Earlier today, the Canadian Imperial Bank of Commerce (TSE:CM) (NYSE:CM), also known as CIBC, reported its Fiscal Q1-2023 financial results, which beat both revenue and earnings-per-share (EPS) expectations. As a result, the stock finished 2.7% higher despite the overall market finishing lower.

Claim 55% Off TipRanks

- Unlock hedge fund-level data and powerful investing tools for smarter, sharper decisions

- Discover top-performing stock ideas and upgrade to a portfolio of market leaders with Smart Investor Picks

In Q1, CIBC’s revenue rose 8% to C$5.93 billion compared to the consensus estimate of about C$5.71 billion. Also, adjusted earnings per share were C$1.94, beating the C$1.71 consensus estimate but down from the C$2.04 per share recorded in the same period last year.

Further, CIBC’s adjusted return on equity fell to 15.5% from 17.6% last year, and its CET1 ratio (a liquidity ratio — a higher percentage indicates more liquidity) fell by 10 basis points year-over-year to 11.6%.

Now, let’s look at the bank’s individual segments. Its Canadian Personal and Business Banking segment saw some headwinds, with net income falling 14% year-over-year to C$589 million, mostly because of “higher non-interest expenses and a higher provision for credit losses, partially offset by higher revenue.” Also, U.S. Commercial Banking and Wealth Management saw a similar drop in profitability. In contrast, CIBC’s Canadian Commercial Banking and Wealth Management experienced a net income increase of 2% to C$469 million.

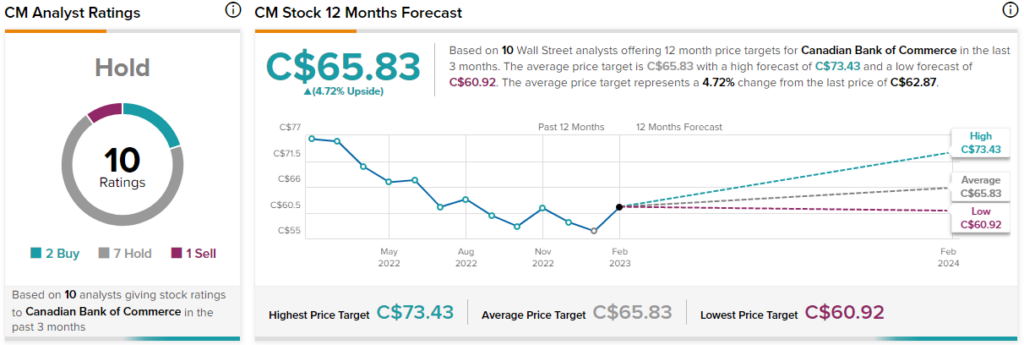

Is CM Stock a Buy, According to Analysts?

According to analysts, CM stock comes in as a Hold based on two Buys, seven Hold ratings, and one Sell given in the past three months. The average CM stock price target of C$65.83 implies 4.7% upside potential.