Chewy (NYSE:CHWY) reported better-than-expected fourth-quarter results. However, CHWY stock declined 2.5% in Wednesday’s extended trading session. The drop stems from the company’s lower-than-expected Q1 revenue forecast. Additionally, the company expects its 2024 active customer base to stay flat due to inflationary pressures and subdued pet ownership trends. This irked investors.

Claim 30% Off TipRanks

- Unlock hedge fund-level data and powerful investing tools for smarter, sharper decisions

- Discover top-performing stock ideas and upgrade to a portfolio of market leaders with Smart Investor Picks

Chewy operates an online platform for pet food, supplies, medications, and other pet health products and services.

Q4 Earnings Highlight

The company reported EPS of $0.07, exceeding analysts’ expectations of a loss of $0.04. Its adjusted EPS stood at $0.18 per share, up from the prior-year quarter’s EPS of $0.16. Moreover, it surpassed analysts’ estimates by $0.09.

Chewy’s revenue increased 4.2% year over year to $2.83 billion, surpassing the consensus estimates of $2.79 billion. The year-over-year growth was driven by solid demand for Chewy’s health and non-discretionary consumable products. During the quarter, net sales per active customer (NSPAC) increased by 11.9% to $555.

Q1 and Fiscal 2024 Outlook

CHWY expects its Q1 revenue to be between $2.84 billion and $2.86 billion, up about 2% year over year. However, it fell short of analysts’ expectations of $2.89 billion.

Furthermore, the company projects Fiscal 2024 revenue between $11.6 billion and $11.8 billion, compared with the Street’s estimates of $11.7 billion. The guidance reflects 4% to 6% growth year-over-year.

Analyst Remains Optimistic

Following the release of Q4 results, Goldman Sachs analyst Alexandra Steiger reiterated a Buy rating on Chewy stock but lowered the price target to $32 (80.4% upside potential) from $36.

The analyst is bullish about CHWY’s long-term prospects and expects it to benefit from international expansion, ad revenue opportunities, and strong momentum in the Chewy Health unit.

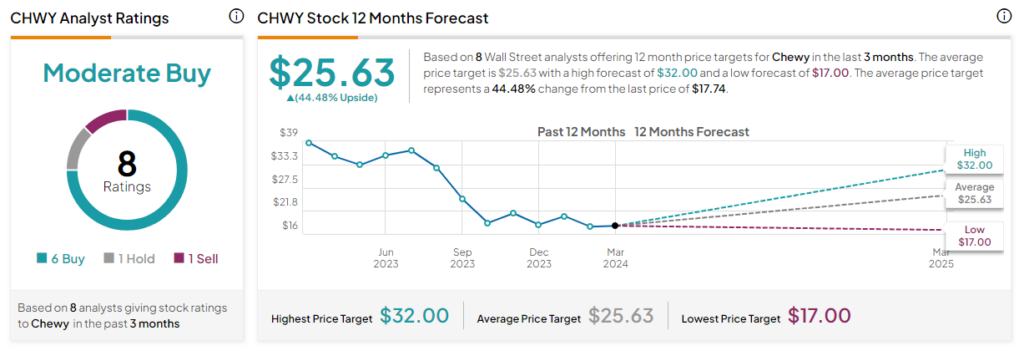

Is Chewy a Buy, Sell, or Hold?

Chewy has a Moderate Buy consensus rating based on six Buy, one Hold, and one Sell ratings. The analysts’ average price target on CHWY stock of $25.63 implies a 44.48% upside potential. Shares of the company have declined by about 29% in the past three months.