As time goes on, Microsoft’s business keeps getting more efficient, blending the traits of a defensive stock with double-digit EPS growth, arguably making its premium valuation easier to justify.

Why Overvalued Microsoft Stock (MSFT) is Still a Winner

Story Highlights

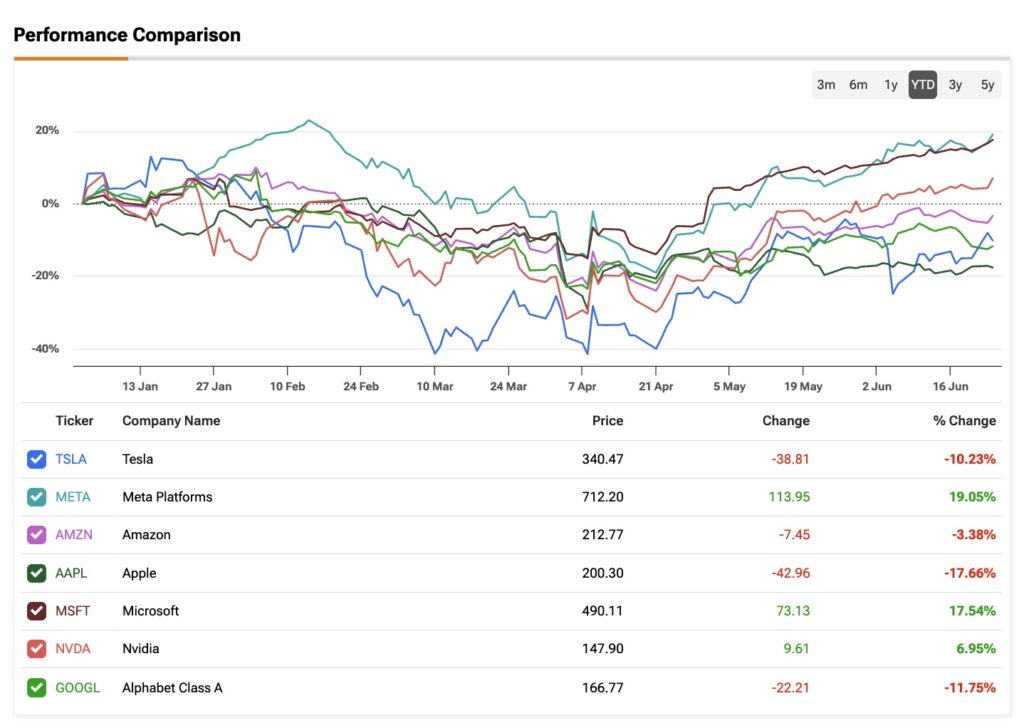

Microsoft (MSFT) bulls have had plenty to cheer about. Just behind Meta Platforms (META), the Redmond, Washington-based tech giant has been the second-best performer within the Magnificent 7 group, up 17% year-to-date, and an additional 24% since its Fiscal Q3 earnings.

Claim 30% Off TipRanks

- Unlock hedge fund-level data and powerful investing tools for smarter, sharper decisions

- Discover top-performing stock ideas and upgrade to a portfolio of market leaders with Smart Investor Picks

Beyond a calmer market tone following the tariff scare, Microsoft’s defensive qualities—which have stood out for decades as a stock that rarely underperforms—in my view, help explain its faster rebound compared to most of its mega-cap peers.

While the stock remains on the expensive side, this is the kind of name that, thanks to outlier-level efficiency at its scale, still deserves a Buy rating. Especially given that Microsoft tends to deliver better risk-adjusted returns during sustained optimism than in brief corrections.

Why Microsoft’s Fundamentals Still Impress

First and foremost, Microsoft is as strong as ever from a fundamentals perspective. Take Fiscal 2025’s Q3, reported at the end of April, when the company managed to grow operating income faster than revenue, up 16% to $32 billion, versus $70 billion in revenue, which rose 13% year-over-year. In other words, Microsoft is becoming increasingly efficient, keeping costs and expenses under control. That’s largely thanks to higher-margin segments—like Azure—growing faster than the rest of the business.

Overall, Microsoft posted an impressive 46% operating margin, putting it among the most efficient companies globally. If we look at the Rule of 40—a classic benchmark for evaluating software companies by combining revenue growth and operating margin—Microsoft easily clears the bar: 13% growth plus a 46% margin equals 59%, well above the 40% threshold typically seen as excellent. That highlights not just operational strength, but an exceptional number for a mature Big Tech company.

For comparison, smaller-scale and less mature companies like Palantir (PLTR) have posted even higher Rule of 40 results—its latest quarter came in at 83%, combining 21% growth with a 62% adjusted operating margin. But it’s important to note that Microsoft’s scale and complexity make a figure like 59% even more impressive and sustainable over time.

Looking at more apples-to-apples comparisons, Oracle (ORCL) posted a Rule of 40 of 55% last quarter (with 11% revenue growth and 44% operating margin), while Adobe (ADBE) virtually tied Microsoft with 11% revenue growth and a 49% margin.

