Boeing’s (NYSE:BA) troubles with its 737 airliner program are by this point in time well-known. From high profile crashes to even higher-profile planes falling apart midair, Boeing’s reputation has been well and truly pummeled in recent years. But… it’s always darkest before the dawn, right?

Claim 30% Off TipRanks

- Unlock hedge fund-level data and powerful investing tools for smarter, sharper decisions

- Discover top-performing stock ideas and upgrade to a portfolio of market leaders with Smart Investor Picks

That’s what Deutsche Bank analyst Scott Deuschle seems to think at least. In a hopeful note, posing the rhetorical question “What happens when accelerating deliveries meet beaten up estimates?”, Deuschle observes that as recently as May 13, Boeing had only delivered four of its 737 airliners in the month of May, but as of Thursday, that number has doubled to eight, putting Boeing on pace to deliver perhaps 16 airplanes this month if things keep going as well as they have been going.

And that might actually happen.

Citing arcane “aircraft age data” from the Cirium aviation analytics database, Deuschle observes that the eight planes Boeing has delivered so far this month all appear to be “recently manufactured aircraft.” From this he seems to surmise that Boeing has cleared out its backlog of airplanes already-built, and is now producing airplanes as fast as customers can take them. And if that’s the case, then it means that the 25 planes Boeing delivered in April (one fewer than in April 2023) made that Boeing’s “trough” month. From here on out, we may see an acceleration in production and deliveries of Boeing planes – and an acceleration in cash flowing into Boeing.

Speaking of cash, Deuschle next turns the conversation to Boeing’s free cash flow. Other analysts, notes this analyst, believe Boeing will generate only $1.3 billion in cash profit this year – but that guess is looking “increasingly beaten up” based on the rate at which Boeing is now delivering planes. Next year, Wall Street thinks Boeing will grow its FCF number to $5.8 billion, but Deuschle is more optimistic, predicting FCF will grow to $6.5 billion as Boeing deliveries increasing quantities of 737 airplanes, and 767s, 777s, and 787s as well.

Now, it’s not all good news for Boeing. Last year, the planemaker delivered 528 total airplanes, of which 396 – fully 75% – were 737s. So far this year, Boeing has delivered only 118 planes total. Run-rate that number out over the rest of this year, and if Deuschle is wrong about the rate of acceleration, then Boeing could end up delivering just 300 or so airplanes this year, a steep come-down from 2023.

On the other hand, if he’s right, if Boeing keeps accelerating production, and ends up generating his hoped-for $6.5 billion in FCF next year, then Boeing stock is currently selling for only about 17x forward free cash flow. With Boeing stock expected to nearly double its FCF number from 2025 through 2027, that seems like an attractive multiple.

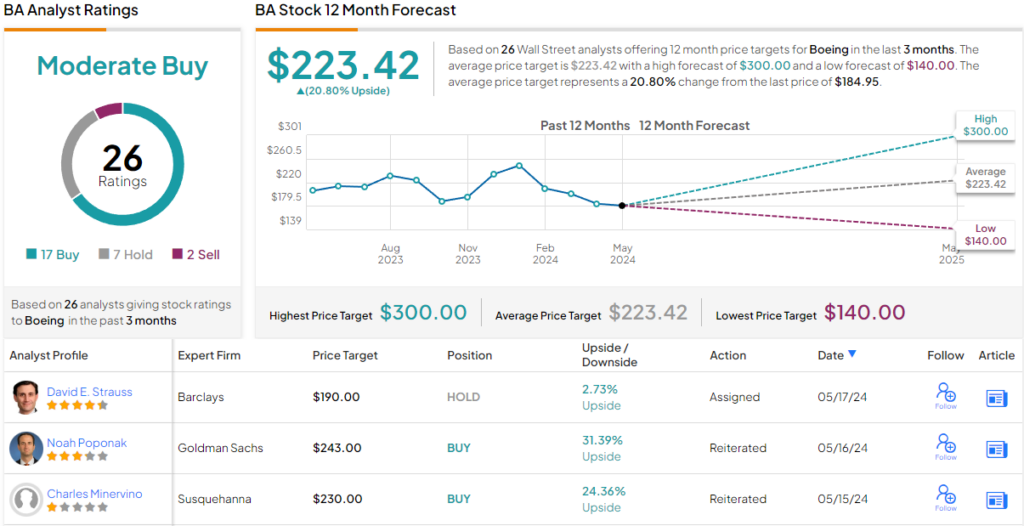

Attractive enough, in fact, that Deuschle values Boeing stock at $225 (about 22% upside from current levels), and he rates the stock a buy. (To watch Deuschle’s track record, click here)

Deuschle objective appears to be in line with the rest of the Street; the average target stands at $223.42, making room for one-year returns of ~21%. Boeing Moderate Buy consensus rating is based on a mix of 17 Buys, 7 Holds and 2 Sells. (See Boeing Stock forecast)

To find good ideas for stocks trading at attractive valuations, visit TipRanks’ Best Stocks to Buy, a tool that unites all of TipRanks’ equity insights.

Disclaimer: The opinions expressed in this article are solely those of the featured analysts. The content is intended to be used for informational purposes only. It is very important to do your own analysis before making any investment.