UK-based Aston Martin Global Holdings PLC (GB:AML) has signalled that it expects lower profits for FY24 due to supply chain disruptions and a decline in sales in China. According to its trading update, the company now expects its adjusted EBITDA (earnings before interest, tax, depreciation, and amortization) to be slightly below FY23 levels. In addition, it no longer expects to achieve positive free cash flow in H2 2024. Following the update, AML shares crashed by around 24% as of writing. Year-to-date, the stock has lost 43%.

Claim 30% Off TipRanks

- Unlock hedge fund-level data and powerful investing tools for smarter, sharper decisions

- Discover top-performing stock ideas and upgrade to a portfolio of market leaders with Smart Investor Picks

Aston Martin is famous for its luxury sports cars and iconic models such as the Vantage, DB11, DBS, DBX, and Valkyrie, among others.

Aston Martin Struggles with Supply Issues and China Slowdown

Aston Martin adjusted its 2024 wholesale volumes, implementing a reduction of approximately 1,000 units. This is to mitigate supply chain disruptions at multiple suppliers, which have resulted in an increasing number of late component arrivals. The company also highlighted the ongoing macroeconomic challenges in China, contributing to weak demand in the region.

For FY24, the wholesale volumes are projected to decrease by a high single-digit percentage compared to the previous fiscal year. Moreover, wholesale volumes and adjusted EBITDA for the third quarter of FY24 are now expected to fall short of current market expectations.

Moving ahead, Aston aims to streamline the flow of wholesale volumes in the upcoming quarters to align with its demand-driven strategy and enhance production efficiencies.

Aston Martin will release its Q3 2024 results on October 30.

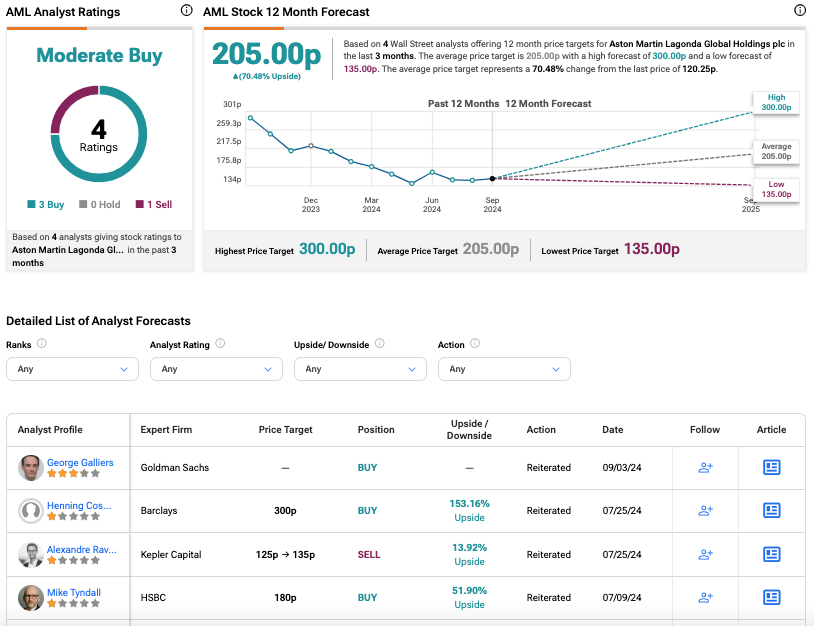

Is Aston Martin a Good Share to Buy?

On TipRanks, AML stock has a Moderate Buy consensus rating based on three Buys and one Sell assigned in the last three months. At 205.0p, the average Aston Martin share price target implies an upside of 70.5% from the current level.