Valuation’s Stretch but Microsoft Keeps Winning

Trading at 36.2x forward earnings, Microsoft is currently priced about 15% above its historical average, which, not coincidentally, is about how much I believe the stock may be overvalued at the moment, or at the very least, lacking a margin of safety.

For instance, if we run a conservative reverse DCF over the next five years using consensus analyst inputs—assuming a 10.4% revenue CAGR and 11% long-term EPS CAGR, no changes in working capital, and a tax rate of 18% (in line with last year’s)—Microsoft would be generating around $174 billion in free cash flow by year five.

Discounting at 8%, applying a 3% perpetual growth rate, yields an implied equity value of approximately $3.1 trillion, roughly 15% below its current market capitalization.

Although Microsoft’s valuation appears stretched, it’s fair to argue that this premium is justified by its consistent execution and the rarity of negative surprises. As a high-quality name, Microsoft has historically delivered better risk-adjusted returns when it’s in an uptrend and trading at a premium, rather than during pullbacks, when the valuation resets.

With MSFT now trading at $492—well above its 200-day moving average of $420—this seems to be one of those moments where relative strength matters more than traditional pricing, reinforcing the idea that the stock continues to lead in the ongoing quality rotation.

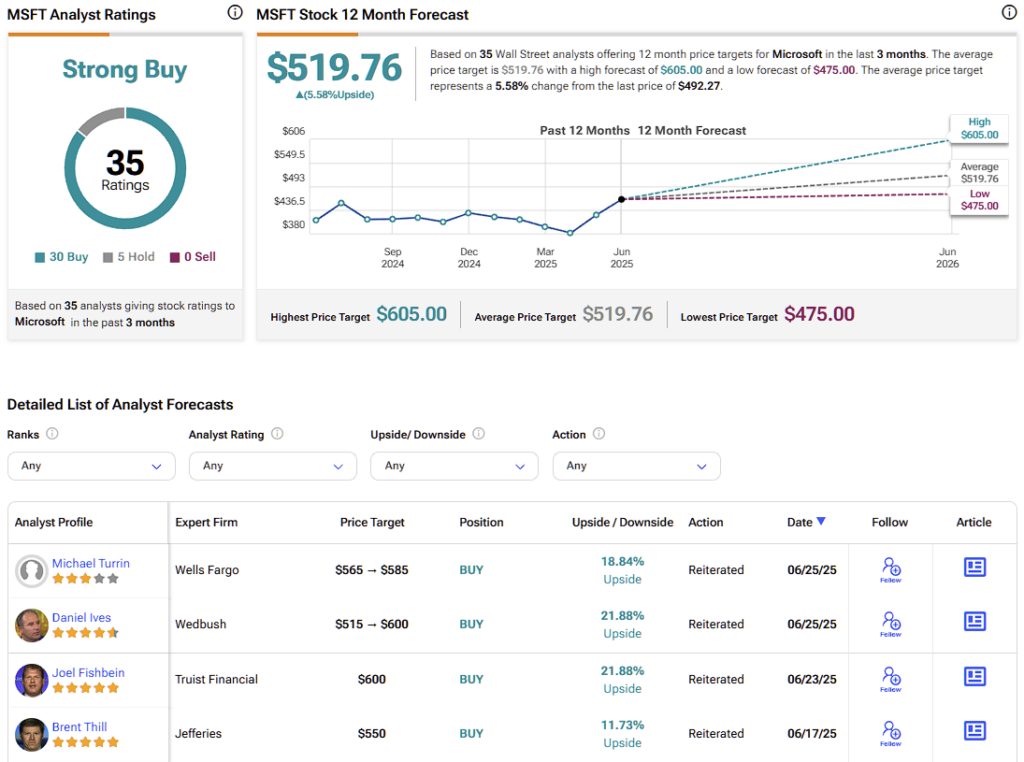

Is Microsoft a Buy, Hold, or Sell?

There’s a lot of optimism among analysts when it comes to MSFT. Out of the 35 covering the stock, 30 are bullish while the remaining five are neutral. Not a single analyst is currently bearish. The average price target is $519.76, indicating a modest upside of approximately 6% from the current share price over the next twelve months.

Few Reasons to Doubt Microsoft and the Long Thesis

While Microsoft’s current valuation leaves little margin of safety—even under conservative assumptions—I continue to support the bullish case. Since the rally began in April, the stock has shown no meaningful signs of weakness, and the market appears to recognize that few companies of this scale can match Microsoft’s level of operational efficiency.

That said, despite its defensive profile and strong long-term EPS growth forecasts in the double digits, Microsoft is not entirely insulated from external pressures. For instance, any slowdown in Azure AI adoption could prompt downward revisions from analysts and place pressure on the company’s historically elevated valuation multiples.

Nevertheless, I believe Microsoft’s broad-based strength across core enterprise segments provides durable support. As long as the current uptrend remains intact, I view this as a compelling opportunity to initiate or add to a long-term position.

1