Camping World (CWH), the nation’s leading seller of RVs and related products, delivered impressive results in its recent Q3 report, outperforming top-and-bottom-line expectations. Fueled by robust new vehicle sales, the company is well-positioned for continued growth into 2025. The recent proposal to offer $300 million of Class A common stock promises to further strengthen the company’s financials. The stock is up over 38% year-to-date, and analysts’ projections point to a favorable outlook, making the stock a solid option for investors looking to participate in the RV market’s turnaround.

Claim 55% Off TipRanks

- Unlock hedge fund-level data and powerful investing tools for smarter, sharper decisions

- Discover top-performing stock ideas and upgrade to a portfolio of market leaders with Smart Investor Picks

Camping World Returns to Positive Revenue Growth

Camping World is the leading provider of RVs and related products and services in the United States. It offers products under the Camping World and Good Sam brands while operating in two segments: Good Sam Services & Plans and RV & Outdoor Retail.

Recently, the company returned to positive revenue growth in its combined new and used same-store unit sales for the first time in ten quarters. This was primarily credited to its strategic focus on product development and affordability. Moreover, it recorded a double-digit growth rate in new units, leading to significant momentum for its 2025 plan.

In the latest news, Camping World announced an offering of $300 million of its Class A common stock, granting the underwriters a 30-day option to purchase up to an additional $45 million. The proceeds from this offering will be used for general corporate purposes, such as enhancing their balance sheet, augmenting working capital, and reducing debt.

Camping World’s Recent Financial Results

The company recently reported its results for Q3 2024, and the driving narrative for the quarter was the confounding nature of sales. Like Two-Face flipping a coin, it appeared to be of two minds. New vehicle revenue significantly rose by $145.7 million or 21.5% despite the average selling price of these vehicles seeing a 7.4% decrease. Yet, used vehicle revenue dropped by $143.0 million, or 24.2%, with a decline in average selling price by 7.7%. Overall, gross profit declined due to lower average selling prices of new and used vehicles, albeit partially offset by lower average costs and a nonrecurring $5.5 million exit arrangement with a service partner.

Overall, revenue was $1.7 billion, beating analysts’ estimates by $60 million. However, gross profit ($498.5 million) and total gross margin (28.9%) decreased year-over-year by $24.6 million (or 4.7%) and 134 basis points, respectively. Non-GAAP earnings per share (EPS) of $0.13 surpassed consensus expectations by $0.04.

The company announced a regular cash dividend of $0.125 per share for the quarter, a dividend equivalent yield of 2.33%, which it paid on September 25, 2024.

Is CWH a Buy?

It has been a rough period for the RV market, translating into a volatile ride for the stock (beta of 1.99). The shares are down 28.29% over the past three years. It trades near the middle of its 52-week price range of $16.18 – $28.72 and shows positive price momentum as it trades above the 20-day (22.42) and 50-day (22.40) moving averages. With a P/S ratio of 0.28x, it is at a slight discount to the Auto & Truck Dealerships industry with an average P/S ratio of 0.48x.

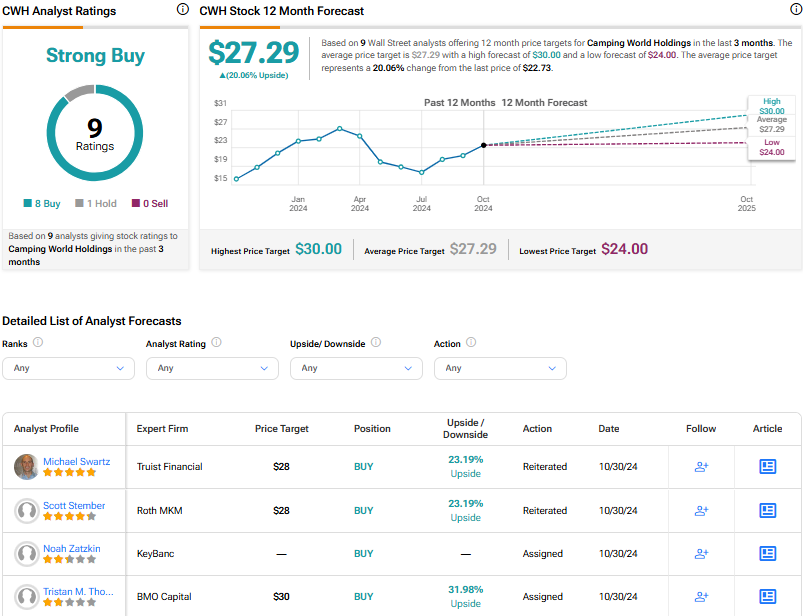

Analysts following the company have been bullish on CWH stock. Based on the most recent recommendations of nine analysts, Camping World Holdings is rated a Strong Buy overall. The average price target for CWH stock is $27.29, representing a potential upside of 20.06% from current levels.

Closing Thoughts on Camping World

Camping World surprised investors in Q3 with substantial new vehicle sales. The company looks to keep the momentum going, with the recent proposition offering $300 million in stock to bolster its financial position. Analysts remain bullish on the stock, making it a compelling choice for investors looking to capitalize on the RV market’s revival.