ASML (ASML) is one of the best underrated chip stocks in the market, and it’s just warming up and getting started. The stock is up about 20% for the year and there’s a lot of room for it to run, but you’ll have to be patient.

Meet Samuel – Your Personal Investing Prophet

NVDS: built for a short position on NVDAThe Netherlands-based company makes photolithography systems that are used by the world’s leading foundries to make sophisticated chips for AI, High Performance Computing, and other resource-intensive use cases. Its top customers include Taiwan Semiconductor Manufacturing Company (TSM) and Intel (INTC).

I am bullish on ASML because of its clear moat in the semiconductor industry, a list of high-profile clients, and its secular runway, given that it’s on the cusp of a cyclical recovery in the semiconductor equipment industry.

ASML Has a Clear Economic Moat

One of the top reasons I like ASML is because of its long-term sustainable competitive advantage in the global semiconductor scene with its lithography systems. As I alluded to above, ADML creates systems that are used by leading foundries to make chips for semiconductor kingpins like Nvidia (NVDA) and Advanced Micro Devices (AMD).

Moreover, ASML has a near-monopoly position in Extreme ultraviolet (EUV) lithography systems and commands an ~83% market share (according to data from Khaveen Investments). But what is EUV lithography and why is it important?

Photolithography (the broader term for EUV lithography) is the process through which integrated circuits (ICs) are made. Lithography machines engrave complex circuit patterns on silicon wafers. These wafers are then used in multiple electronic devices, ranging from smartphones to powerful graphics processing units (GPUs) that we use for crypto mining or training an AI model.

You can think about ASML as the back-end of the back-end of the chip world. Without ASML, we wouldn’t have Nvidia chips. That’s how important this company is to the semiconductor industry.

ASML Is Just Getting Started

What’s paramount to my bullish stance is the fact that ASML is just getting started. While 2024 is expected to be lackluster for the company, as management pointed out during the Q2 2024 investor presentation, 2025 is expected to be great.

ASML’s revenue fell nearly 11.7% year over year to $6.8 billion in Q2 2024, but it beat analysts’ expectations by $212.7 million. The group’s EPS was $4.39 and was ahead of Street expectations by 36 cents.

Even though sales and profitability are falling year-over-year, they are recovering quarter over quarter. This revenue was up from the $5.6 billion ASML posted in Q1 2024.

The semiconductor industry is going through a broad-based slowdown this year and ASML, in particular, is facing some macro headwinds in addition to that. The US does not want China to get its hands on powerful chips and has therefore placed bans on chip exports to China. This isn’t good for ASML, since China accounted for ~50% of its revenue in Q2 2024, but this is mainly why the pessimists overreacted.

However, things aren’t as bad as the bears say. Management says 2024 is a “transition year” for them and I agree. ASML’s revenue may have tumbled, but its backlog of EUR 39 billion ($43.5 billion), at the end of Q2 2024, should not be discounted. The industry is near its bottom, but I see it picking up pace and recovering in 2025 on the back of strong demand from AI customers.

For full-year 2024, ASML expects revenue growth to be flat. But the company is ramping up production capacity and investing heavily in technology to prepare for next year. Indeed, in 2025, the semiconductor industry is expected to go through a cyclical upturn, and ASML is at an inflection point.

Moreover, management sees an expanding application space and an increase in lithography demand. They are optimistic about the secular tailwinds from the energy transition, electrification, and AI, which will drive long-term growth for the business.

I like this story and believe it will come to fruition. ASML is preparing for supplying its industry-leading lithography systems to fabs across different geographies.

With its end markets recovering by 2025, I don’t see management missing their sales target of EUR 30 billion to EUR 40 billion ($33.4 billion – $44.5 billion) in 2025; instead, I expect them to exceed it.

Additionally, their 2030 sales target remains unchanged at EUR 44 billion to EUR 60 billion ($49 billion – $67 billion), which they will update at their investor day on November 14. Call me a cockeyed optimist, but I expect an upwards revision.

More on What the Bears are Missing

I believe China problems aren’t a good enough reason to not like ASML stock, even though that part of the business is big and still under-penetrated. It’s just not worth ignoring a ~ $350-billion monopoly holder and ignorant investors should pay attention to more important things when evaluating a business.

For one, ASML has a monopoly in its market, as was established earlier in the article. This monopoly gives its pricing power, which can be seen in gross margin improvements. Its Q2 2024 gross margin was 51.5%, up from 51% in the prior quarter. That tells me its clients love the product and are willing to pay a premium for them.

Moreover, management strategically gave a conservative Q3 2024 outlook on margins and ASML is likely to beat expectations, as it has in the previous quarters. Under-promise and overdeliver is the recipe for capital appreciation in the long term.

Finally, ASML is seeing an improvement in its lithography tool utilization levels, both at the Logic and Memory levels. The company shipped more NXE:3800E systems during the quarter and continue to see observe demand for them. These systems are used in the volume production of 2 nanometer Logic nodes and leading-edge DRAM nodes, in a cost-efficient manner.

Analysts’ Take on ASML Stock

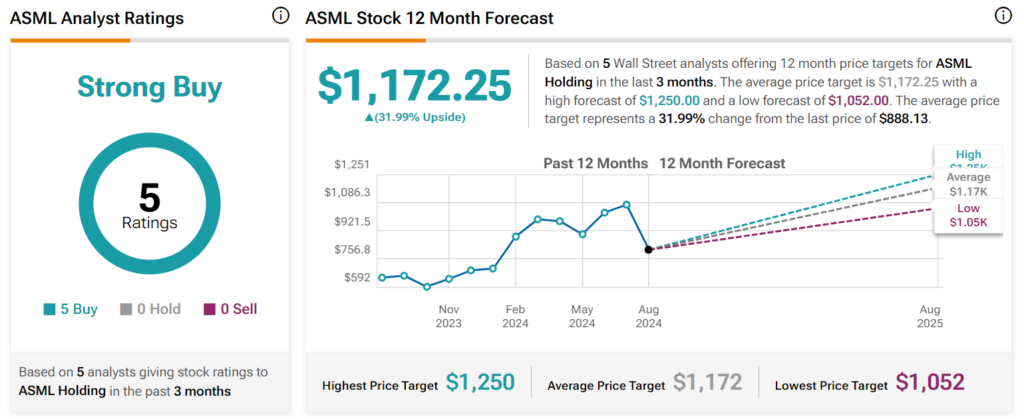

On the Street, ASML stock sports a consensus Strong Buy rating based on five unanimous Buys. The average price target of $1,172.25 represents an upside of nearly 32% from current levels.

The Bottom Line

ASML is a high-quality monopoly holder and a key enabler of multiple structural changes, thanks to generative AI. I’m bullish on ASML, but the valuation is rich (42 times forward earnings). If that’s too high for you, wait for a pullback before ASML stock’s expected rise.