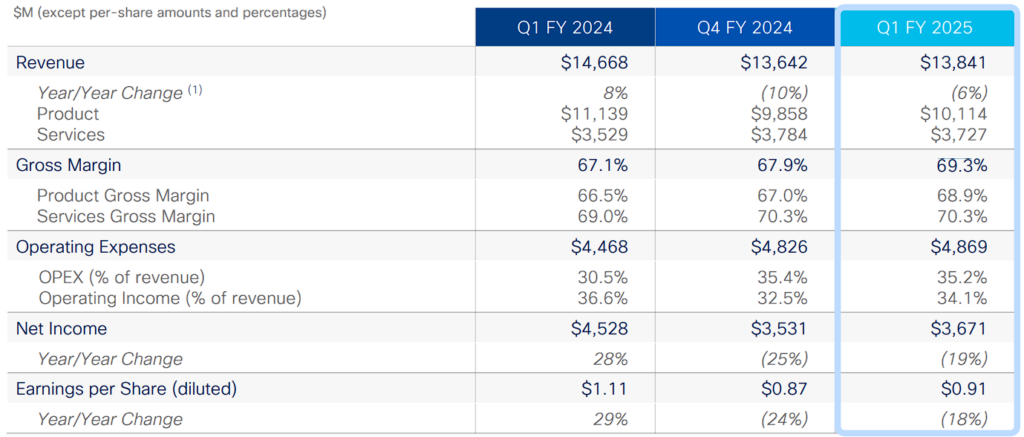

Examining Cisco’s recent performance, I think it becomes easy to see that the company is well-positioned to reignite its dividend growth momentum. Its Fiscal Q1 results were uplifting, with revenues hitting $13.8 billion—at the high end of Cisco’s guidance range. There were some noteworthy highlights. For instance, product orders increased 20% year-over-year, including a 9% gain when excluding Splunk’s contributions, indicating robust demand levels for Cisco’s products and solutions. Further, Cisco achieved adjusted EPS of $0.91, exceeding expectations and demonstrating operational efficiency. This was partly thanks to a favorable product mix, leading to an adjusted gross margin of 69.3%—the highest in over two decades!

More specifically, the company has seen strong demand in key segments, like security and observability, which benefited from Splunk’s integration. In fact, security orders doubled year-over-year, powered by Cisco turning its focus on advanced threat intelligence and new product offerings like XDR and Secure Access.

In addition, I liked how the rest of Cisco’s networking portfolio displayed encouraging signs of growth, with consecutive quarters of double-digit order increases in data center switching. I think that these developments seem to validate Cisco’s strength in capitalizing on the rising demand for AI infrastructure and enterprise networking we are observing these days. This trend suggests that the company shouldn’t struggle to deliver solid earnings growth going forward.

Earnings Growth Poised to Support Bigger Dividends

Speaking of earnings growth, Cisco Systems is set to deliver another year of near-record earnings. The company projects adjusted EPS of $3.60 to $3.66 for Fiscal 2025—not far from Fiscal 2024’s $3.73 and Fiscal 2023’s record $3.89. I should note that earnings over the past couple of years were boosted by a backlog of delayed orders, mainly due to supply chain disruptions and pent-up customer demand during the pandemic, which artificially inflated results. That’s why Cisco’s guidance is still impressive, especially considering the normalization of demand and the absence of a similar backlog effect.

In any case, Cisco’s payout ratio hovers at about 44% around the midpoint of management’s guidance, indicating ample room for management to pursue more aggressive dividend increases. Historically, Cisco has been committed to maintaining a competitive dividend yield, so I believe this will likely motivate the company to shift away from single-cent dividend hikes in favor of more substantial hikes. From another perspective, with Cisco’s shares trading at just about 16 times this year’s expected EPS—notably below its tech sector peers—a more substantial dividend increase this year could reignite investor interest in the stock and expand its valuation multiple.

Is CSCO Stock a Buy?

Wall Street analysts seem somewhat bullish on Cisco Systems’ outlook following the stock’s recent rally. Specifically, CSCO stock features a Moderate Buy, with recent analyst ratings consisting of seven Buys and seven Hold ratings over the past three months. At $63.07, the average CSCO stock price target implies an upside potential of 7.4% from its current levels.

For the best guidance on buying and selling CSCO stock, look to George Notter. He is the most profitable analyst covering the stock (on a one-year timeframe), boasting an average return of 12.9% per rating and an outstanding 66% success rate.

Summing up

In summary, Cisco’s recent performance and strong earnings outlook suggest it may be ready to reverse the trend of modest dividend increases. With solid demand, growth across key segments, and a healthy payout ratio to support higher payouts, Cisco appears well-positioned for a more substantial dividend hike in the upcoming quarter. I believe that such a move could rejuvenate investor interest and potentially boost its valuation, making CSCO an attractive pick for dividend-growth investors today.