Monetary policy has significantly influenced market sentiment toward the gold-mining enterprise Barrick Gold (GOLD). Recently, a signal of the Federal Reserve’s potential strategy pivot has sent sentiment for the underlying shining metal moving higher (notwithstanding Friday’s soft session). With Barrick also enjoying a very attractive valuation, I am bullish on GOLD stock and its capability of acting as a precious metal proxy.

Claim 30% Off TipRanks

- Unlock hedge fund-level data and powerful investing tools for smarter, sharper decisions

- Discover top-performing stock ideas and upgrade to a portfolio of market leaders with Smart Investor Picks

The Financial Framework Favors GOLD Stock

Before diving into the fundamental argument for GOLD stock, it’s helpful to consider the financial rationale. Right now, shares trade hands at 2.83x trailing-year sales. That’s a modest premium compared to the price-to-sales ratio recorded in the first quarter of 2023 and Q1 2024, which was 2.71x.

Also, the company’s projected earnings multiple is 16.08x, up from 18.08x in the past year. In other words, the market has no problem supporting GOLD stock at or near its current earnings and sales premiums.

Even better, the gold market runs an average revenue multiple of 3.16x. So, even with the modest bump up to 2.83x, GOLD stock is technically undervalued. The case becomes even more favorable when looking at the earnings multiple for the sector, which stands at 41.65x. Whether you look at Barrick’s forward multiple or trailing multiple (which happens to be 22.59x), the assessment is the same: it’s a discount.

Further, this prospect could become even more enticing when considering analysts’ projections. By the end of Fiscal 2024, Barrick could post earnings per share of $1.14. That would come out to a nearly 36% increase over last year’s print of 84 cents. The following year, EPS could hit $1.48, a rise of almost 30% from projected 2024 earnings.

On the top line, Wall Street’s experts target sales of $12.91 billion. If so, that would imply a 13.3% lift from last year’s tally of $11.4 billion. By Fiscal 2025, the top line may expand to $14.57 billion, up 12.9% from projected 2024 revenue.

Generally, the forecasts seem reasonable based on recent historical figures. Barrick posted an average EPS of 22 cents in the past four quarters. This figure beat the consensus view of 19 cents, thus yielding an average earnings surprise of 18.25%.

Admittedly, the revenue picture is a bit trickier. In the past, Barrick hasn’t always hit its sales mark. However, keep in mind that if Barrick’s Fiscal 2024 sales fall to the low-end estimate of $10.78 billion, its revenue multiple would be 3.02x (assuming a shares outstanding count of 1.76 billion). That’s still lower than the sector average, giving GOLD stock a safety cushion.

Fundamentals Could Really Swing Barrick Gold Higher

While the valuation of GOLD stock provides much comfort for investors, they might not need it. The fundamentals could provide a significant catalyst for the enterprise.

Let’s consider the basic context. Barrick Gold is one of the biggest gold miners in the world. This is not a speculative play where it may find some gold or not. It produces a boatload of yellow metal and, relatively speaking, enjoys an established and predictable operating protocol. Therefore, it’s one of the best proxies of the precious metal.

Generally speaking, whatever is good for gold is good for GOLD stock. Currently, one of the driving forces of key commodities is inflation. That narrative took a hit last month when Fed Chair Jerome Powell “highlighted the challenges the central bank faces in balancing economic growth with price stability,” according to TipRanks’ Paul Hoffman.

However, the fundamentals could be back on again for GOLD stock. Powell’s comments have suggested that a policy pivot may be on the way. Per TipRanks’ Amit Singh, the central bank chief stated that significant progress has been made in the battle against inflation. Powell didn’t state directly when rate cuts might materialize. However, investors have speculated on this development, leading to a rise in risk-on assets.

Essentially, lower borrowing costs imply dollar devaluation. Naturally, “inflation-friendly” assets such as precious metals shot higher. In the business week ending July 12, GOLD stock gained over 7% of equity value.

Barrick is attractive compared to purely speculative ideas because GOLD stock is undervalued against the combination of sector averages and analysts’ targets. Plus, investors can enjoy the benefit of hanging out. GOLD stock has a dividend yield of 2.22%.

Financially undervalued and supportive fundamentals? That sounds like a good deal.

Is Barrick Gold Stock a Buy, According to Analysts?

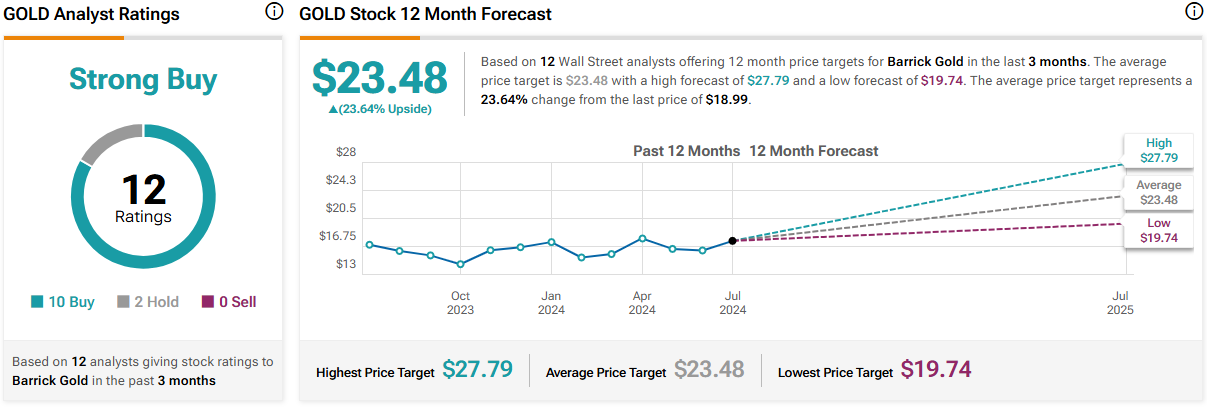

Turning to Wall Street, GOLD stock has a Strong Buy consensus rating based on 10 Buys, two Holds, and zero Sell ratings. The average GOLD stock price target is $23.48, implying 23.6% upside potential.

The Takeaway: GOLD Stock Offers a Compelling Proxy Play

Without any other fundamental context, Barrick Gold already appears undervalued relative to the combination of analysts’ projections and the average premiums associated with the gold sector. Additionally, in the broader context of a potential monetary policy pivot, GOLD stock appears even more enticing as a proxy play for the underlying commodity.